- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted May 8, 2026 at 2:51 am

Investopedia is partnering with All Star Charts on this newsletter. The contents of this newsletter are for informational and educational purposes only.

Headlines say inflation is cooling. The bond market is saying the opposite.

Two specific bond ETFs are now telling investors something the headlines have not yet caught up to.

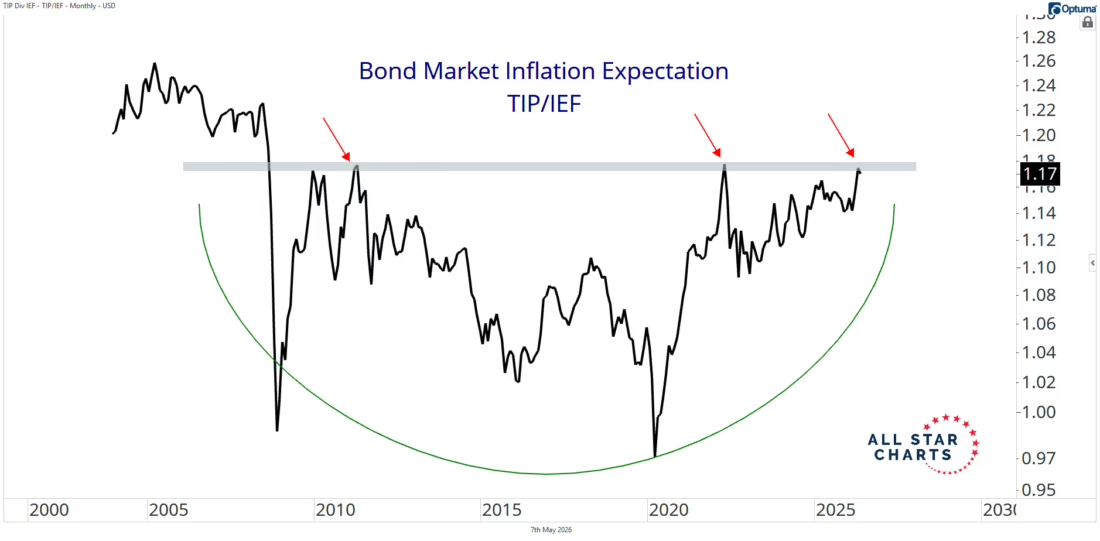

The ratio between the iShares TIPS Bond ETF (TIP) and the iShares 7-10 Year Treasury Bond ETF (IEF) just pressed against a level it has tested twice in the last fifteen years, and both prior tests failed.

The third test is happening right now, and something we’re tracking at the Strazza Letter– a confirmed breakout would tell investors that the next inflation cycle has begun.

The math behind the ratio is simple. TIP holds bonds that pay investors more when inflation rises. IEF holds bonds that pay the same fixed amount regardless of what inflation does.

When the ratio between them rises, it means investors are paying more for the bond that protects them from inflation, because they expect inflation to get worse.

Right now, that ratio is rising fast.

The current TIP/IEF ratio sits near 1.17, the same level that capped the rally in 2010 and again in 2021.

Both prior tests were rejected and the ratio rolled over. What is different this time is the chart structure, with the ratio having spent the last several years building a slow base and climbing higher off each pullback, the kind of pattern that usually precedes a breakout rather than another rejection.

The reason this matters is that bond traders tend to read inflation before equity investors do.

The bond market is the largest and most liquid market in the world, and it is dominated by institutions with access to credit data, supply chain information, and central bank intelligence that retail investors never see.

When the bond market starts pricing in higher inflation, it is usually correct.

For an everyday investor, a confirmed inflation re-acceleration would change a lot of things at once.

Standard bonds in retirement accounts would lose value, because the fixed payments those bonds promise become worth less when inflation rises.

Cash sitting in checking and savings would lose purchasing power faster than it already is, and the cost of groceries, gas, rent, and insurance would continue rising at a pace most people have not budgeted for.

Inside the stock market, the effects would split across sectors.

Energy companies, materials companies, miners, and other producers of real assets would benefit directly because the things they sell would command higher prices.

Long-duration growth stocks, including many of the technology names that have led the market, would face pressure because higher inflation usually means higher interest rates, and higher rates make distant future earnings worth less today.

The investments that would benefit most directly are the ones that have lagged for years.

Gold has already rallied above $4,700 per ounce, with major banks now forecasting prices over $5,000 by year-end, and Brent crude is forecast to average $86 per barrel in 2026 versus $69 last year.

The World Bank projects overall commodity prices to rise 16% in 2026, and the bond market signal would confirm what those individual moves are already telling investors.

The macro context supports the setup.

The 5-year breakeven inflation rate sits at 2.67%, well above the Federal Reserve’s 2% target, and CPI rose 3.3% in the twelve months ending March 2026.

Energy infrastructure damage from the Iran conflict has triggered the largest oil supply shock on record, and even with peace talks progressing, the structural pressure on prices remains.

What would invalidate this view is straightforward.

If TIP/IEF rejects from the 1.17 level for a third time and the ratio rolls back over, the breakout is not happening and inflation expectations are not accelerating.

The setup requires a clean monthly close above resistance to confirm the move.

For investors watching this signal, the level to monitor is 1.17.

A confirmed breakout would mean reviewing how much of a portfolio sits in long-duration bonds, how much sits in cash that is losing real value, and how much is positioned in the sectors that benefit from rising inflation.

The bond market does not always get inflation right, but when it has been wrong, it has usually been wrong on the side of being too cautious.

For more analysis like this, including the specific names I am tracking across commodities, energy, and precious metals if this breakout confirms, you can read The Strazza Letter.

—

Originally posted 7th May 2026

Investopedia.com: The comments, opinions and analyses expressed herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. While we believe the information provided herein is reliable, we do not warrant its accuracy or completeness. The views and strategies described on our content may not be suitable for all investors. Because market and economic conditions are subject to rapid change, all comments, opinions and analyses contained within our content are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy. This information is intended for US residents only.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Investopedia and is being posted with its permission. The views expressed in this material are solely those of the author and/or Investopedia and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Any discussion or mention of an ETF is not to be construed as recommendation, promotion or solicitation. All investors should review and consider associated investment risks, charges and expenses of the investment company or fund prior to investing. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Municipal Bonds are only available from Interactive Brokers for IBKR LLC, IBKR Canada, IBKR Hong Kong, IBKR Australia and IBKR Singapore entities.

Related Articles

?")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!