- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted April 29, 2025 at 1:00 pm

Investors are stepping up to the plate and engaging in some buying despite lackluster corporate earnings reports that included several companies canceling forward guidance due to elevated uncertainty regarding cross-border commerce. Meanwhile, tensions flared as the White House reflected its disappointment concerning Amazon.com’s plan to reflect the added costs from tariffs onto the actual packaged goods themselves. But stocks are up for the sixth day in a row, and today’s bullishness is motivated by softening economic data that are bolstering the case for an imminent Fed cut. Indeed, this morning’s updates were awful, missing expectations by a mile and then some. Consumer confidence fell for a fifth consecutive month to its lowest level since the depths of the pandemic in 2020, job openings dropped to the weakest point in six months and the trade deficit ballooned to a new monthly record as folks rushed to acquire products prior to the implementation of levies. Still, markets are optimistic today as traders grab equities, Treasuries, greenback futures, bitcoins and forecast contracts while trimming exposures to commodities and volatility protection.

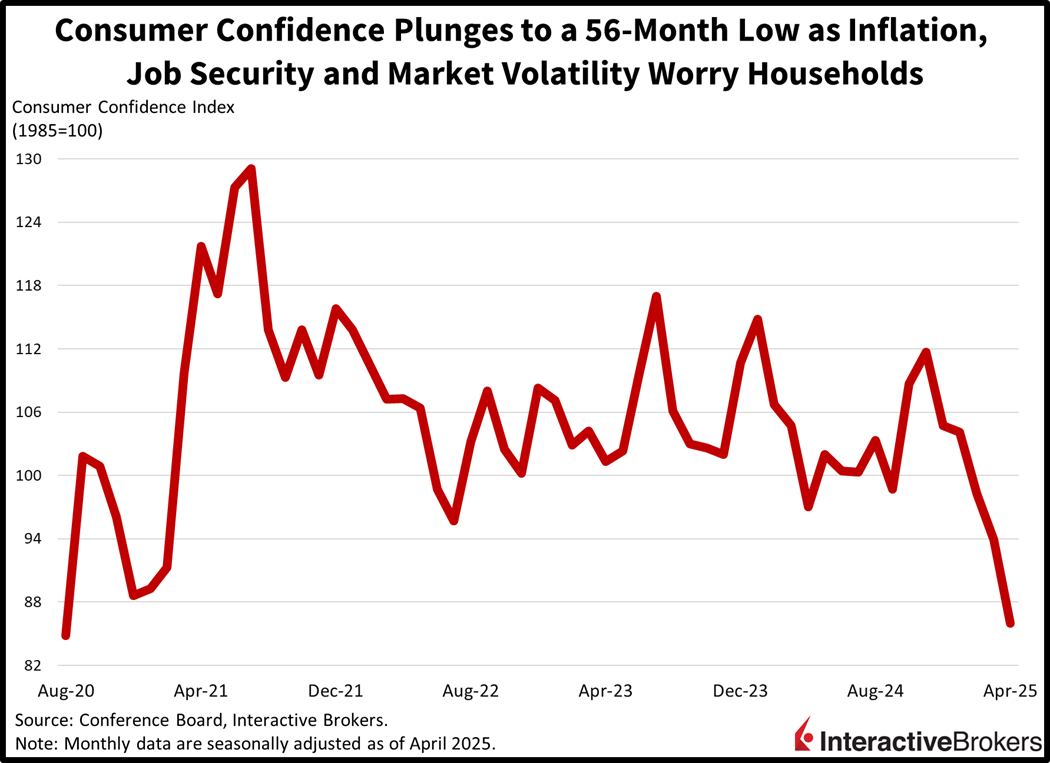

Consumer confidence plunged to its lowest level since August 2020 as anxiety regarding elevated prices, heavy interest rates, job security and market volatility fostered rising pessimism. The Conference Board’s Consumer Confidence Index declined to 86 this month, missing the 87.5 projection and arriving beneath March’s 93.9. While current conditions held in there, the outlook for the future severely weighed on the print. The Present Situation and Expectations sub-indices dropped 0.9 and 12.5 points to 133.5 and 54.4, as the latter gauge fell to its weakest result since October of 2011.

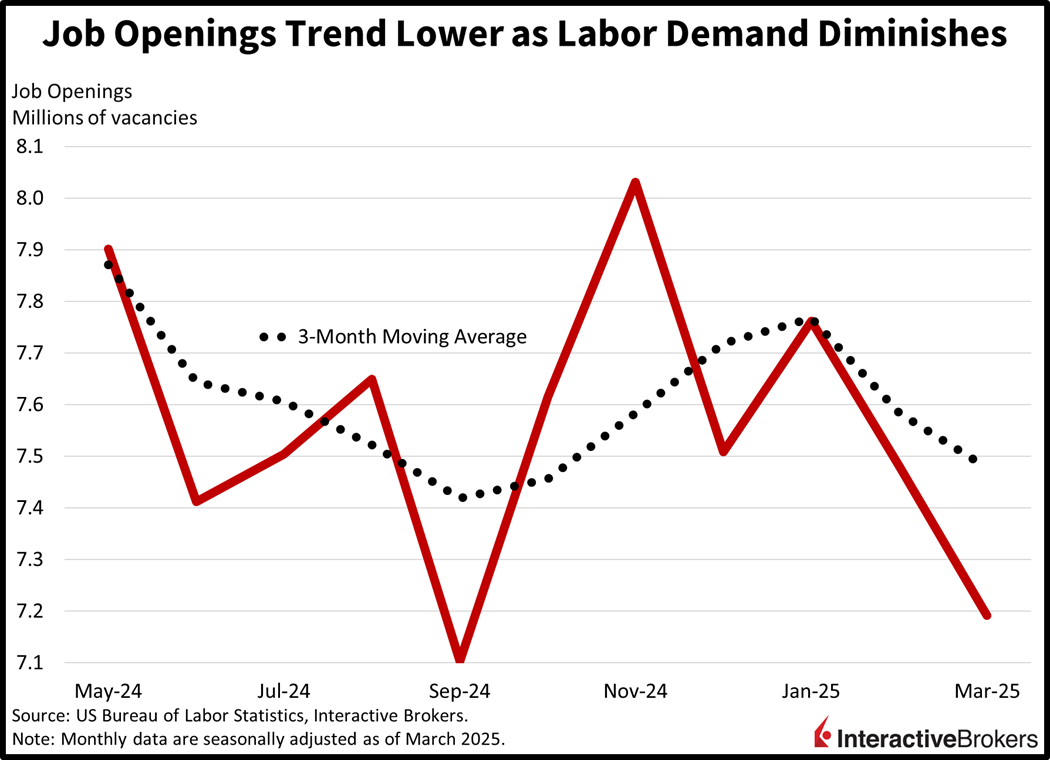

For-hire signs fell to a six-month low in March amidst broad-based sectoral weakness. Worker vacancies slipped to 7.192 million, according to the Bureau of Labor Statistics’ (BLS) Job Openings and Labor Turnover Survey. The result missed the median estimate of 7.50 million and sank from the preceding period’s 7.48 million. It marked the second consecutive monthly drop. Quits rose slightly, however, from 3.25 million to 3.332 million.

The trade deficit among goods fell to $161.99 billion for the month of March, the largest gap on record as folks rushed to import products ahead of Trump tariffs. The result trounced expectations calling for a reduction to $146 billion after February’s figure came in at $147.85 billion.

Markets are climbing and every major domestic equity benchmark is in the green. The Dow Jones Industrial, S&P 500, Nasdaq 100 and Russell 2000 indices are higher by 0.5%, 0.2%, 0.2% and 0.1%. All sectors are participating minus energy and consumer discretionary, which are down 0.5% and 0.4%. Real estate, materials and financials are leading the charge, gaining 0.5%, 0.5% and 0.4% on the session. Treasuries and the greenback are also catching bids with the 2- and 10-year Treasury maturities changing hands at 3.66% and 4.18%, 3 basis points (bps) lighter across both instruments. The Dollar Index is up 21 bps as the US currency appreciates against most of its major counterparts, including the euro, pound sterling, franc, yen, loonie and Aussie tender, but it is depreciating relative to the yuan. Commodities are being sold on weaker economic prospects and light safe haven demand, with crude oil, gold, lumber, copper and silver falling 2%, 1.1%, 0.6%, 0.3% and 0.1%. WTI crude oil is trading at $60.55 per barrel on a challenging consumption outlook amidst elevated uncertainty.

Tomorrow’s data will be pivotal as both the European Union and the United States release their preliminary reads of first-quarter GDP. Forecasters expect a few tenths of a percent above the 0 mark for the regions, 0.2% on the east side of the Atlantic and 0.4% on the west side. Meanwhile, investors are eager to analyze the prints in order to gauge the impacts of Trump tariffs and the resulting uncertainty on economic growth as well as corporate earnings prospects. But the calendar is much broader; folks will also get a look at April hiring from ADP, wage pressures from the BLS’s Employment Cost Index, consumer spending trends as well as inflationary forces from the Census Bureau’s Personal Income and Outlays report and more. Turning back to GDP, however, today’s wider trade deficit reading raises the chances of a negative figure for the US, with our prediction market pointing to a 41% probability of a number at or below 0.

Liberal Party candidate Mark Carney won the prime minister race yesterday with a platform that focuses on investing in new trade corridors, increasing defense spending, building rental apartments and growing the country’s technology industry. Carney has proposed a $150 billion increase in spending to fund those initiatives, which would increase the annual deficit from 1.47% of gross domestic product (GDP) to 1.96%.

The Singapore Domestic Supply Price Index climbed 3.9% year over year (y/y) last month, easing from the 5.5% rate in February. The machinery and transportation equipment component led the advance, soaring 15.6% y/y while the animal and vegetable oils category gained 7.1% and the food and live animals group increased 5.7%. Chemicals and chemical products along with the manufactured goods groups were the only decliners with prices falling 4.4% and 0.8%, respectively. While efforts to contain inflation were aided by a 4% decline in costs for imports compared to February’s 3.4% drop, charges for exports also weakened. After declining 3.5% in February, prices last month dropped 5.1%.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Interactive Brokers LLC is a CFTC-registered Futures Commission Merchant and a clearing member and affiliate of ForecastEx LLC (“ForecastEx”). ForecastEx is a CFTC-registered Designated Contract Market and Derivatives Clearing Organization. Interactive Brokers LLC provides access to ForecastEx Forecast Contracts for eligible customers. Interactive Brokers LLC does not make recommendations with respect to any products available on its platform, including those offered by ForecastEx.

This is commentary on economic, political and/or market conditions within the meaning of CFTC Regulation 1.71, and is not meant provide sufficient information upon which to base a decision to enter into a derivatives transaction.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!