- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted May 27, 2025 at 1:04 pm

Wall Street is in risk-on mode as a friendly weekend conversation between President Trump and European Commission Head Von der Leyen is bolstering optimism about a transatlantic trade deal. The US Commander in Chief happily agreed to extend the tariff deadline to July 9 while both sides work diligently to forge an agreement. But also strengthening animal spirits is news suggesting that Tokyo is considering lessening bond issuance in an effort to quell pressure at the long end. Rates are plunging as a result and helping to support stocks while the yield curve shifts south in bull-flattening fashion with the cost for duration dropping faster than the price at the shorter-ends. Furthermore, the first monthly increase in consumer confidence since November is adding to the positive sentiment and serving to propel chances of an augmented economic expansion ahead. Investors are responding to the mix of desirable developments regarding cross-border commerce, fixed-income supply and the economic calendar by scooping up equities in all sectors, Treasuries across the curve, greenback futures, cryptocurrencies and forecast contracts. Conversely, folks are unwinding their volatility hedges and reducing their exposures to major commodities minus natural gas.

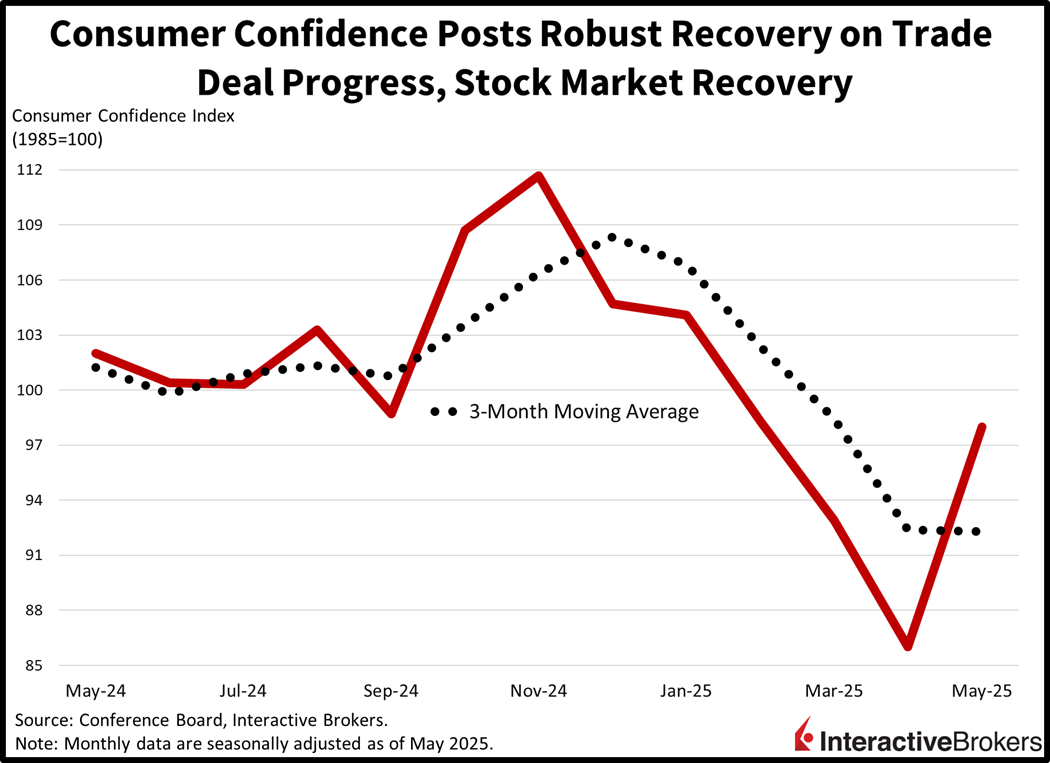

Consumer confidence climbed in May for the first time in six months, as breakthroughs on trade supported optimism about the road ahead. The Conference Board reported a headline score of 98, exceeding the median estimate of 87 and April’s 85.7. The Present Situation and Expectations components both strengthened from 55.4 and 131.1 to 72.8 and 135.9. The gains were driven by broad-based progress across business, income and employment conditions, although perceptions related to current job availability weakened slightly. Households reflected improved sentiment regarding stock prices, inflation, recession risk and making large purchases in the next few months. Still, folks were worried about tariff uncertainty and the potential adverse affects on the economy and personal finances.

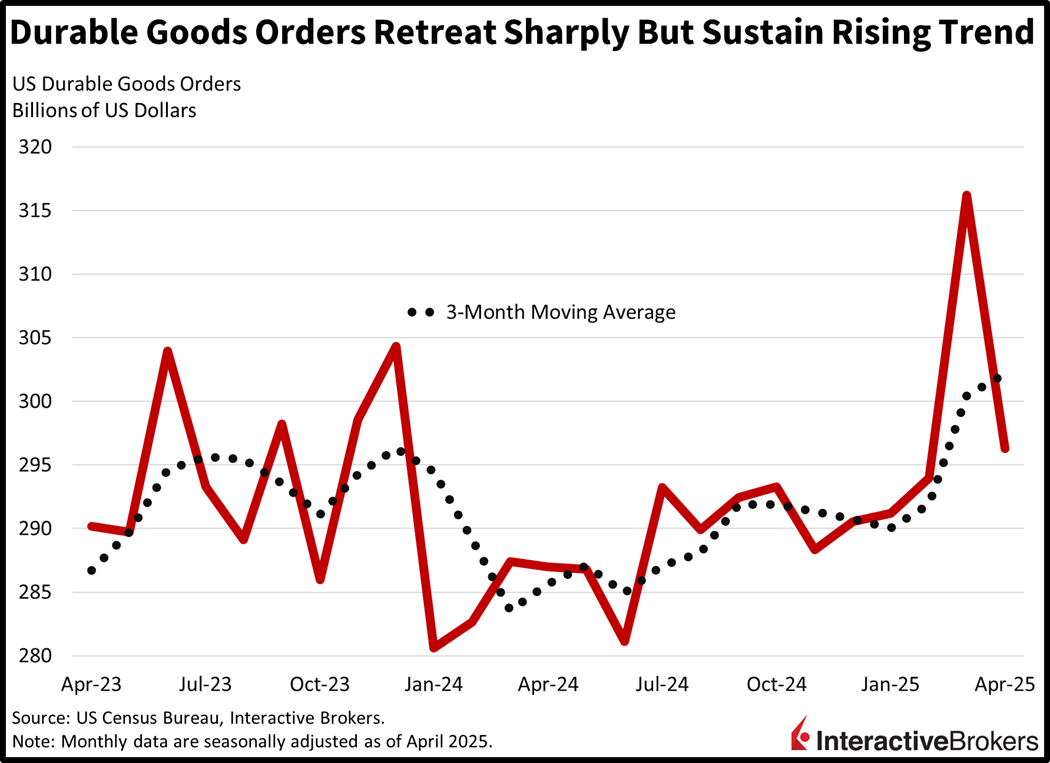

Durable goods orders declined significantly last month because households and firms completed the majority of their purchases in March to avoid liberation day tariffs. Transactions decreased a meaningful 6.3% month over month (m/m), marking the steepest fall in 15 months but arriving ahead of expectations for a drop of 7.8%. March sported a 7.6% gain, meanwhile. Weighing on headline results most notably last month and the extent of the various components’ declines were as follows:

The defense capital goods, computer, machinery and fabricated metal product categories helped to cushion the blow, however, increasing 30.5%, 6.5%, 0.8% and 0.8%. Nondefense capital goods, excluding aircraft, a proxy for business investment, dropped a sharp 1.3% m/m as corporates boosted inventories the month prior, before significant levies were announced.

Economic conditions in the Federal Reserve’s Dallas region weakened this month as revenue trends worsened despite broad-based gains in other categories. The Texas Manufacturing Outlook survey sported a headline score of -15.3, improving from March’s steeper rate of decline, which was -35.8. Firms increased their headcounts, wage bills and capital expenditures, but margins faced pressures since costs paid for raw materials expanded at a much faster pace than the prices received for finished products.

Today’s buoyancy is being helped by factors associated with fundamentals as well as valuations. Improving prospects regarding a transatlantic trade deal are boosting revenue projections while countering inflation expectations, helping corporations at the top-line as well as with their margin profiles, while also aiding in bringing down the price of duration. Additionally, news supporting reduced issuance from Tokyo at the long end boosted anticipations of economic growth while subduing term premiums. And then consumer confidence really assisted Wall Street in illuminating what was once the somber Trump trade tunnel, with investors asking themselves, if households see the worst of cross-border commerce behind us, why shouldn’t we? Combine that with lighter costs of capital folks, and in conclusion, the rallies in stocks and rates have further to go.

Singapore’s industrial production climbed 5.3% m/m in April, reversing from a 2.7% decline in March. For the year over year (y/y) metric, production was up 5.9%, moderating from the 6.8% March increase. The m/m print benefited from exporters frontloading orders in preparation of potentially higher tariffs.

S&P Global and Moody’s recently said they will keep their AA+ and Aa3 credit ratings for Hong Kong. S&P also raised its outlook from negative to stable. Just last week, Fitch said it will continue with its AA- rating and stable view of the country. The most recent two firms to say they are maintaining their ratings cited the Special Administrative Region’s fiscal buffers, external balance sheet, higher personal income levels and foreign exchange reserves.

Hong Kong’s trade imbalance in April fell from $45.4 billion to $16 billion. Overall cross-border commerce activity, however, moderated, with export growth of 14.7% y/y compared to 18.5% in the preceding period and import expansion easing from 16.6% y/y to 15.8%.

Japan’s Services Producer Price Index, which is commonly viewed as in indicator of future inflation, climbed 0.5% m/m and 3.1% y/y. The annualized figure exceeded the consensus forecast of 3%, but eased from the March increase of 3.3%. The m/m result also moderated after moving north by 0.8% in March. Among broad categories, the other services group posted the largest m/m gain of 1.6% followed by the 0.7% gain of transportation and postal services. Advertising services and international transportation sank 7.3% and 4.5%.

Manufacturing sales in Canada dropped 2% m/m in April after falling 1.4% in the prior month. In April, transactions of coal, petroleum and motor vehicles fell considerably. The final March result was adversely impacted by lower metal volumes following the US implementing tariffs on imports from the country.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!