- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted January 14, 2026 at 1:01 pm

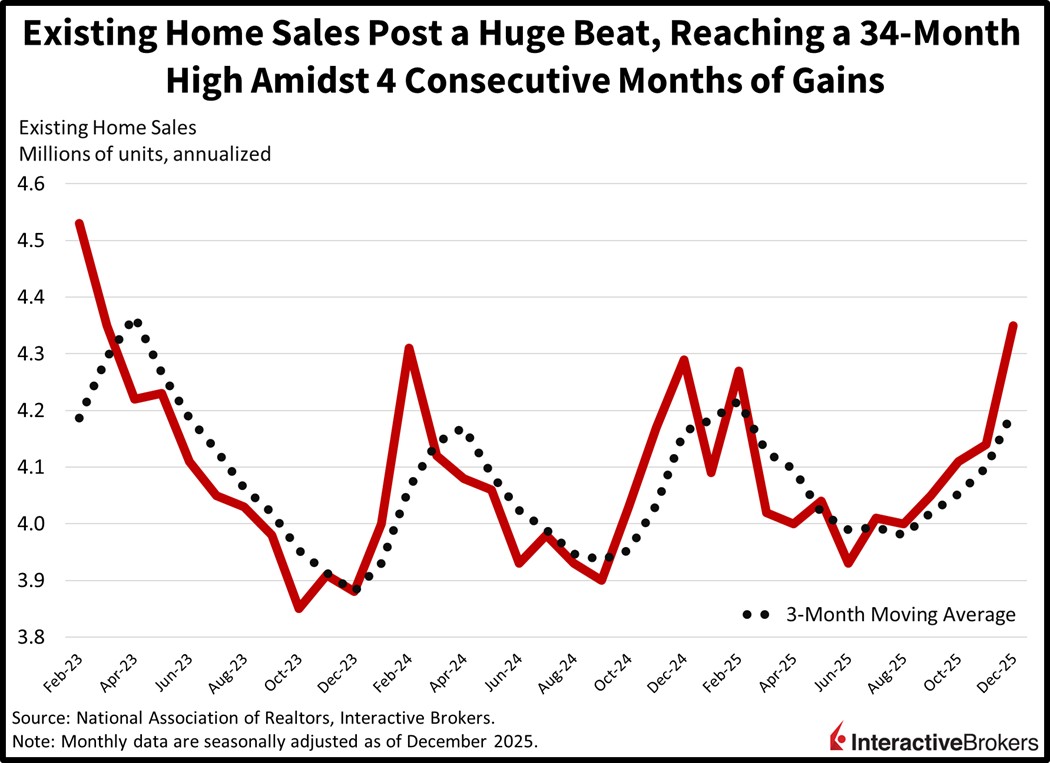

Mounting geopolitical uncertainty, a postponed Supreme Court decision on tariffs and lackluster earnings results from big banks are blowing risk-off winds throughout Wall Street today. Stocks are poised to suffer losses for two consecutive sessions for the first time this year as investors clamor for safe-haven holdings against the backdrop of a low-impact economic calendar featuring stale PPI and retail sales data from November and a timely read on housing transactions for December. Participants are indeed guiding their decisions from profitability reports and international developments and are responding by reaching for Treasuries with a long-end, bull flattener bias while doing some aggressive commodity buying, as copper, gold and silver reach fresh records. Meanwhile, crude oil is trading at its loftiest price of 2026 on worries that supplies could be disturbed due to tensions in Tehran. Despite the three major domestic benchmarks sharply lower though, there’s interest in shares in the defensive consumer staples, utilities and health care sectors in light of their relatively stable characteristics. And in the cyclical space, energy, materials are appreciating on widening margin profiles driven by heavier selling costs while real estate is climbing in response to lighter mortgage rates amidst a huge beat on existing home closings which featured the fourth consecutive increase, sending the headline figure to a 34-month high. Additionally, volatility protection instruments and put options are seeing pricier premiums as traders rapidly add hedges to portfolios. Folks are also gravitating to alternatives like cryptocurrencies and forecast contracts with Bitcoin and Ethereum and “Yes/No” trades catching bids while subdued yields weigh on the greenback.

Decelerating prices combined with lighter interest costs generated a huge beat in existing home sales for December. The fourth consecutive report featuring an uptick saw the headline figure jump to its strongest pace in 34 months, or since February 2023. Indeed, the 4.35 million seasonally adjusted annualized units flew past expectations of 4.21 million and improved by 5.1% month over month (m/m) from November’s 4.14 million. The South, West and Northeast bolstered results with increases of 6.9%, 6.6% and 2% m/m, while the Midwest offset some of the progress, sliding 2% during the period. Single-family homes saw closings inch up 5.1% while the condominium/cooperative segment climbed a higher 5.3%. Meanwhile, factors that propelled transactions were values rising just 0.4% year over year (y/y) to a median level of $405,400, inventories increasing 3.5% y/y and subdued mortgage rates, which fell from 6.72% to 6.19% y/y.

With limited economic data remaining this week, investors will continue analyzing incoming earnings reports and watching international developments to gauge the appropriate amount of portfolio risk. So far, it appears Wall Street is placing a high bar on corporate America’s quarterly results and forward guidance based on the reactions in the first few days of the reporting season. Against the backdrop of elevated valuations and mounting geopolitical turbulence from multiple corners of the world, shareholders want to see stellar profitability and buoyant future expectations prior to accumulating more equity. And unfortunately for stock bulls, a potential rally following a Supreme Court decision to block President Trump’s tariffs expected today was postponed. The expected action, which ForecastEx participants price out at 70%, would raise the likelihood of significant fiscal stimulus reaching the economy while a greater chance of levy refunds would shore up balance sheets and bolster bottom lines in the short run. Conversely, however, it would weigh on onshoring ambitions and lift long-end Treasury yields on heavier term premiums driven by a worsening deficit.

China’s annual trade surplus hit an all-time high of $1.19 trillion in 2025 and jumped 20% from the preceding year, a result of the country expanding into higher value manufacturing and improving relationships with buyers in Europe and Southeast Asia. In December, furthermore, exports climbed 6.6% y/y, exceeding the economist consensus prediction that shipments would increase only 3% and accelerating from the 5.9% gain in November.

Imports also strengthened. Shipments from foreign providers were 5.7% higher y/y after growing only 1.9% in the preceding month. Economists anticipated a 0.9% increase.

While US buyers slashed purchases by 20% in 2025, the following regions increased their Chinese imports by the stated amounts:

The Reuters Tankan Index dropped from 10 in December to 7 with manufacturers’ sentiment falling, a reaction to weak orders from foreign markets. The oil and ceramics category declined the most, tanking 25 points to zero, while the steel sector slipped 11 points to minus 44. Confidence in the chemicals industry also weakened, sinking 5 points to plus 6. Separately, a gauge of services providers’ descended 1 point with the wholesaling and retailing classifications sinking 10 and 7 points. Some survey respondents observed a decline in tourists from China, a result of growing tensions between the two countries. Conversely, transport, information and real estate strengthened.

South Korea’s unemployment rate spiked, climbing from 2.7% in November to 4% last month, according to the Ministry of Data and Statistics.It was the highest December reading in 25 years. During the month, 1,217,000 individuals were out of work, up by 103,000 from the year-ago period. The Ministry of Data and Statistics said the weakness in accommodation, foods services, manufacturing and construction contributed to the rise in joblessness, especially among younger individuals who tend to be employed in those sectors.

Approvals for proposed construction projects in Australia climbed 20.2% y/y and 15.2% m/m in November, matching the economist consensus estimates and reversing from October’s 1.1% y/y and 6.1% m/m contractions. Among approvals, private houses were 1.3% higher, which also matched estimates following a decline by the same amount in October.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. Eligibility to trade in digital asset products may vary based on jurisdiction.

Options involve risk and are not suitable for all investors. For information on the uses and risks of options, you can obtain a copy of the Options Clearing Corporation risk disclosure document titled Characteristics and Risks of Standardized Options by going to the following link ibkr.com/occ. Multiple leg strategies, including spreads, will incur multiple transaction costs.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

Interactive Brokers LLC is a CFTC-registered Futures Commission Merchant and a clearing member and affiliate of ForecastEx LLC (“ForecastEx”). ForecastEx is a CFTC-registered Designated Contract Market and Derivatives Clearing Organization. Interactive Brokers LLC provides access to ForecastEx Forecast Contracts for eligible customers. Interactive Brokers LLC does not make recommendations with respect to any products available on its platform, including those offered by ForecastEx.

This is commentary on economic, political and/or market conditions within the meaning of CFTC Regulation 1.71, and is not meant provide sufficient information upon which to base a decision to enter into a derivatives transaction.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!