- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted November 11, 2025 at 1:10 pm

Optimism regarding the government potentially reopening tomorrow following an expected vote in the House was countered by weaker-than-anticipated economic data this morning. ADP and the NFIB reported declines in payrolls and in small business sentiment, which weighed on risk appetites in markets before animal spirits made a ferocious comeback. Furthermore, valuation concerns and news that SoftBank sold all of its Nvidia holdings are hampering the performance of tech shares. But the soft employment and survey numbers are dialing up probabilities of a Fed cut in December, as the central bank responds to rising evidence of deteriorating labor conditions. That dovish descent on the yield curve has investors picking up stocks in the rate-sensitive, cyclical areas of the equity space, with 10 of the 11 major sectors advancing. The imminent end of the shutdown coinciding with the potential for incrementally accommodative monetary policy is driving a bifurcation across the benchmarks, with the Dow Jones Industrial climbing strongly, the Russell 2000 near its flatline, while dwindling Mag 7 enthusiasm is weighing on the S&P 500 and Nasdaq 100 gauges. Treasury trading is closed for Veterans Day; however, futures are indicating lighter costs of capital throughout maturities in response to slowdown fears. Softening growth prospects are slamming the greenback and most commodities minus natural gas and crude oil, as Washington’s sanctions on Moscow are lightening the supply picture. A relaxation of speculative momentum is sending bitcoin south, although volatility protection instruments and forecast contracts are caching bids.

Private Payrolls Contract

The US private sector lost an average of 11k jobs per week during the four-week period ended on Oct. 25, according to ADP. The weak performance quells the enthusiasm from the provider’s upbeat monthly employment report released last Wednesday and adds credence to the belief that payroll losses have been mounting, as depicted by Challenger and Revelio last Thursday.

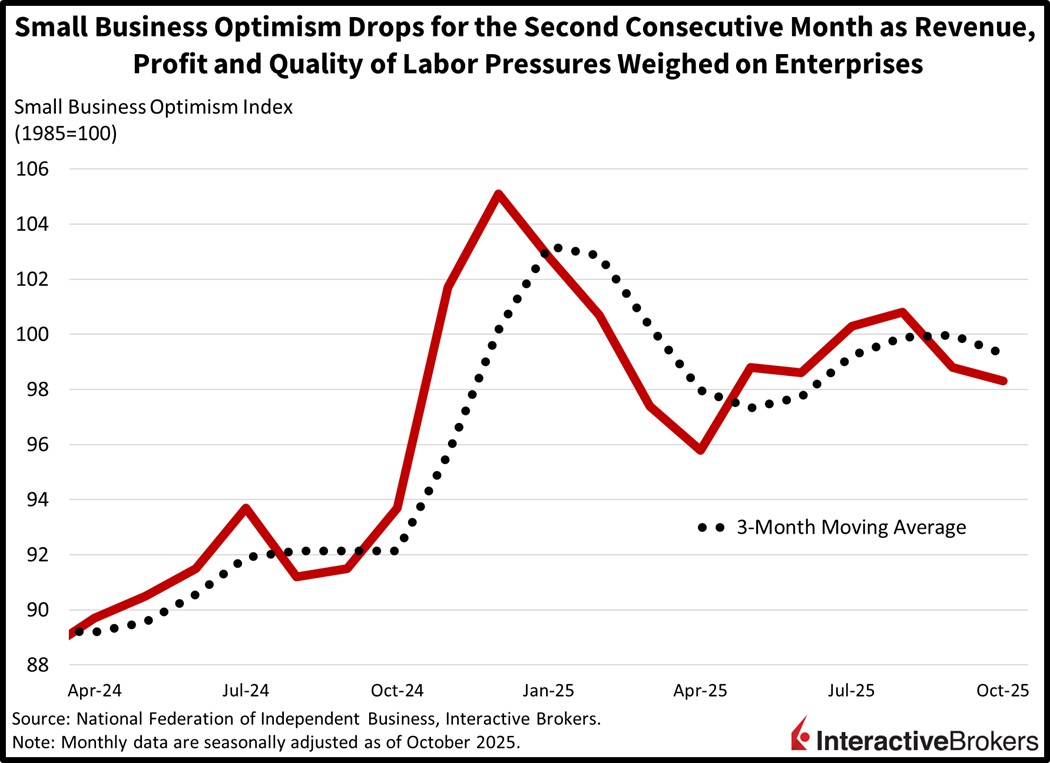

Small Businesses Under Pressure

Small business optimism weakened further last month, according to the National Federation for Independent Business (NFIB), as enterprises noted softening profitability conditions. The headline figure of 98.2 missed the projected 98.3 and dropped from September’s 98.8. Pressures on earnings, revenues, inventories and hiring drove weakening economic expectations; however, firms were upbeat about expansion projects as well as the cost and availability of credit. As far as the single most important problem plaguing establishments in the survey, 27% reported quality of labor, 16% said taxes, 12% mentioned inflation and 10% announced a lack of transactions.

Data Poised to Strengthen Following Reopening

Weak labor data is poised to strengthen following elevated confidence of a reopened government tomorrow. The resumption of federal activities is set to bolster sentiment in the economy by propelling liquidity conditions for workers, contractors ad vendors while stabilizing public services. Meanwhile, the incoming releases of long-awaited economic figures are likely to propel odds of Fed rate cuts in upcoming meetings, as the BLS’s jobs report is probably going to be released next week. I’m expecting soft results to come in, a result of the shutdown slowing the cycle’s momentum, followed by a subsequent reacceleration as we head into 2026. Finally, a favorable seasonal environment alongside enthusiasm concerning monetary policy are set to drive a year-end rally, as investors overlook short-term slowdown concerns and focus on long-haul corporate earnings growth ahead.

International Roundup

UK Labor Market Weakens and Fiscal Deficit Comes into Focus

The United Kingdom’s job market weakened at a time when anticipation grows that Chancellor Rachel Reeves will seek tax hikes to fill an expected budget shortfall. Last month, 29k individuals filed for unemployment benefits, according to the Office for National Statistics. The result was considerably worse than the economist consensus estimate of 17.6k and 400in September.

Preliminary data, furthermore, depicts the number of working individuals slipping 180,000 year over year (y/y) and 32,000 month over month (m/m) in October. The change resulted primarily from fewer full-time payrolled individuals. The unemployment rate, meanwhile, climbed from 4.8% to 5% during the July to September period, surpassing the consensus estimate of 4.9%.

Wage increases also eased. Annual compensation with bonuses was 4.8% higher in September compared to the 5% gain in August. Economists anticipated that pay raises would match the preceding month’s result. The similar metric without bonuses climbed 4.6%, slowing from 4.7% in the preceding month but matching the economist consensus estimate.

Britain Chancellor Rachel Reeves recently opined that sticking with the Labor Party’s pledge to refrain from raising taxes would require deep cuts in capital spending as the country predicts it will experience a funding shortage in the coming budget. She is scheduled to present the next budget on Nov. 26 and her recent comments have observers anticipating that she will propose a tax increase. The Institute for Fiscal Studies recently estimated that the coming year’s budget could face a £22 billion financial gap.

And Retail Sales Growth Cools

UK retail sales in October grew at their slowest pace since May as consumers waited for Black Friday deals against the backdrop of the country’s looming budget shortfall potentially sparking a tax increase. Total sales were up 1.6% y/y, while comparable sales climbed 1.5%, down from 2% in September, according to the British Retail Consortium. The headline number was significantly below the 12-month average of 2.1%. Food sales were up 3.5% y/y, matching the 12-month average. Higher prices accounted for much of the increase. Non-food sales, however, were only 0.1% above the year-ago level. The 12-month average for this category is 0.6%.

Australia Consumer Confidence Finally Turns Positive

The Westpac-Melbourne Institute Consumer Confidence Index jumped 12.8%, hitting 122.8 this month. It was a seven year high in addition to exceeding the pessimism-optimism threshold of 100. Prospects for the economy contributed the most to the increase with the 12-month and five-year expectations strengthening 16.6% and 15.3%. A de-escalation of the US-China trade dispute and a deal involving Australia providing rare earth materials to the world’s economy contributed to the improved outlook. Additionally, consumer demand and the housing market have both improved. On the downside, individuals have renewed concerns about potential inflation and the interest rate outlook.

And Business Conditions Improve

Australian business conditions firmed in October with the National Australia Bank index climbing one point to +9, the strongest result since March 2024. Conversely, the organization’s index of business confidence slipped one point to +6, but the level is still above the long-term average. Within the business conditions gauge, sales hit +19, up five points and profitability reached +9, a three-point advance. Employment was unchanged at +3. Overall activity also remained high with capital utilization moving from 83.3 to 83.4.

Investors’ Outlook for Eurozone Weakens

Eurozone investors’ confidence sank this month, with the Sentix gauge falling from -5.4 in October to -7.4. Economists forecasted a slight improvement to -3.9.

Sentix, a behavioral finance firm, says the decline resulted from a lack of indicators that the eurozone economy is ready to improve. The current situation metric fell from -16 to -17.5 and the expectations measurement moved from 5.8 to 3.3. On a positive note, inflation fears eased, however, with the outlook for price pressures moving to -11 after the preceding month’s print of -20.

Banking Lending in Japan Exceeds Expectations

Bank lending in October was 4.1% higher than in the year-ago period. Economists expected a 3.8% gain following the 3.8% y/y increase in September. Banks also captured more money to fuel their loan activities with deposits climbing 0.8% y/y.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!