- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted March 11, 2026 at 12:56 pm

Markets are falling even with this morning’s CPI arriving in line with expectations and IEA members agreeing to provide 400 million barrels of oil from strategic reserves. Stocks are dropping broadly and yields are soaring throughout the Treasury curve as WTI crude remains above $87. Progress in the Middle East amidst cooperation amongst Western countries has certainly helped oil cool off from the $119.48 level reached on Monday; however, the commodity is still up 54% year to date, illustrating the ongoing risk of an extended conflict which would likely be accompanied by transportation constraints along the Strait of Hormuz and upside risks to inflation. In trading, every equity sector and major benchmark is lower minus energy and technology, as the greenback strengthens as a result of tightening financial conditions stemming from loftier interest rates. Elsewhere, non-energy commodities are facing selling pressure, but volatility protection instruments are catching bids in light of defensive winds on Wall Street. Cryptocurrencies and forecast contracts are additionally experiencing engagement.

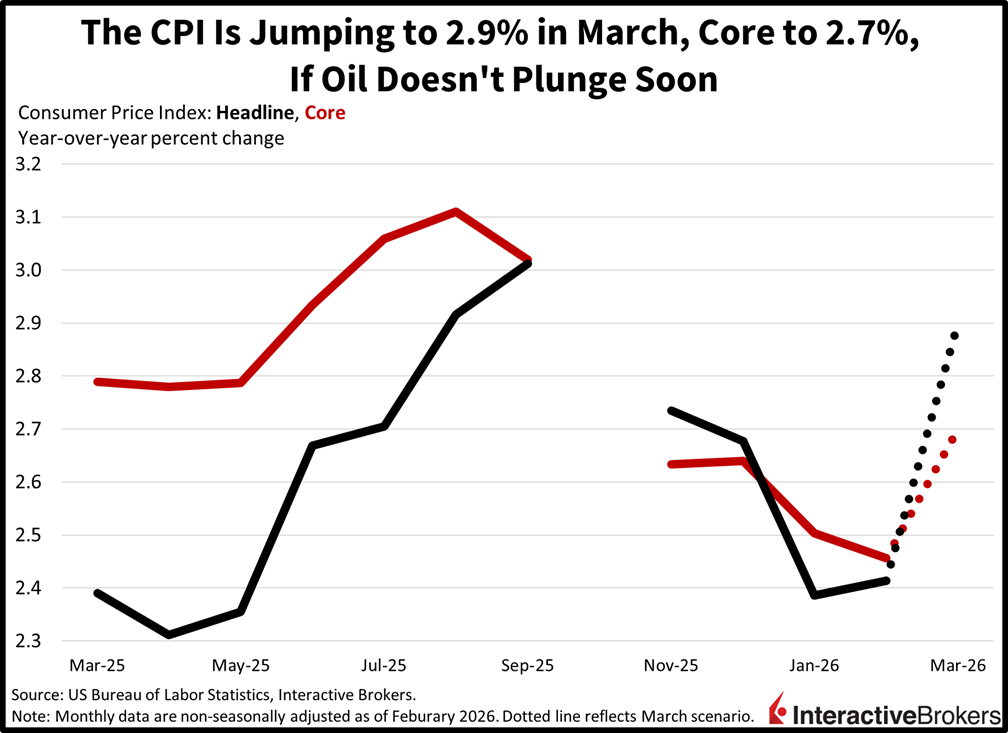

February inflation was in line with forecasts and roughly unchanged from the preceding month as subdued housing costs and declining used car prices offset the impact of groceries, medical care and apparel becoming much more expensive, according to the Consumer Price Index (CPI). The gauge was up 2.4% year over year (y/y) and 0.3% month over month (m/m). The y/y print matched January’s result while the m/m rate inched up from 0.2%. Both February metrics were consistent with consensus estimates.

Within the m/m gauge, shelter increased 0.2% and had the largest impact on the headline. Food and energy, furthermore, climbed 0.4% and 0.6%. The food at home and away from home components increased by 0.4% and 0.3%, respectively. In other areas, apparel, medical services and transportation were 1.3%, 0.6% and 0.2% more expensive m/m.

The Core CPI, which excludes energy and food due to the items’ volatile prices, depicted easing m/m inflation and a y/y print that matched January’s result. When compared to January, the gauge was 0.2% higher, exactly the same as the consensus estimate and softer than the preceding print depicting a 0.3% ascent. The y/y core result, at 2.5%, was consistent with the economist consensus and January’s print.

WTI crude oil has advanced over 34% y/y even after the dramatic pullback from the jump to $119.48 and it will be almost impossible to keep the CPI in the low 2s unless we see a plunge in the critical commodity’s price. For this reason, Fed watchers are now expecting just one rate cut in 2026, which has derailed investor sentiment regarding cyclical equity areas that benefit the most from monetary policy accommodation amidst a reaccelerating economy. The problem with elevated energy costs is that they are not only inflationary, but they also reduce the capacity for consumers to spend on goods and services and for firms to hire and initiate capital expenditures, as more funds must be allocated toward fuel. An increasingly cautious outlook paired with expectations of a tighter central bank has reversed powerful year-to-date rallies in the Dow Jones Industrial and Russell 2000 indices, which were offsetting declining AI enthusiasm that continues to weigh on the Nasdaq 100 and S&P 500 benchmarks. The good news, however, is that valuations have decreased substantially against the backdrop of flat stock performance during the past six months, and favorable developments in the Middle East have the potential to generate a meaningful advance from here.

Wholesale price pressures in Japan eased during January with the preliminary Producer Price Index down 0.1% m/m and up only 2% y/y. The results showed gate price inflation slowing from December’s 0.2% m/m and 2.3% y/y ascents. The metrics were also below the m/m and y/y economist consensus estimates for 0.1% and 2.2% hikes.

On a yen basis, exporters boosted prices by 1.2% m/m and 9.5% y/y while importers experienced cost climbs of 0.1% and 2.8% at a time when the country’s currency is weakening. More broadly, m/m price gains within Japan were led by petroleum and coal products, which became 3.1% more costly after sinking 2.5% in December. Other categories with notable price gains and the extent of the changes were as follows:

The impacts of those results were more than offset by the following categories that experienced price declines as stated:

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. Eligibility to trade in digital asset products may vary based on jurisdiction.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!