- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted July 16, 2026 at 1:28 pm

Escalating Middle East violence continues to offset the impact upon investor sentiment of this week’s positive economic data and corporate earnings as an extended climb in energy prices weighs on markets. WTI jumped to nearly $81 before the bell, which countered optimism that resulted from the pair of much cooler-than-expected inflation reports of the past two days. Higher oil is also increasingly testing the consensus view that peak cost pressures are behind us. Interest rates and the greenback have remained restrictive as a result, despite this week’s unexpected CPI and PPI declines. This morning’s lighter-than-anticipated unemployment claims amidst the fifth consecutive month of retail sales growth certainly didn’t help the Treasury complex either, because the firm numbers strengthened GDP estimates and Fed hike wagers, which inflicted pain on equities. The Dow Jones Industrial Average is the sole gainer of the 4 major domestic benchmarks, even as 7 of the 11 sectors rise. In the tech world, a robust quarter from Taiwan Semi is failing to bolster chipmaker enthusiasm on valuation and payout worries; however, 5 of the Magnificent 7 are appreciating, helping to limit the damage for the Nasdaq 100 and S&P 500 indices. Elsewhere, commodities ex precious metals and prediction markets are catching bids but a retreat in animal spirits is hampering cryptocurrencies. Additionally, volatility protection instruments are seeing loftier premiums on greater hedging demand.

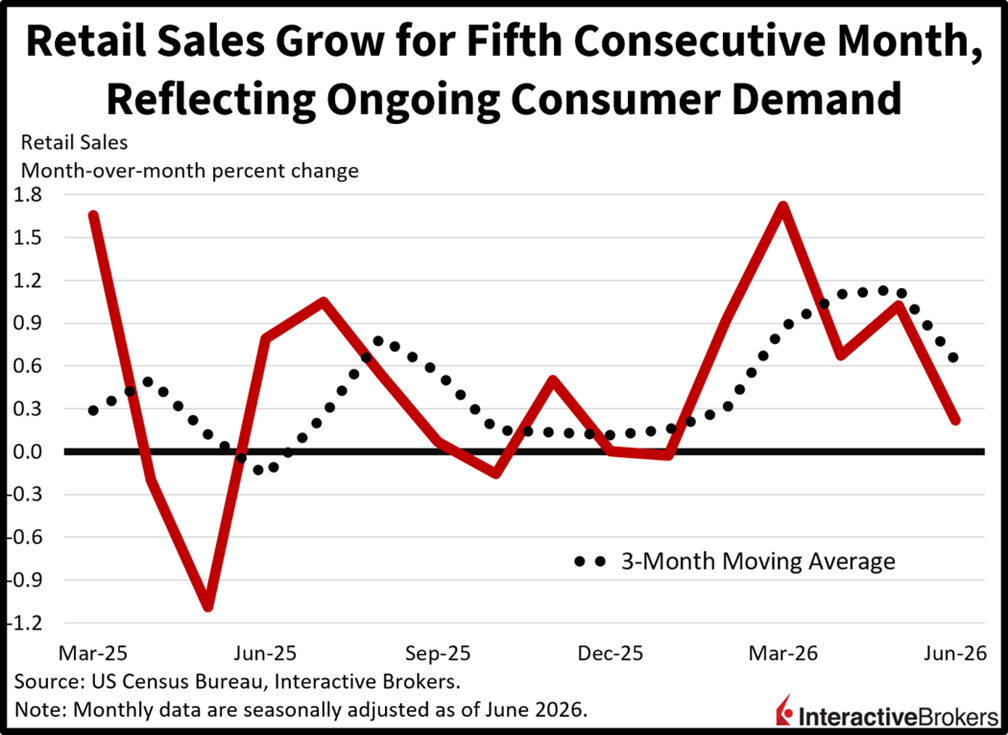

Retail sales expanded for the fifth consecutive month in June as consumer demand remained robust even as lighter energy prices limited transaction aggregates. Cash register dollars grew 0.2% month over month (m/m), in-line with expectations but marking a deceleration from May’s 1% gain. When excluding gasoline and automobiles; however, activity was even stronger, expanding 0.4% m/m, although it also tempered results when compared to the prior period’s 1%. Similarly, the critical control group rose 0.5%, as projected, but slower than the previous interval’s 0.8%. The progress wasn’t broad-based though, as the following groups experienced the stated increases:

The building materials, general merchandise, restaurant/bats segments saw gains of just 0.1% while furniture showrooms were unchanged. Conversely, the categories that experienced declines and the extent of their changes were as follows:

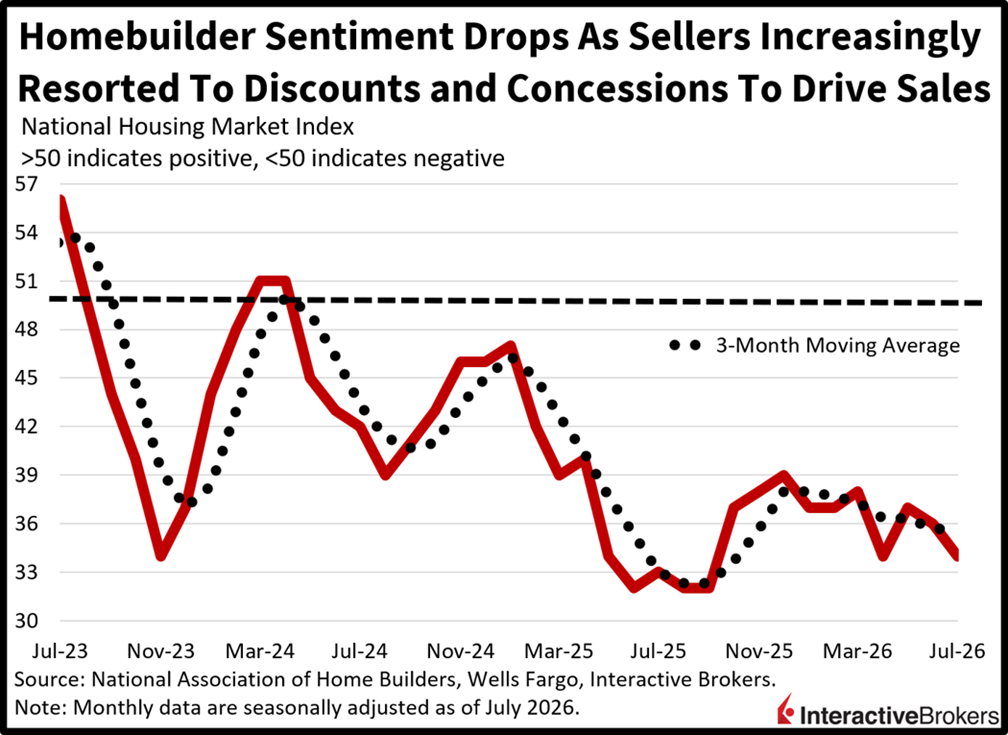

Homebuilder sentiment declined this month as the monthly payment picture worsened for potential purchasers against the backdrop of elevated mortgage rates and lofty valuations. The National Association of Homebuilders/Well Fargo headline index of 34 matched its lowest level since April, fell from June’s 36 and missed the median estimate of 35. The sub-indices for current sales momentum, the outlook over six months and traffic of prospective buyers all weakened, dropping from 38, 45 and 25 to 37, 43 and 23. Among regions, the Northeast and West slipped from 50 and 27 to 25, the South was unchanged at 31 and the Midwest climbed 1 point to 46.

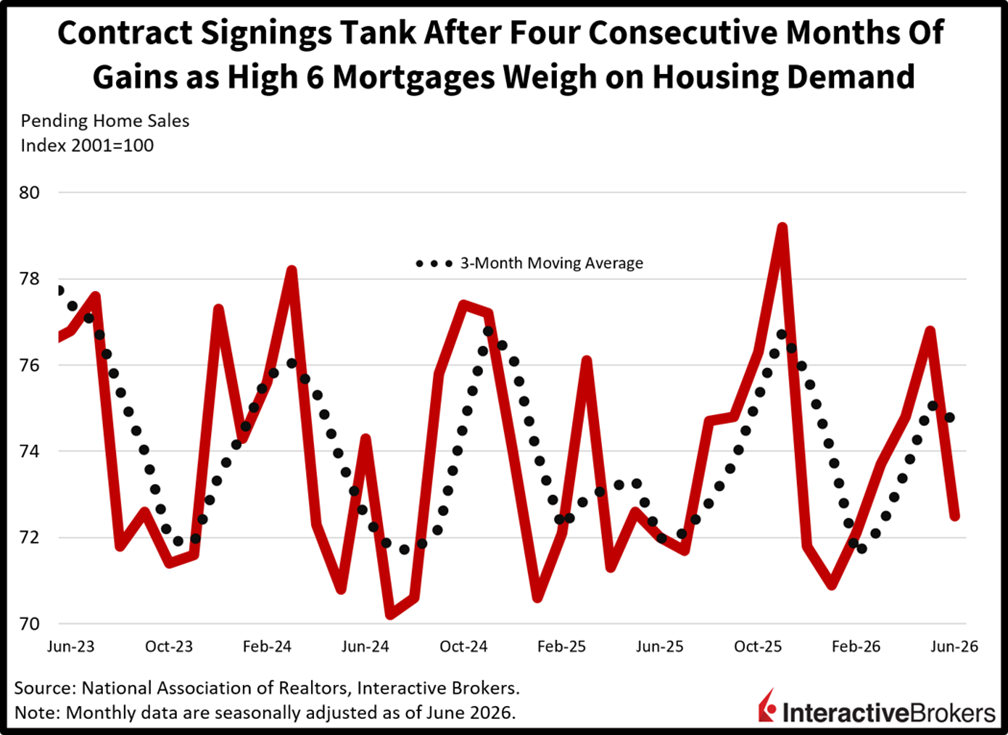

The sluggish mood amongst homebuilders was also present in the pending home sales indicator, which tanked following four consecutive months of gains. Contract signings fell 5.4% m/m and 0.3% year over year (y/y) in June as high 6 handle mortgages and record high values weighed on residential demand. All regions weakened as the Midwest, West, South and Northeast saw m/m declines of 8.9%, 4.7%, 4.1% and 3%. On a positive note, the West and Midwest experienced modest y/y progress of 1.1% and 0.3%.

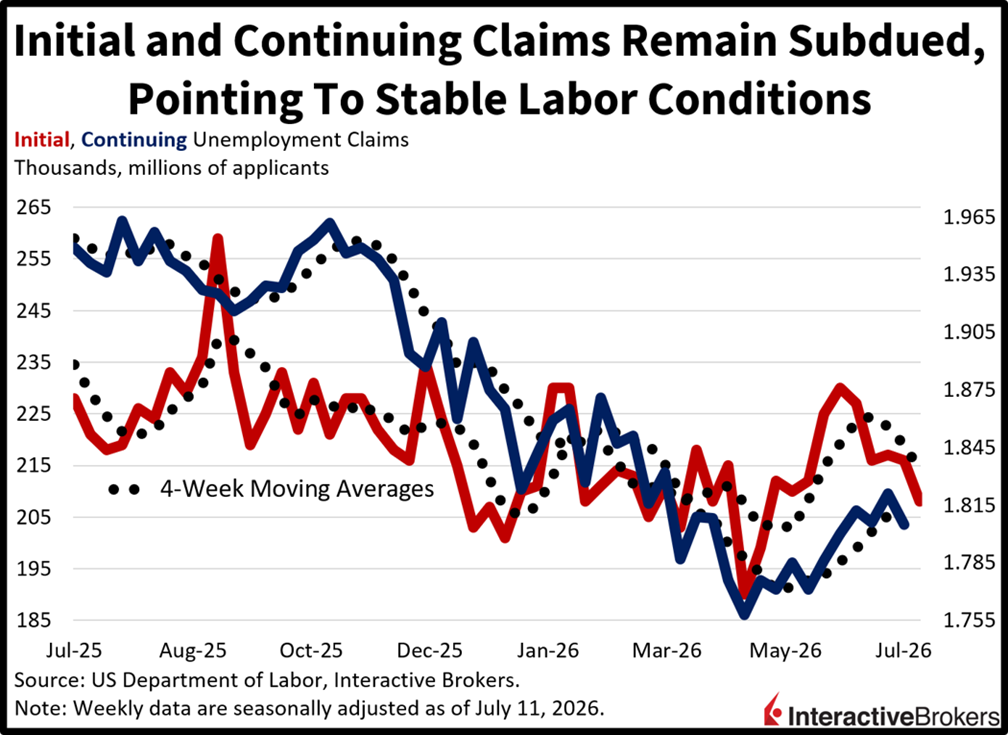

Unemployment claims continue to point to labor market stability. Both the initial and continuing segments fell during the past two weeks to 208k and 1.805 million from 216k and 1.821 million for the seven-day periods ending on July 11 and July 4. Additionally, the indicators were beneath the median estimates of 217k and 1.820 million. Four-week moving averages fell slightly for first-time applications to 214.25k and climbed modestly to 1.811 million for ongoing filings.

The $80 resistance level on West Texas Intermediate crude oil is holding even US-Iran violence has intensified. Energy traders still believe that President Trump will tilt to a conciliatory posture in the next few days in consideration of a constituency that doesn’t want to face a renewed bout of pain at the pump. Meanwhile, the GOP is navigating an anticipated Senate majority result in the upcoming midterm election while the Democrats are expected to handily win back the House of Representatives, according to our Prediction Markets. An escalation of the US’ actions against Iran would make political sense after the midterm elections rather than during the summer. Furthermore, the commander in chief’s goal of lighter interest rates is made increasingly complicated by these tensions, as they may very well force Fed Chair Kevin Warsh’s hand towards a benchmark lift. Additionally, we are entering a period of seasonal weakness for markets next month and ongoing geopolitical hostilities are poised to worsen equity and fixed-income performance; however, I continue to think duration is undervalued and overlooked by investors and believe that long-end yields will fall hard at some point in the coming six months.

The UK’s gross domestic product (GDP) grew 0.1% m/m and 1.3% y/y in May following April’s 0.1% m/m decline and 1.1% annualized expansion. Economists anticipated that May would produce no growth compared to April and post a 1.4% jump compared to the year-ago period. For the m/m result, services were up 0.3%, but the tailwind was partially offset by production and construction sinking 0.5% and 0.8%, respectively.

The UK’s total goods and services trade deficit expanded from £4.7 billion in the three months to February to £9.1 billion during the three month that ended in May, according to the Office for National Statistics.

Imports and exports of goods grew 5.9% and 6.2% while imports of services rose 1.4% and services exports dropped 0.1%. Goods imports from the European Union (EU) and non-EU countries rose 6.4% and 5.2% while goods exports to the EU and non-EU countries climbed 8.5% and 3.9%.

The Bank of Korea hiked its key interest rate by 25 basis points to 2.75%, a decision that was in line with expectations. In a statement following the central bank’s meeting last night, the organization said it believes inflation will stay above its 2% target and that price pressures will remain elevated due to the lag in when higher oil prices cause other items to become more costly. It also maintained that economic growth is continuing, a result, in part, of strong exports for AI. In the first three months of this year, gross domestic product expanding by 3.8%, which is providing room for further monetary tightening if required.

Construction companies broke ground on 239k residential units last month, missing the economist consensus estimate of 256k and falling from 253.1k in May, according to the Canadian Mortgage and Housing Corporation. When measured with the six-month moving average of the monthly seasonally adjusted annual, starts fell 2.8% from May’s paces. Starts increased in Montreal but contracted in Vancouver.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!