- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted March 19, 2026 at 1:17 pm

Rates are jumping further today after Fed Chair Powell communicated yesterday during the FOMC presser that he isn’t leaving the central bank until the DOJ case against him is closed. Despite his term as head ending in May, he could stay on as governor if he so chooses. This development, in conjunction with the ECB and BoE stating that they are prepared to start hiking if need be to temper the adverse effects of the Middle East war, has Wall Street effectively pricing in no rate cuts in 2026. Meanwhile, the Iran conflict has been intensifying in recent hours, as attacks on critical energy facilities drive up the cost of crude and lift geopolitical worries throughout markets. Treasuries are also suffering retreats in response to this morning’s lighter-than-expected initial unemployment claims, which continue to weaken the argument that labor conditions require imminent monetary policy accommodation to avoid deterioration. But the curve is ascending in bear-flattening fashion led heavily by the shorter-tenors by a difference of about 8 basis points, as duration hangs in there in consideration of slowdown concerns and stronger odds of demand destruction causing inflation expectations to soften. Indeed, sluggish activity projections are dealing losses across all major stock benchmarks, with 10 of 11 sectors, sub-components, the greenback and the commodity complex sinking with energy being the sole exception in equities and physical inputs. A lack of speculative enthusiasm is weighing on cryptocurrencies while participants reach for volatility protection instruments in light of greater hedging interest. Additionally, forecast contracts are catching non-correlated opportunity bids.

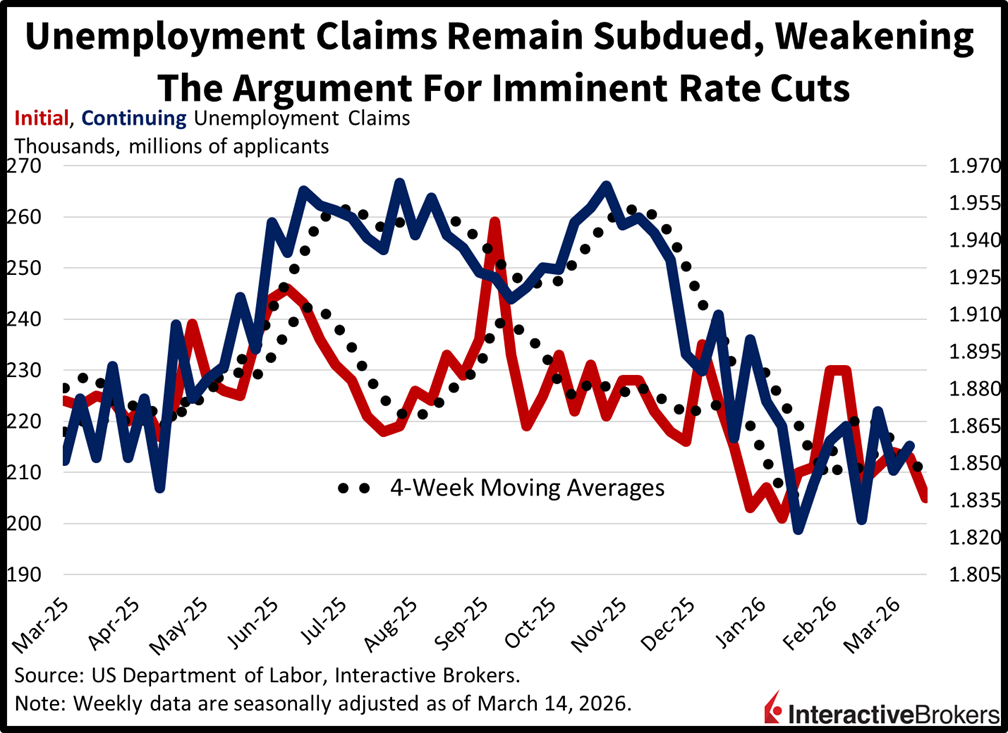

Layoffs remained subdued in the past two weeks as employers continued to refrain from workforce reductions. Initial unemployment claims dropped to 205k for the week ended March 14, lighter than the expected 215k and the prior time span’s 213k. Continuing filings rose slightly to 1.857 million, above the anticipated 1.850 million and the previous interval’s 1.847 million. Four-week moving averages were relatively stable at 210.75k and 1.851 million.

Sales of new homes dropped to a 39-month low to start the year as builders kept more inventory even as they cut prices. The pace of transactions took a 17.6% month over month (m/m) dive to 587k seasonally adjusted annualized units in January, much less than 720k projected and the 712k from December. All regions contributed to the plunge with the Northeast, Midwest, West and South decreasing 44.7%, 33.9%, 21.6% and 8.1% m/m, while the average and median closing values fell 4.5% and 5.9% m/m. Inventory based on the number of months required to sell new builds, which is key measure of dwellings on the market, grew 21.3% m/m from 8.0 months to 9.7 months, also a 39-month high.

The rapid acceleration in inflation, which we wrote about yesterday while detailing projections of 3- and 4-handles on the March Consumer and Producer Price Indices that will be released next month, has finally caught up to central banks. Wall Street has been hoping for a quick end to the Middle East conflict but at this point, the damage to charges across the economy are likely to have already lifted cost pressures materially for at least the first six months of 2026. But with President Trump and his administration highly attentive to the leap in oil prices and looking for this war to end quickly, the back half of this year may be terrific for stocks and fixed-income assets alike against the backdrop of the potential for a delayed economic reacceleration as well as slowing cost forces. For equity investors seeking bargain opportunities as we progress through the calendar, the upcoming several weeks may provide value-hunters with chances to pounce on sparks of volatility as markets react to the likelihood of slower growth and a steady Fed. Conversely, there’s risk of the Iran battle extending past the summer, and that would unfortunately lead to the US monetary policy authority joining its counterparts around the world by opening the door to hikes. That would result in a down year for benchmarks and Treasurys, similar to 2022, when an inflationary surge left participants with few places to hide. In conclusion, rotating from T-bills to duration isn’t terrible in this environment, as traders can use spikes in yields to extend along the curve while utilizing drops in borrowing costs as a motivator to capture opportunities at the short end.

The European Central Bank (ECB) and the Bank of England (BOE) both decided to hold their key interest rates in response to growing uncertainty regarding the impact of the Iran war on inflation and economic growth. Central bankers in Switzerland and Sweden reached similar conclusions. In the aftermath of the decisions, investors are increasingly anticipating that the BOE and ECB will each hike rates twice this year. In a press release, the ECB maintained that the war created upside risk for inflation and downside risk for economic growth. The hostilities will have a material impact on near-term inflation by increasing energy costs. Medium-term implications, however, will depend on the intensity and duration of the conflict. On a positive note, the ECB maintains its Governing Council is well positioned to deal with the Middle East turmoil with inflation close to its 2% target. The ECB also revised its 2026, 2027 and 2028 inflation forecasts upward to 2.6%, 2% and 2.1%. In December, it estimated headline inflation would hit 2.2%, 1.9% and 2.0% in 2026, 2027 and 2028. The ECB also trimmed its GDP growth estimate to from 1.2% to 0.9% for this year and from 1.4% to 1.3% for 2027. The organization’s interest rates on its deposit facility, main refinancing operations and the marginal lending facility are 2%, 2.15% and 2.40%, respectively.

The BOE, for its part, held its key interest rate at 3.75% and Bank Governor Andrew Bailey emphasized that the institution’s goal, regardless of what happens, is to push inflation down to 2%. The UK was expected to reach that target in the coming months, but with growing uncertainty, it’s unclear when that will happen.

The Bank of Japan also issued warnings about inflation from the Middle East conflict and decided to hold its key interest at 0.75%. In announcing the decision, which was widely expected by investors, it said inflation risks are tilted to the upside due to the war. Only one member, Hajime Takata, of the nine-person board opposed the decision and stumped for a 25-bps hike. Japan imports nearly all of its energy from the Middle East. Slowing price hikes for rice have helped the BOJ curtain inflation but rising costs of oil prices driven by the war will create stronger price pressures.

Orders for machinery received by a survey group of 280 manufacturers in Japan dropped 2% month over month (m/m) in January after climbing 19.8% and 7.1% in December and November, according to the Cabinet office. Core orders, which exclude ships and orders from electric companies, furthermore, slipped 5.5%. For the core print, a consensus of economists anticipated a 9.6% drop following December 19.1% expansion.

Even with the m/m decline, core orders were 13.7% higher than in the year-ago period, a result that exceeded the economist estimate for a 10.5% gain following December’s 19.8 y/y growth. Among private sector orders, requests for manufacturing tools sank 12.5% with the petroleum and coal products sinking 75.9%, pulp, paper and paper products equipment contracting 33.8% and non-ferrous metals down 57.1%. Equipment orders from non-manufacturing customers were 0.2% higher m/m.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. Eligibility to trade in digital asset products may vary based on jurisdiction.

Short selling is an advanced trading strategy involving potentially unlimited risks and must be done in a margin account.

Trading on margin is only for experienced investors with high risk tolerance. You may lose more than your initial investment. For additional information regarding margin loan rates, see ibkr.com/interest

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!