- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted March 25, 2026 at 12:59 pm

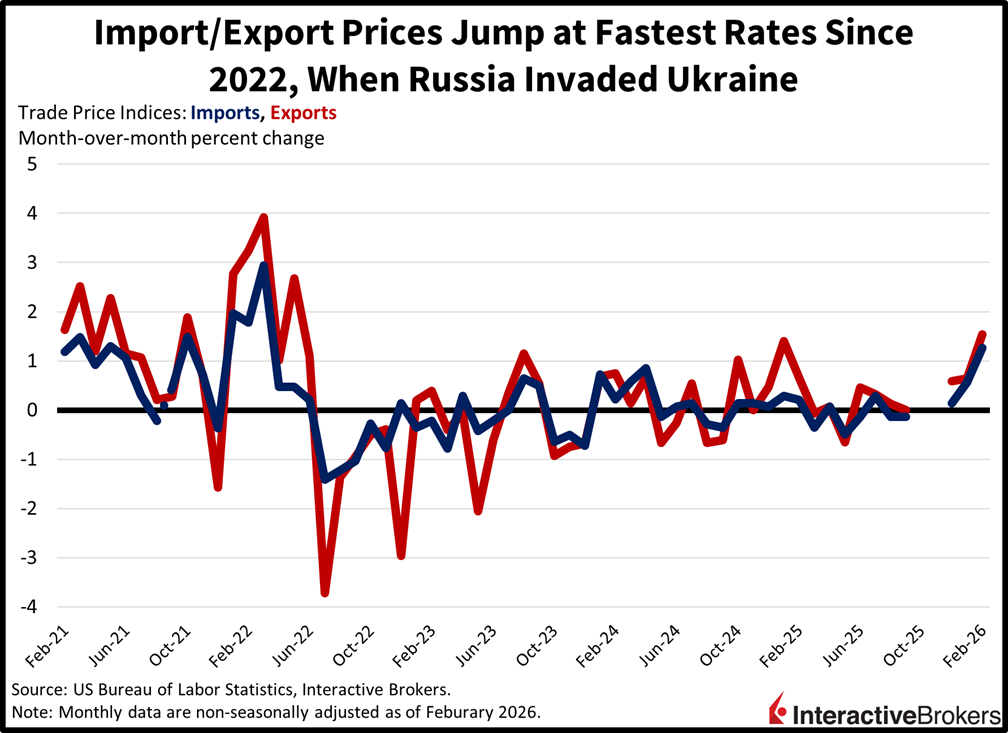

Stocks are continuing their recovery today as persistent White House remarks signaling positive negotiations with Tehran bolster confidence that a ceasefire may be around the corner. Treasuries are joining the advance as well after retreating yesterday against the backdrop of doubts that peace in the Middle East will come to fruition in the near future. But WTI is rising modestly as Iran continues to play hardball with the Trump administration by both denying that productive conversations have taken place and rejecting the US 15-point offer that would end the conflict. In the meantime, it’s increasingly a single-variable market, as crude oil costs are the key factor driving buying and selling decisions on Wall Street. In equities, the S&P 500 was fiercely rejected this morning at the 200-day moving average despite all major benchmarks, sectors and subcategories climbing, a critical technical level that could support a stronger rebound for investors. The yield curve is supportive, however, with the complex descending in bull-flattening motion led by duration, a sign that fixed-income watchers do indeed see progress with foreign relations as they dial down inflation expectations, even as import and export prices rose to 4-year highs in February according to a BLS report released prior to the opening bell. The greenback and commodities are catching safe-haven bids, while cryptocurrencies and forecast contracts additionally experience engagement. Volatility levels remain elevated although premiums are slipping in consideration of traders as a whole seeing a glimpse of light along the geopolitical tunnel.

Import and export costs jumped at their fastest rates since 2022, when Russia invaded Ukraine and oil charges soared. The 1.3% and 1.5% month-over-month (m/m) February climbs were well above the 0.5% median estimates and the 0.6% rate of January increases on both fronts. Fuel and non-energy imports rose 3.8% and 1.1% m/m, while agricultural and non-farm exports climbed 0.7% and 1.7%.

Despite President Trump signaling that a ceasefire could be around the corner, communication from Tehran amidst continued violence in the Middle East suggests that the two sides remain far apart from an agreement. Messages from Iranian leaders have disappointed investors with the country indicating that it would not accept the US peace deal, and furthermore, government officials continuously deny that any discussions are taking place. But in Washington, political pressure is mounting against the backdrop of pain at the pump hurting everyday Americans, while stock market volatility driven by deteriorating corporate fundamentals, particularly margins, threatens to hamper the expenditure patterns of the wealthiest consumers. The K-shaped dynamics of the past few years have lifted the higher-earners towards comprising a rising share of economic performance, and if this group curtails its wallets and pocketbooks, then slowdown risk rises meaningfully at the same time that rate cut prospects have essentially been thrown out the window. The adverse environment has weighed on the GOP’s chances regarding this November’s midterm elections, with even the Senate up for grabs. The shift in probabilities is monumental, because at the beginning of the year the Republicans had an approximately 75% likelihood of maintaining their majority, however, the odds are now near a coin-flip for the upper chamber.

Inflation in Australia eased in February with the Consumer Price Index (CPI) climbing 3.7% year over year (y/y) following January’s 3.8% gain, according to the Australian Bureau of Statistics. Economists anticipated that prices would climb at the same pace as in January. On a m/m basis, the gauge was up 0.2%, a substantial deceleration from January’s 0.5% jump.

Housing was up 7.2% y/y. Australians were hit with higher electricity costs with funding for an energy relief bill having ended. Expenses for new homes and rents also climbed. Other categories with substantial y/y gains and the extent of their changes included the following:

Other categories increased at lower rates with the exception of transport, which experienced a 0.2% y/y drop.

After dropping 0.5% m/m in January, the UK’s CPI climbed 0.4%, matching the economist consensus estimate. For the y/y result, the gauge was in-line with January’s 3% ascent, arriving as expected. The CPIH, which includes housing, however, was slightly hotter with a 3.2% y/y gain but its monthly jump of 0.4% matched the CPI. Meanwhile, core inflation, which excludes certain items with volatile prices, strengthened from 3.1% y/y and -0.6% m/m to 3.2% and 0.6%, respectively. Within the CPIH, furniture and household goods experienced the strongest price pressures with the segment costing 1.7% more m/m. The restaurant and hotels category, the clothing and footwear group and the miscellaneous goods and services segment followed with hikes of 1%, 0.6% and 0.6%.

UK businesses in February experienced stronger input cost pressures but they fetched 0.5% less for their products on the wholesale market than during January, according to the Producer Price Index. The decline was considerably beneath the economist consensus estimate for a 0.3% m/m gain. Price pressures, furthermore, weakened on a y/y basis with tags growing only 1.7% compared to the 2.5% jump in January and the economist estimate of 2.6% y/y.

Input costs, in contrast, climbed 0.5% y/y and 0.8% m/m after January’s 0.4% and 0.3% results. Economists anticipated y/y and m/m increases of 0.4% and 0.5%. Input inflation relative to the year-ago period occurred in 8 out of 10 product groups with the prices of metals and non-metallic mineral products category rising by 4.2%. Parts and equipment, additionally, were up 0.8%. Crude oil provided partial relief, declining 12.6% after a 22.6% January hike.

The South Korea Composite Consumer Sentiment Index sank 5.1 points to 107 in March with declines occurring in most of the gauge’s subcategories as follows:

Future household spending was an exception with an unchanged level of 111.

Consumers anticipated a 2.7% inflation rate for the remainder of 2026. Inflation for the three-year and five-year ahead periods is expected to be 2.6% and 2.5%.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. Eligibility to trade in digital asset products may vary based on jurisdiction.

Related Articles

")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!