- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted January 15, 2026 at 1:05 pm

Bullish sentiments were revived on Wall Street following a robust earnings report from Taiwan Semi that bolstered optimism surrounding artificial intelligence. The blockbuster beat and raise sent the Nasdaq 100 about 1% off of its all-time high in a 2026 that has so far featured outperformance from the non-tech, cyclically oriented areas of the market that benefit from a pickup in economic growth. Emblematic of the rotation is the small-cap Russell 2000 jumping to a fresh record for a second consecutive session while the Dow Jones is close to achieving one of its own against the backdrop of those two indices already up 7.7% and 3% year to date. Investor enthusiasm was additionally propelled by simmering tensions between Washington and Tehran, as protests have been subsiding and President Trump has indicated that the US may not intervene, which pulled crude prices south by roughly 4% after a rally sparked by energy supply worries amidst elevated geopolitical risk. Safe-haven metals are also plunging as the path for peace has widened in the short-run, and silver and gold are now reversing from an earlier advance. But lower oil isn’t helping Treasuries, which are sinking on much stronger-than-expected unemployment claims, lifting the yield curve in bear-flattening fashion led by the monetary-policy sensitive shorter tenors. Indeed, rising evidence of stable labor conditions are dropping the odds of an April cut as fixed-income watchers appear increasingly confident that the next benchmark drop will come from Chair Powell’s successor in June. Elsewhere, the greenback is catching bids on heavier domestic borrowing costs and forecast contracts are seeing interest too. However, cryptocurrencies are experiencing modest losses.

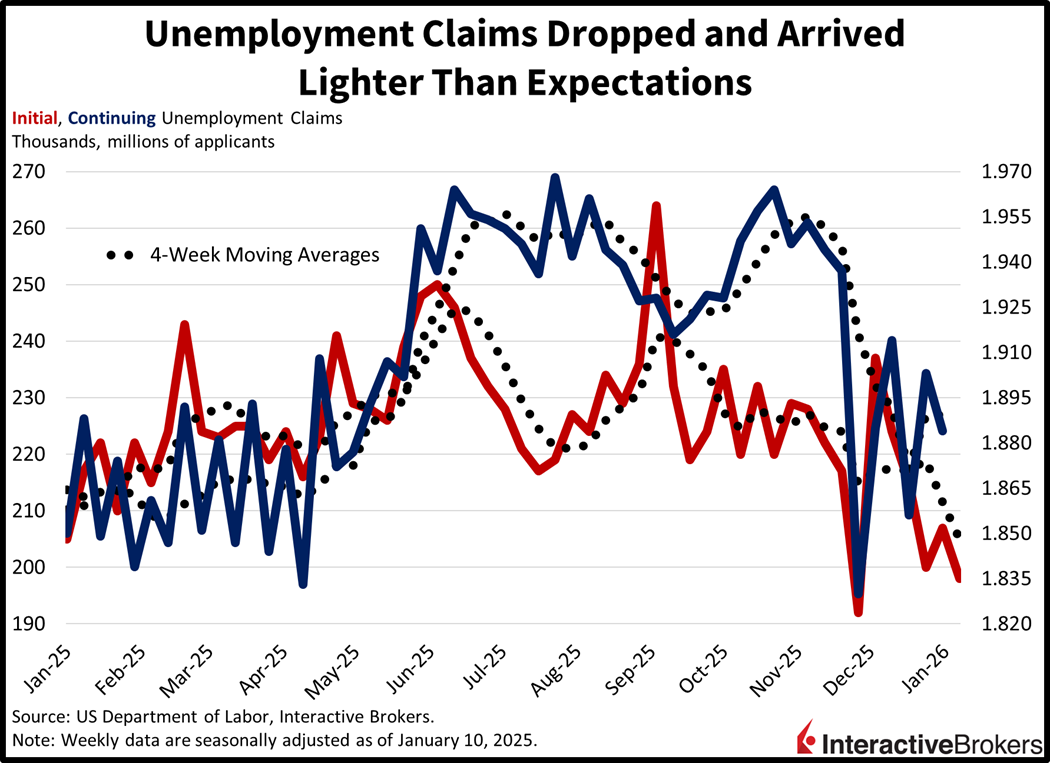

Unemployment claims dropped, were lighter than expectations and resulted in four-week moving averages sinking. The initial segment printed at 198k for the seven-day interval ending Jan. 10, softer than the 215k anticipated and the 207k from the prior period. Continuing filings for the week ended Jan. 3, meanwhile, arrived at 1.884 million, beneath the forecasted 1.890 million and the previous timespan’s 1.903 million. Four-week trends improved from 211.5k and 1.890 million to 205k and 1.889 million.

This morning’s developments are quelling investor concerns related to two of the most significant risks for markets in this new year. Taiwan Semi’s terrific earnings and the downside miss on unemployment claims are dismissing worries of whether the enormous investments in artificial intelligence will deliver buoyant returns as well as rising joblessness driving a retrenchment in consumer spending momentum. The positively received quarterly print boosted confidence that the tech sector still has legs to advance further despite 2026’s underperformance relative to cyclicals, while stable employment trends signaled that the cycle remains on solid footing and can support an environment conducive to continued expansions in corporate America’s profitability.

The Bank of Korea (BOK), in a widely expected decision, held its key interest rate at 2.5% yesterday and said it is likely to be done with monetary easing. The bank’s statements following previous meetings said the organization would consider if additional cuts were needed and the appropriate timing for such actions. That wording was removed yesterday, implying that policymakers are now focusing on financial stability at a time when a plunging won threatens to fuel import inflation. In a related matter, the BOK’s updated outlook reiterated policymakers’ recent views about the economy. The organization expects the Consumer Price Index to gradually decline from 2.1% in 2025 to 2%, although currency exchange rates and global oil prices are risks to this view. While non-information technology exports are likely to be slow this year, strong demand for the country’s semiconductors and domestic consumption are poised to boost activity.

Wholesale inflation slowed in Japan last month with the Producer Price Index matching the economists’ consensus estimates for increases of 0.1% month over month (m/m) and 2.4% year over year (y/y) after ascending 0.3% m/m and 2.7% y/y in November.bExports fetched 1.8% m/m and 4.9% y/y more in December while purchases of items from abroad were 1.1% more costly relative to November. The y/y metric depicted no change. Broadly speaking, nonferrous metals led the m/m ascent, climbing 0.2% m/m. Other categories increased less than 0.1% except for the petroleum and coal group, which slipped 0.3%.

Euro area industrial production was up 0.7% m/m and 2.5% y/y in November. Economists anticipated 0.5% m/m and 2% y/y growth following October’s gains of 0.7% and 1.6%.

For the m/m print, output of capital goods led, growing 2.8%. It was followed by a 0.3% ascent of consumer goods. Energy, durable consumer goods and non-durable consumer goods output, conversely, slipped 2.2%, 1.3% and 0.6%, respectively. Relative to November 2025, output of capital goods, non-durable consumer goods, intermediate goods and energy were up 3.6%, 3.4%, 1.1% and 0.5%. Durable consumer goods, however, sank 2.1%.

Sales in Canada’s wholesale and manufacturing segments during November sank more than anticipated. Purchases on a wholesale level slipped1.8% m/m while the economist consensus expectation was for a 0.1% advance. In October, volume was up 0.4%. In the manufacturing segment, sales fell 1.2%, slightly worse than the estimate for a 1.1% decline and October 1% contraction.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. Eligibility to trade in digital asset products may vary based on jurisdiction.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!