- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted February 24, 2026 at 12:53 pm

Solid economic data are supporting a Turnaround Tuesday in stocks as strengthening hiring statistics from ADP coincided with a beat on consumer confidence. Investor sentiment was hurt yesterday by confusion regarding the road ahead for tariffs, as the White House vowed to maintain restrictive trade measures. Thankfully, Wall Street has grown accustomed to the back-and-forth characteristics of the Trump Administration and top of mind today is that the cycle’s foundation appears healthy. As a result, equities are recovering broadly with consumer discretionary, technology and industrials leading amidst all four major benchmarks advancing on the session. However, the better-than-expected reports are driving the greenback and yields modestly higher, with the bear-flattening move across the curve led by the monetary policy sensitive shorter tenors. Rates are climbing because improving jobs figures are weakening the argument from dovish voting members of the Fed that are pointing to softening labor trends to justify cuts. Elsewhere, commodities ex copper are sinking on a lack of safe-haven demand and a stronger dollar, and so are volatility protection instrument premiums as traders unwind hedges and go on offense. The lift in animal spirits, furthermore, is raising interest in forecast contracts but cryptocurrencies can’t seem to catch a break despite the risk-on mood.

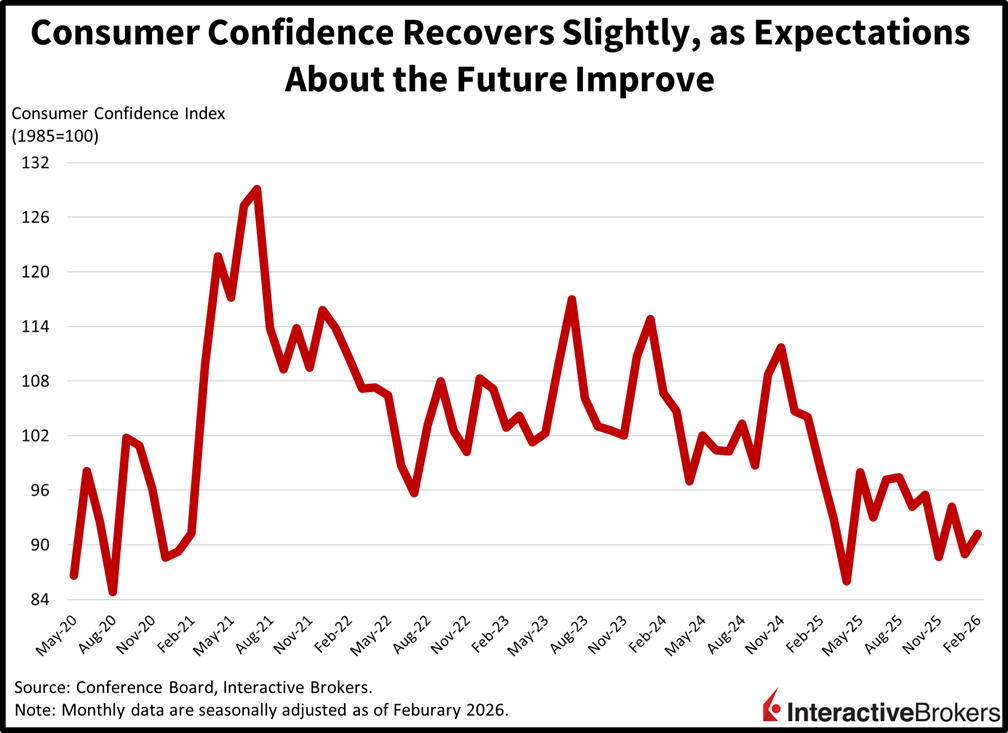

Improving sentiments concerning the future lifted consumer confidence this month, even as perspectives about the present weakened. The headline figure of 91.2 exceeded the projected 87 and January’s 89, however, it was well below the 2025 average of 95. The sub-indices for current conditions and longer-term expectations shifted in bifurcated fashion, from 121.8 and 67.2 to 120 and 72. Households remained worried about inflation, tariffs, immigration restrictiveness and politics, while concerns of labor market opportunities, income prospects and business possibilities lightened to an extent. Additionally, anticipated price pressures were unchanged, while survey respondents were bullish on stocks while believing that interest rates will stay elevated.

Private sector payrolls increased by an average of 12.75k workers in each of the four weeks during the period ended Feb. 7, according to ADP. It was the strongest print since Oct. 29 and marks a persistent hiring acceleration that began in early January. The positive trend is strengthening investor confidence regarding the buoyancy of the cycle.

The stage is set for AI and tariffs to remain turbulent themes that can amplify bumpiness on Wall Street while robust economic data can suppress volatility. Indeed, the significant capital expenditures committed by corporate America are under careful watch of stock and fixed-income players on the public side, as well as participants that are increasingly exposed to the modern technology via private markets through both equity and credit. The fluctuations of the risk-reward calculations and the financial return profiles are poised to keep investors on a jarring ride, just as President Trump’s tariff policies generate confusion and unease for traders. But ongoing evidence signaling buoyant consumption, improving sentiment, faster hiring and strengthening activity can continue to offset risks, serving as a reason to scoop the ice cream.

The Confederation of British Industry (CBI) Distributive Trades Survey fell from -17 in January to -43 for this month, a much worse showing than the -27 anticipated by a consensus of economists. The Confederation reports that retail sales in the year to February sank at the fastest pace since mid-2023, although the contraction is expected to decelerate in the coming month. Meanwhile, employment slipped and selling prices climbed. Retailers also expect to curtail capital expenditures, and persistently weak demand is expected to weigh on sentiment.

China’s central bank held its 1-year and 5-year key rates at 3% and 3.5% yesterday as the country focuses on measures other than monetary policy to juice domestic demand. The People’s Bank of China decision extends the current costs of capital for the 10th consecutive month as the country struggles with sluggish consumer spending, excessive manufacturing capacity and a glut of residential real estate. Meanwhile, China’s currency has been strengthening, potentially creating a headwind for export volumes. Domestically, new home prices have declined year-over-year (y/y) every month since last August and wholesale prices have been softening as consumer spending has weakened. Additionally, in the fourth quarter, gross domestic product grew only 4.5% y/y in the final three months of last year, its slowest pace in approximately three years. After having mixed results with trade-in subsidies to boost purchases of large-ticket items, officials recently launched incentives for consumers to spend on services, such as travel and sporting events.

Manufacturing sales in Canada sank 3.3% month over month (m/m) in January, the third decline in the past four months, according to preliminary data from Statistics Canada. The drop, a reversal from the 0.6% gain in December, was driven primarily by weakness in the transportation equipment and machinery subsectors.

Railroad freight volume fell 2% y/y in December with fewer shipments in iron ore and coal hurting overall demand. For the full year, railroad freight sank 0.2% despite strong levels of grain shipments during a bumper crop-production year, helping to offset a decline in demand from US rail connections.

South Korea’s preliminary Producer Price Index was up 0.6% m/m in January, a slightly stronger gain than the 0.4% jump in the final month of 2025. The y/y growth rate, however, was unchanged from December’s 1.9%. For the m/m print, the agricultural, forestry and marine products category and the services classification had the largest sticker increases, gaining 0.7% each. Manufacturing products followed at 0.6% while electric power, gas, water and waste were flat. Among subcategories, financial and insurance was 4.7% more costly than in December and basic metal products were 3% higher.

A strong domestic equity market and demand for semiconductor chips pushed South Korea’s Consumer Confidence gauge from 110.8 in January to 112.1, its highest level in three months, according to the Bank of Korea. A reading of 100 is the threshold between negative and positive. The biggest gain occurred in assessments of current economic conditions and expectations as consumers expressed optimism regarding export demand and the stock market. Conversely, efforts by the government to shore up the residential real estate market failed to prevent a decline in housing sentiment.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. Eligibility to trade in digital asset products may vary based on jurisdiction.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

")

Citizenships some company Bangladesh bogura destec sajahanpur noymailjamalpur