- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted March 16, 2026 at 1:04 pm

Glimpses of progress on the Strait of Hormuz featuring a few ships that have made it across the critical passage are sparking a Wall Street recovery to begin this new week. The resulting decline in oil prices is generating a broad advance in stocks and fixed income with every sector, sub-category and major benchmark gaining in equities while yields plunge throughout maturities. But the Treasury rally is more pronounced at the long-end, as duration benefits from softening inflation expectations, sinking the complex in bull-flattening fashion. There’s still a heavy amount of uncertainty as to what happens next; however, President Trump is attempting to gather other nations to help Washington in securing the waterway and is working on a plan to have the US Navy escort certain vessels through the Gulf. Meanwhile, members of the administration, including Secretary Bessent, looked to bolster market confidence by opining that the world will be better off when the conflict ends and that crude should fall to below $80 as a result; it’s currently around $95. On the economic data front, industrial production and homebuilder sentiment modestly beat estimates, which was also somewhat supportive of this Monday’s rebound. Elsewhere, lighter domestic borrowing costs are weighing on the greenback, risk-on attitudes are lowering premiums on volatility protection instruments, cryptocurrencies and forecast contracts are catching bids and non-energy commodities are climbing overall.

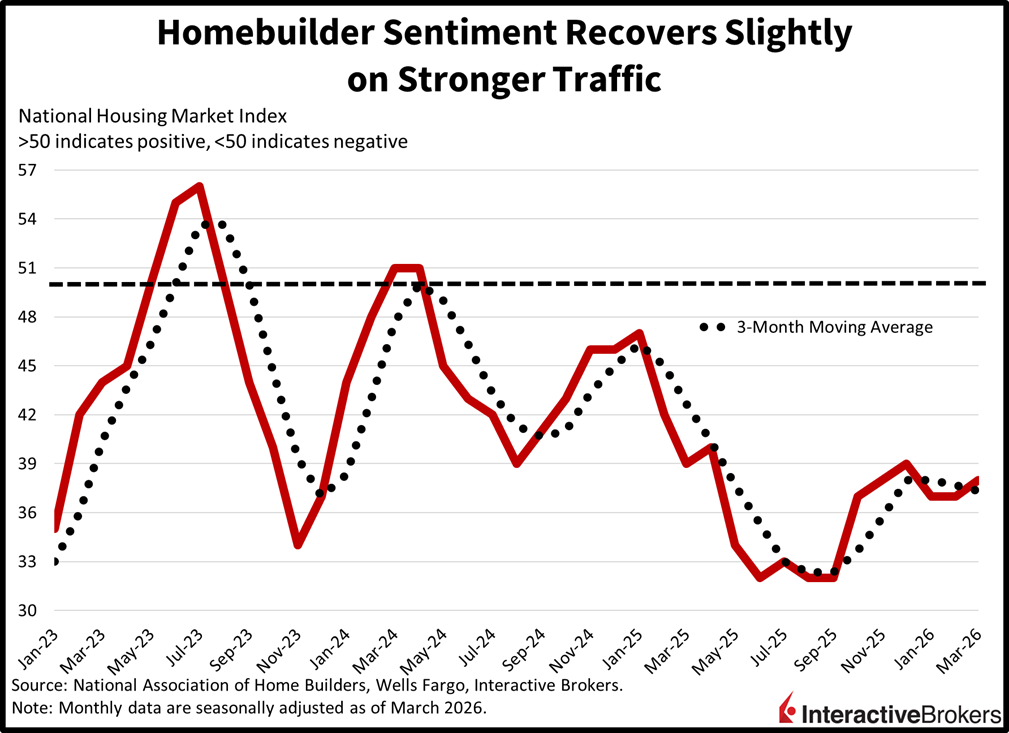

Homebuilder sentiment improved slightly this month on broad progress across categories even though the result remained extremely weak by historical standards. The NAHB/Wells Fargo headline index of 38 was modestly above the 37 expected, which would have been the same figure from February. The current sales, transaction outlook, and prospective buyer traffic components all rose, climbing from 41, 47 and 22 to 42, 49 and 25. Throughout regions, the Midwest and South experienced increases of 5 and 1 to land at 47 and 36, offsetting the 1-point drop in the Northeast, which placed the region at 42. The West arrived unchanged, meanwhile, at 30, which printed well below the positive-negative threshold of 50. Going under the hood, 37% of suppliers cut prices in March while the use of incentives was at 64%, compared to 36% and 65% from the prior period.

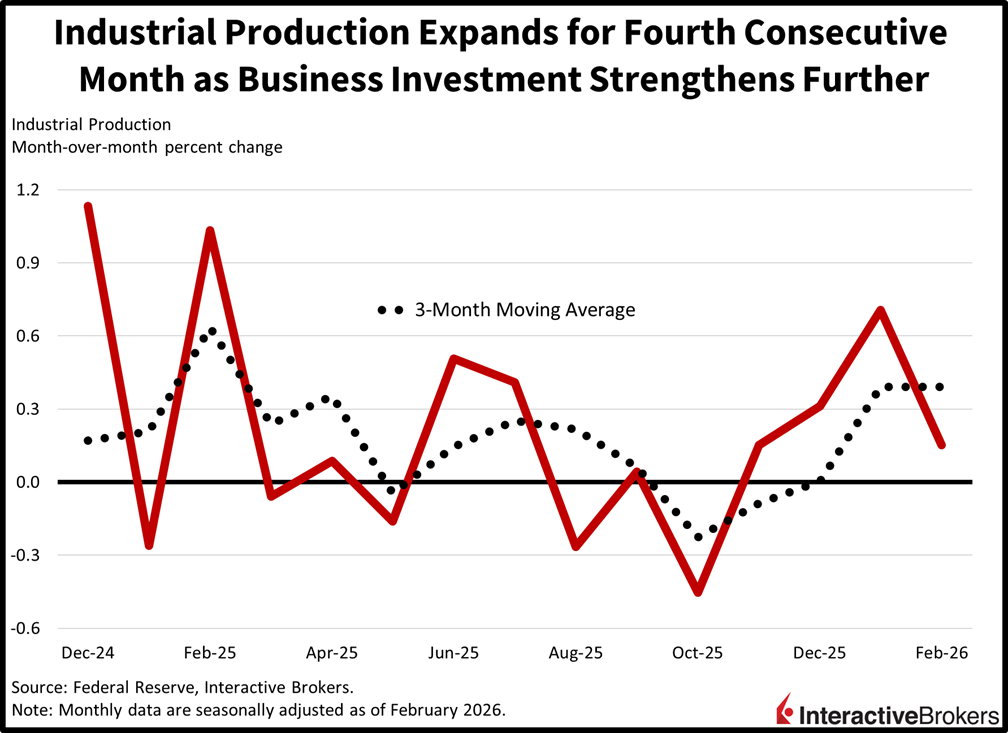

Industrial production expanded for the fourth consecutive month in February, pointing to the manufacturing sector potentially entering an extended period of expansion. The 0.2% month-over-month (m/m) and 1.4% year-over-year (y/y) growth in the headline figure slowed from the 0.7% and 2.3% climbs in January, but the monthly result beat estimates calling for just 0.1%. Goods output and mining rose 0.2% and 0.8% m/m, offsetting a 0.6% decline in utilities. And amongst market groups, materials and business equipment increased 0.3% and 0.2% m/m, construction sank 0.2%, and consumer products and nonindustrial supplies were unchanged during the interval.

To the potential satisfaction of equity and fixed-income investors, President Trump appears to be in deal mode as he pulls levers to try and quell the jump in oil prices. The White House is speaking with other nations so they can help in the conflict, has communicated with international agencies to raise the supply of crude, and has demanded that Tehran surrender. Meanwhile, questionable rumors of a ceasefire have inspired controversy in both Iran and the US. The commander in chief, furthermore, knows who unpopular elevated gasoline costs and he faces declining approval odds and worsening GOP probabilities in the midterm elections. While there’s still a possibility of an extended battle in the Middle East, the backdrop increasingly points to the war ending sooner than later, and markets would rally strongly as a result. Indeed, participants may want to consider setting up TACO trades, with longs on Russell small caps and Treasury duration alongside shorts on energy stocks poised to benefit disproportionately from a possible truce.

China’s National Bureau of Statistics (NBS) reported that industrial production, retail spending and fixed investment strengthened during the first two months of the year while unemployment was generally stable. Home sale prices, however, continued to fall. The unemployment rate in the world’s second largest economy climbed from 5.1% in December to 5.3% during the January and February period, which exceeded the consensus estimate of 5.1%. An NBS spokesperson, however, maintained that the increase resulted from the Spring Festival holiday and that the rate was unchanged y/y. Also in February, new home prices sank 3.3% y/y, the fastest pace in eight months. Prices dropped 3.1% in January. On a m/m basis, the metric depicted a 0.3% decline, a slight moderation for the 0.4% descent in January, which supported optimism that housing deflation may be in its final stages.

Industrial output in China climbed 6.3% in January and February relative to the same period of 2025, according to the NBS. Economists anticipated a 5.3% gain following the 5.2% increase in December. The recent activity was led by high-tech production and value-added equipment manufacturing, which grew 13.1% and 9.3%, respectively. On a more granular level, 3D printing devices, lithium batteries and robotics output climbed by 54.1%, 42.6% and 31.1% y/y. In another development, fixed investment, which consists of capital expenditures in rural areas, climbed 1.8% y/y in February, a much stronger showing than the 5% fall anticipated by economists and the negative 3.8% print for January. It was also the first positive report since August when investment climbed 1.6%

Retail sales during the January and February period grew 2.8% y/y, exceeding both the consensus estimate of 2.6% and December’s 0.9% expansion. Broadly speaking, retailing benefited from strong spending during the Spring Festival with home bookings and duty-free shopping experiencing healthy demand.

The extent of February price gains as depicted by the Consumer Price Index eased considerably in Canada on a y/y basis, but the metric was driven largely by changes in retail taxes. The m/m pace moved in the opposite direction. For the y/y print, the CPI was up only 1.8% following January’s 2.3%. In mid-February of last year, prices jumped when a tax holiday ended, which caused a higher base effect, resulting in a lower reading. The m/m metric, conversely, depicted costs growing 0.5% relative to January. Economists anticipated a 0.7% lift following the goose egg result in the first month of the year.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. Eligibility to trade in digital asset products may vary based on jurisdiction.

Short selling is an advanced trading strategy involving potentially unlimited risks and must be done in a margin account.

Trading on margin is only for experienced investors with high risk tolerance. You may lose more than your initial investment. For additional information regarding margin loan rates, see ibkr.com/interest

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

")

lol. There is ZERO chance of a deal. ZERO. and NO SHIPS are going thru. Except Chinese…so what is the street thinking? It’s garbage.

Hear hear.