- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted July 9, 2026 at 1:32 pm

A $50 billion lift in Micron’s domestic capital expenditure plans is reviving the semiconductor trade by strengthening the case that the AI build-out remains in its early innings. The announcement is bolstering tech enthusiasm and has the Nasdaq 100 leading benchmark gains amidst all of the major indices advancing alongside 8 of the 11 sectors in the green. The rebound is transpiring even as the Magnificent 7 names fail to participate much in this session’s advance due to uncertain return prospects tied to their significant investments in the modern infrastructure. Investor sentiment is also improving as a result of plummeting crude prices as participants gauge that President Trump doesn’t want intense Middle East hostilities occurring prior to a midterm election in which the Republicans carry just a narrow lead in sustaining their Senate majority. Those tumbling oil and natural gas costs, meanwhile, are helping to loosen financial conditions via subdued Fed hike expectations, plunging yields and a depreciating greenback, factors that are conducive to buoyant stock buying. Non-energy commodities and cryptocurrencies are additionally benefiting from the resurgence in animal spirits, however, with precious metals and copper especially driving the train. Hedging interest is waning in light of the risk-on attitude on Wall Street, with volatility protection instruments seeing lighter premiums. Conversely, prediction markets are catching bids.

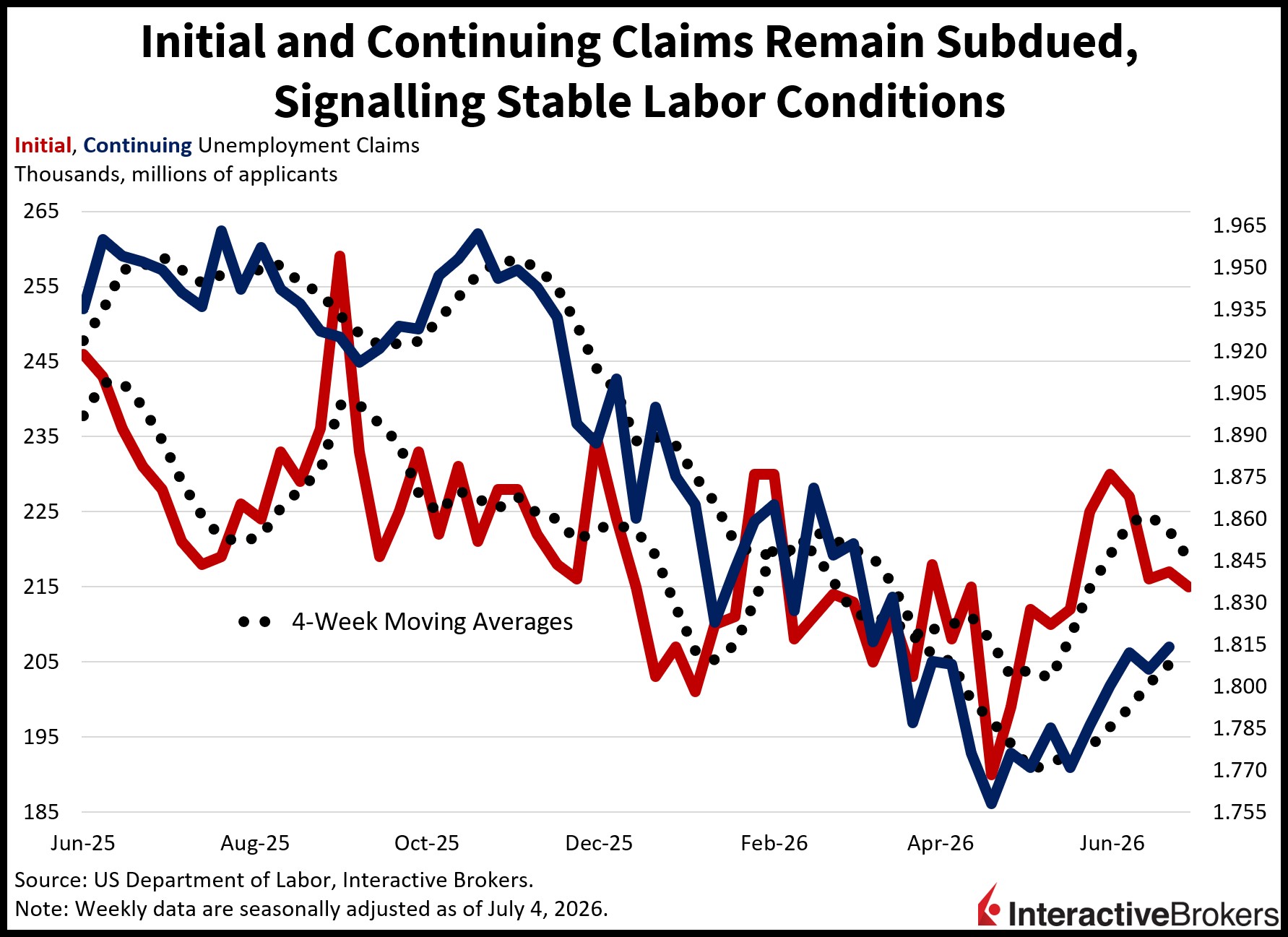

Claims for unemployment benefits for the past two-week period continued to depict a stable job market with employers refraining from layoffs. Initial filings declined to 215k during the interval that ended July 4, dropping below the 218k economist consensus estimate and the preceding period’s 217k. Continuing applications rose modestly to 1.814 million through the time span culminating on June 27, considerably below the 1.820 million anticipated. In the preceding period, continuing claims totaled 1.80 million. Four-week moving averages shifted in bifurcation fashion from 222.5k and 1.801 million to 218.7k and 1.808 million.

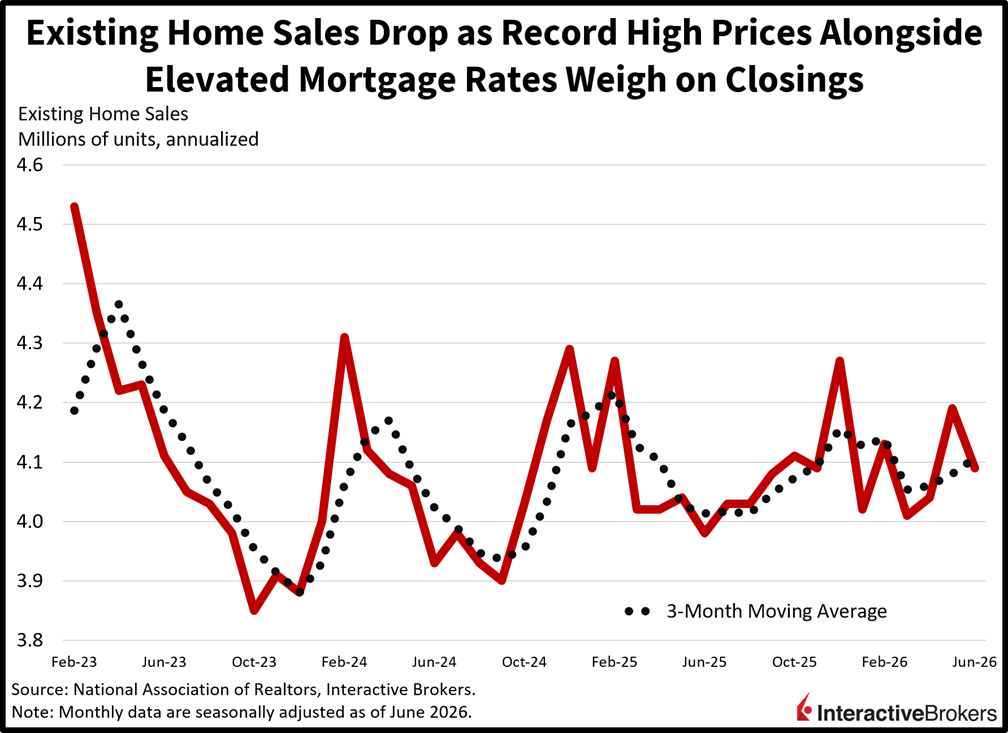

Existing home sales fell in June, snapping a two-month streak of increases as record-high prices pushed potential buyers out of the market, according to the National Association of Realtors. The 4.09 million seasonally adjusted annualized units (SAAU) sold was a 2.4% month-over-month (m/m) decline and below the projection for a repeat of May’s 4.19 million transactions. It was also a reversal from May’s 3.7% m/m increase. The weakness was broad as follows:

Among regions, the Northeast was an outlier, posting a 2.1% m/m increase. In other regions, the Midwest, South and West experienced declines of 3%, 3.6% and 1.3%, respectively. Despite the contraction in property deeds switching hands, inventory fell 0.6% from May. Meanwhile, the median existing home price climbed 1.8% year over year (y/y) to $460,600, an all-time high. The average mortgage rate, furthermore, at 6.49%, remained nearly unchanged from 6.44% in May. Nevertheless, it was down from 6.82% in the year-ago period.

Yields are far too elevated at the long end of the curve at this juncture and bonds have several paths to meaningful appreciation as follows:

Consumer price pressures eased in China last month, but wholesale inflation intensified, marking the fifth consecutive month in which businesses fetched more for their products rather than having to lower their stickers.

The CPI was down by 0.3% m/m after falling 0.1% in May. An economic consensus called for prices to slip 0.2%. Relative to the year-ago period, consumers dished out 1% more compared to the 1.2% y/y climb in May. Economists anticipated a 1.1% pace. The June core CPI, which strips out food and energy, matched the broader index’s result after hitting 1.1% in the preceding month. June’s y/y headline was dampened by food prices falling 1.6% after sinking 1.7% in the preceding month. Other items climbed 1.5%, a deceleration from 1.9% in May. Within that category, industrial sticker growth eased from 3.9% to 2.9%. Services became 0.8% more expensive.

Gate prices, meanwhile, were up 4.1% y/y, matching the economist consensus estimate and accelerating from 3.9%. When compared to May, however, prices were down 0.3%, a result of softer global oil prices. The y/y print reflects the elevated base effect, or a comparison to a low number y/y. Indeed, wholesale prices declined every month from October 2022 until February of this year, and in the year-ago period, gate prices registered a 12-month 3.6% decline. Coal mining, electrical machinery, ferrous metals and electronics also contributed to the higher y/y print.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Futures, event contracts, and forecast contracts are not suitable for all investors. Before trading these products, please read the CFTC Risk Disclosure. For a copy, visit our Warnings and Disclosures Page.

Investments in certain commodities (precious metals) may be subject to significant price volatility and often involve risks related to market fluctuations, liquidity constraints, geopolitical events, and changes in global economic conditions that could adversely affect their value.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. Eligibility to trade in digital asset products may vary based on jurisdiction.

Municipal Bonds are only available from Interactive Brokers for IBKR LLC, IBKR Canada, IBKR Hong Kong, IBKR Australia and IBKR Singapore entities.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!