- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted October 9, 2025 at 12:54 pm

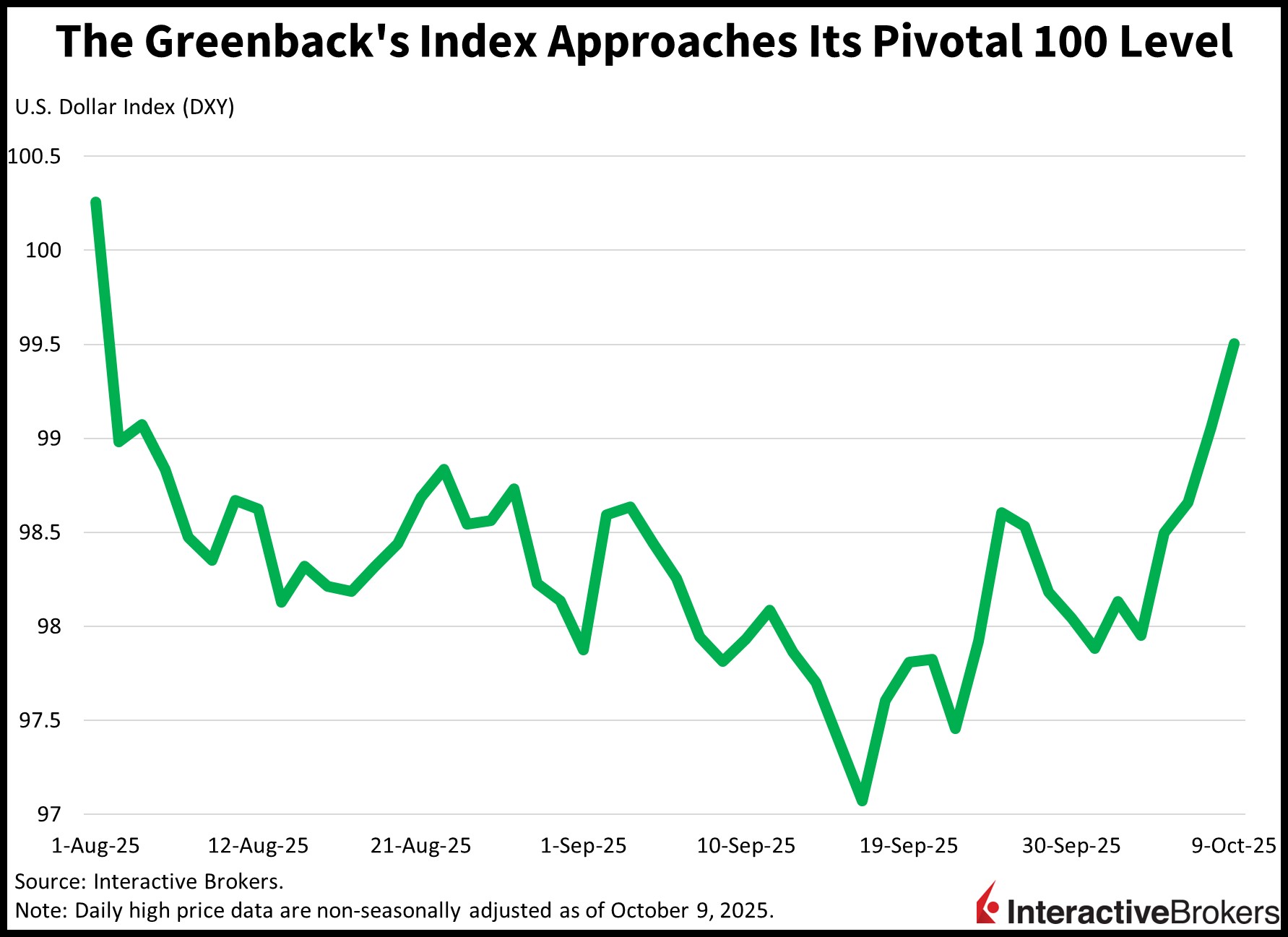

The greenback is surging again in response to yesterday’s release of minutes from the Fed’s September meeting that depict division among policymakers regarding the expected number of rate cuts in the next few meetings. Treasuries are slipping against this backdrop, as Wall Street places the probability of a quarter-point trim in December at 80%. An October trimming of the key benchmark is essentially in the bag at 95% and equity investors are now focusing on how many subsequent reductions will occur. Meanwhile, the US government shutdown, on its ninth day, continues to cloud the rationale for investment decisions and monetary policy expectations, and our IBKR prediction market participants believe there’s a higher chance than not of a reopening on the 23rd of this month. Amidst a lack of economic data, however, corporate earnings are starting to arrive before the season heats up on Tuesday. This morning’s results from Delta Airlines were well received, as the company pointed to resilient consumers that bolstered a profit beat. The company also provided strong guidance, including margin expansion through 2026. In trading action, all 11 major equity sectors are retreating and bitcoin is also being hit by the risk-off sentiment. Conversely, the commodity complex is largely bullish across the majors, excluding gold and natural gas. Volatility protection instruments are catching bids on heavier hedging demand while forecast contracts additionally see interest.

The AI theme has dominated stock market returns in the past few years because the technology is growing bottom lines and expanding earnings multiples. As a result, investors are looking for additional information about current levels of AI profitability and expectations for future earnings. Capital expenditure prospects as well as whether the outlays will pay off in the long run are also a critical topic for investors. There’s been talk on Wall Street regarding potential froth in risk-assets that could generate significant volatility if AI investments fail to deliver against the backdrop of elevated earnings estimates. Meanwhile, the lengthier the government shutdown goes, the weaker short-term economic conditions will become, in my view, and that is currently a more front-and-center danger. But the good news is that pro-growth government policies coinciding with a friendly business environment are likely to justify a bullish outlook.

Consumers in Australia anticipate that overall prices will grow 4.8% in the coming 12 months, according to the October Melbourne Institute Inflation Expectations Index. The result is up from 4.7% in September and is the highest print since June’s 5% result.

After slipping 6.4% month over month (m/m) in July, orders for tools climbed 14.7% in Japan last month, according to the Japan Machine Tool Builders Association (JMTBA). Sales also picked up relative to the year-ago period with September logging a 9.9% year-over-year (y/y) jump compared to the 8.5% August increase. At a time of increased global trade uncertainty following efforts by the US to increase onshoring, Japanese tool providers experienced a 13% y/y increase in foreign orders with domestic purchases expanding only 3%.

The UK’s residential real estate market languished for a third-consecutive month in September despite some metrics improving modestly, according to the Royal Institution of Chartered Surveyors (RICS). In a RICS survey of property professionals, 19% of respondents reported a decline in buyers, marking the third consecutive month of sinking demand. The organization’s price balance gauge, which tracks the percentage of price increases and declines, was -15 last month, slightly better than -18 in August. Nevertheless, the negative number implies that more prices have sunk than have climbed. In another metric, demand for leases remained stable while the number of landlords listing rental properties has hit the lowest level since early 2020, prompting RICS to predict that rental costs will climb 3% during the coming 12 months. Broadly speaking, landlords have been selling properties in response to increases in borrowing costs and other expenses. Proposed legislation to increase tenant rights is also believed to have motivated property owners to sell. In other recent developments, the Institute of Chartered Accountants found business confidence in the third quarter hit its lowest level in three years.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!