- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted April 14, 2026 at 11:44 am

There seems to be a growing crowd who say, ‘Crypto is not going away.’ Given that, keeping pace with the ever-evolving, digital financial ecosystem appears key to grasping the seismic structural shift many think the traditional financial system is undergoing. In this episode of IBKR Podcasts, we discuss a series of current trends with crypto leaders Eliézer Ndinga and Adrian Fritz of 21Shares –from trading Bitcoin in volatile times, to its role as ‘digital gold’ amid a projected spike in tokenized real-world assets – to blockchain infrastructure, prediction markets, and much more!

The following is a summary of a live audio recording and may contain errors in spelling or grammar. Although IBKR has edited for clarity no material changes have been made.

Hello, and welcome to IBKR Podcasts. I’m Steven Levine, Senior Market Analyst at Interactive Brokers – your host for today’s program. We have a lot to talk about on this show -especially in light of the recent geopolitical events and volatility. We’ll be looking at Bitcoin‘s role in all of this, along with topics centered around blockchain infrastructure, prediction markets, tokenization, and a lot more.

And here with us to fill us in with all their insights into this are Eliézer (‘Eli’) Ndinga, Global Head of Research, and Adrian Fritz, Chief Investment Strategist – both of 21Shares, which has launched several crypto exchange-traded products on various European exchanges, in various currencies,including U.S. dollars, euros, Swiss francs, and many more.

So, welcome Eli and Adrian. Good to have you here! Thanks very much for taking the time to do this.

Thanks for having us, Steven. Good to be here.

It’s great to be here.

I’m very excited about this discussion. I mean, there’s so much happening in this crypto space. It’s overwhelming to me what’s happening – not just looking at the macro environment in terms of geopolitical risk, but I guess we can start by talking about Bitcoin’s role in today’s markets. We’ll just get going with Bitcoin.

What’s happening with geopolitics today and these risks that are in the environment have just been ramping up really significantly in recent days. It keeps escalating, it seems. I mean, we’ve already hadUkraine-Russia in Eastern Europe, and now we’ve got this entire calamity across the Middle East, and there’s all these ongoing trade disputes. I mean, these might just remain with us for some time…all these uncertainties.

I’d love to know your thoughts on how you think, say, institutional investors in this environment…how should they think about Bitcoin? It wouldn’t be entirely be the same as hedging with a traditional safe-haven asset, right? It’s not like actual gold, like physical gold, or, say, the Swiss franc, but it’s speculative in nature, isn’t it – for the most part –Bitcoin? Would investors just simply find value in diversifying with it, or would it then be like some kind of speculative diversifier? I’d love to know your thoughts on this.

Absolutely. It’s a huge debate, obviously, and it always comes back to: ‘Is Bitcoin truly that classical safe haven asset?’ And I think it’s misinterpreted a lot of times. Of course, Bitcoin is a non-sovereign, scarce, globally transferable, monetary asset. But the behavior a lot of times…it just depends on the type of shock. I think in portfolio construction terms, the case—if we compare it to gold—is also less that Bitcoin replaces gold, and it’s more like Bitcoin may just expand the opportunities, because obviously it introduces exposure to a different set of macro and monetary risk factors.

We’ve seen a couple of times in the past, especially over the short-term, that it’s very sensitive to liquidity. It also trades 24/7. Therefore, if there’s any geopolitical escalation, especially on the weekend, that’s where the market expresses their feelings. But over the longer horizon, its appeal is tied to scarcity, to neutrality, to censorship resistance….

But, I think for institutions, the relevant question is not whether Bitcoin is a perfect hedge, but whether a small allocation can improve risk-adjusted returns across different market regimes.

I think for the investors listening to this podcast, what they should understand…if wetake a step back a little bit…is that Bitcoin is an emerging store of value. When we compare it with gold, this is an asset that is just 15 years old. It has been traded since 2011, but at the same time, it’s also a technology play.

So, it’s a two-phased asset that looks like an equity play because of the technological benefits, while at the same time having characteristics of gold as a scarce asset, with the benefits of also being globally accessible with an internet connection and, most importantly, also being easy to transfer and hold across borders, if people have to flee countries because of war.

We’ve seen that, of course, in multiple cases—whether it was Ukraine or Lebanon, or even as recently as in places like Iran, as well as Dubai, for wealth transfers. But I think it’s really important for investors to understand that this is an asset that can react differently, as Adrian mentioned, in different market shocks.

Historically, what we’ve seen is that as the best-performing asset of the last decade – doesn’t mean this will be the case for the next one – but, what we’ve seen so far is that Bitcoin has outperformed gold and equities in the U.S, specifically after about a month or so, despite any overshoot we experienced before.

Of course, Steven, you could tell us that in 2020 and 2021, everything went up, which is true – that’s why we carve out 2020 and 2021 to ensure investors understand that the long-story-short is that Bitcoin has outperformed, because it’s a long-duration asset rather than a short-term trade.

Source: IBKR Trader Workstation

Okay. Bitcoin, itself, has always been somewhat interesting to me, because I never really quite understood what Bitcoin was. I know it’s exercised a great deal of volatility since its inception. You had all sorts of different events—there were these liquidity shocks back in, say, 2022,there was a shock when they [the Federal Reserve Bank’s Federal Open Market Committee] raised rates to combat inflation. I think it fell something like 65%.

Source: IBKR Trader Workstation

There was also COVID, but everything kind of fell during COVID. Then you had this rally when things weren’t going so well in 2023 with the banking crisis of SVB and Signature Bank.

Source: IBKR Trader Workstation

I don’t understand exactly how the performance of Bitcoin works. I understand it’s called “digital gold,” and I understand that, you mentioned, it has characteristics of gold, but if it displays this kind of extreme volatility, as it does, can you really say it has characteristics of gold?

I guess a big question is: What exactly props up Bitcoin as an asset? I know you said it’s a technology play, and it has characteristics of gold, but what if people just lost faith in, say, the entire network that Bitcoin’s on? Would they all leave en masse? Can you just fork Bitcoin’s code and create a “digital platinum” or a “digital silver” or something like that?

It’s not fundamentally the same as physical gold, so I’m just wondering how you can justify tying the characteristics of gold to the nature of Bitcoin’s performance and volatility?

Yeah, it’s a great question. Let me respond to that, and then, Adrian, you can add to this. This is a question, by the way, that Adrian and I—we at 21Shares, running this $8 billion asset manager—get all the time. And even for me, personally, over the last 11 years in this space.

Bitcoin, more specifically, has characteristics of gold when you look at the features that the monetary asset has. This asset has about 21 million Bitcoins that will ever exist in the world. We are about 7 billion people on Earth, and there are only 21 million bitcoins that will ever exist.

You can also see that every four years there is a programmatic mechanism that decreases the inflation rate of Bitcoin by half, which means that there will be less Bitcoins created every single day up untilthe next 100 years. Today, there are about 20 million Bitcoins in existence. You might think that in the next year or so we’ll reach 21 million, but actually not.

The fact is, for the next 100 years, with this monetary policy, Bitcoin’s going to reach 21 million. That’s actually the reason why 21Shares is called ‘21Shares’—because it’s a reference to the 21 million Bitcoins.

But the long-story-short, specifically in response to your question: Bitcoin is a scarce asset, because of its limited supply, which is very similar to gold. But this supply is verifiable 24/7 in a very transparent way, thanks to the blockchain technology, itself, that underpins Bitcoin.

So, we have a monetary policy that is basically very similar to gold, with a 21 million limit, and thenalso the transparency—for you, Steven, and your audience—to check on any website where thetransactions are going and how many coins can exist today.

The beauty of Bitcoin is that this is not an asset you can forge. If you, Steven, hold Bitcoin, I cannot replicate that same Bitcoin for myself, then create the same one for Adrian and another friend, and another friend, et cetera. What you own is verifiable. It’s math-based, that no one can actually replicate it and try to steal it from you—unless, of course, you’re sharing your PIN code, which is the equivalent of your secret to hold your own Bitcoin in a safe, if you want to have an analogy.

So, it’s very important to understand that the performance of Bitcoin, is to some extent, in the short-run, acting like a tech play, but in the long-run, it’s actually acting like gold. We’ve seen that several times. And of course, gold has been used for thousands of years – Bitcoin just about 15 years or so -when looking at trading activity.

But we do believe that with the characteristics of the hard-asset and limited supply, Bitcoin is verysimilar to gold rather than similar to the [U.S.] dollar, or similar to an Apple stock, or an NVIDIA stock.

I get it. The store-of-value and the scarcity part of it make a lot of sense to me. I guess, to my mind, the only thing you really can’t do is melt it down or make it into jewelry. So, there are some downsides there, unfortunately—but I think maybe one day, who knows?

Sure, there is some downside. But the other thing you also asked, Steven, is, I think,a very important question is the value of Bitcoin. Many investors—and Adrian is smiling right now for those who won’t be watching this episode—but many investors are asking: how do we value Bitcoin? Is there intrinsic value for Bitcoin?

Adrian, you can respond to that. How do we think about intrinsic valuation for Bitcoin, especially when we look at the mining cost of production, which is very similar to gold? Adrian, can you walk us through how we think about that at 21Shares?

Yeah, there are a lot of valuation frameworks that you could apply to give you some sense, but it’s obviously quite challenging—just like it is with gold—because it doesn’t generate any yield.

However, if we take a close look at the valuation of gold, where does it come from? And, I thinkSteven you already alluded to it—it’s maybe two pieces. Number one, it is being used as an industrial metal; it has a physical use case – but that doesn’t make up a $30–35 trillion market cap. A big chunk of that valuation comes from the belief that it really acts as that store of value, which it has proven over many hundreds of years.

For Bitcoin, it’s very similar. Bitcoin has a monetary premium, because it is scarce, and that scarcity gives it value, and also the belief that it can act as a store of value in the future.

However, the other piece for Bitcoin—and that’s where the tech play comes in—it is a global monetary system, which is completely decentralized. It’s neutral, and it allows us to send value across the globe with no central control. And especially in a time with a lot of geopolitical changes – with a lot of debasement that is going to infinity, that is definitely a value proposition that is becoming more and more relevant.

I find this incredibly fascinating, especially since there are events that are, I believe,are intentionally made by governments and others not to disrupt markets. So, they’ll do them outside of market times—on weekends—so that they don’t interfere with the normal activity of daily markets.Sometimes that’s impossible to do, I suppose. But I think when you have that kind of choice or control, you would prefer to do that.

Even earnings – before the open, after the close. But now as blockchain is a 24/7 infrastructure, there is no ‘before the open or after the closed’. It’s all just operating 24/7, isn’t it?

So yes, I understand, things can happen on the weekends and you might not know, say, the price of a certain commodity, or other real-world- or off-chain asset, especially during these geopolitical conflicts. I mean, events can escalate, de-escalate, on weekends, or other times when the markets otherwise closed.

Source: Los Angeles Times Source: IBKR Trader Workstation

What would you say are some examples of how this looks, maybe just a different topic altogether…. but you did mention earlier, Adrian, the 24/7 nature of blockchains. And, so, I’m just picking up on that, and I’m thinking about tokenized assets, for example. How would you say tokenized assets or, say, tokenized commodities … What are the benefits of having them be 24/7 when these things are happening? Say, on the weekends and the market’s closed? I mean, is there some kind of like price discovery, as a benefit, to this or….? I don’t know. I don’t even know if there’s really significanttrading volume happening, with tokenized [RWAs].

What get into the volumes of those [tokenized RWAs] a bit later. But I know that commodities are a part of what is growing. And, so, I’d love to know what the benefits are of being able to trade tokenized assets, tokenized commodities, on a weekend when, say, geopolitical events are escalating.

Yeah, there’s a lot to unpack in this question, Steven. And, as you mentioned, traditional finance still operates with opening hours, with batch settlement, and with market closure gaps. And obviously blockchain allows to trade 24/7 and during weekends or during political events. I believe Bitcoin and crypto markets often provide some sort of early price signal before traditional venues actually reopen.

And I think it matters. Even if the volumes are smaller, I think the informational function can still be meaningful. And we see there’s more and more. There’s some other examples where we see on-chain derivatives, or futures, that are being traded via the blockchain that are even being referenced as kind of like gauging the price during the weekend in traditional media as well.

So, we are already seeing like a slow shift where traditional financial players looking at crypto markets just to see and get that informational inside in what could be happening until Monday opening.

I have a lot of questions about tokenization, and we’re going to get into that in just a minute, because I’ve been seeing all sorts of projections about tokenized assets just growing exponentially, it sems, through the next, I don’t know, five years or so. But I’d like to talk about that. It seems like there are very select asset classes that are dominating that volume right now.

But, if we’re talking about geopolitics, and we’re talking about what’s been really, really prevalent in markets, especially in these kinds of volatile times, I think we have to talk about prediction markets. That’s a huge topic today, it seems.

I don’t know if people recognize that prediction markets are … you know … the newer markets, anyway, are actually blockchain-powered. I didn’t know that before this. And so, I think it’s a really interesting thing. I mean, Polymarket’s processed what, like billions, I think, right? I mean, just around the last presidential election cycle that we had in 2024. They continue to be really activearound geopolitical events, right? I mean, they’re providing even more accurate, maybe, some think real-time probability assessments than what we refer to today as traditional polling.

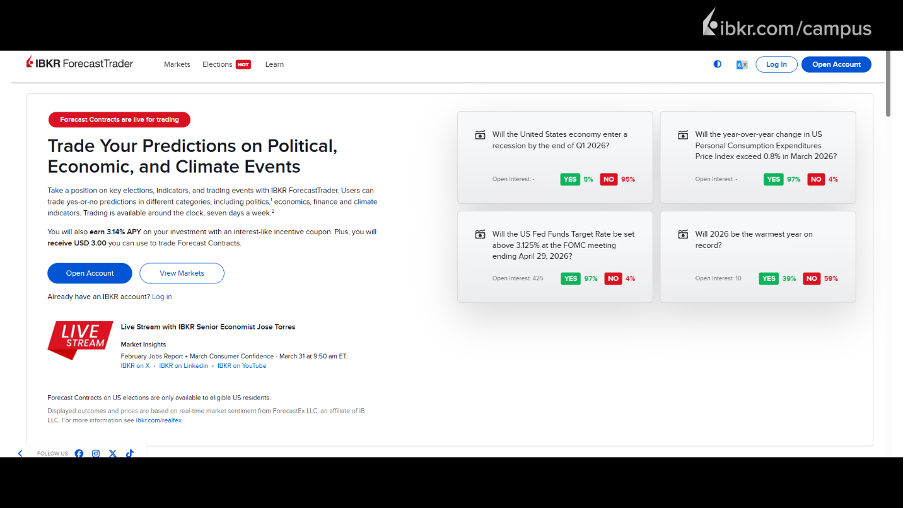

Everything’s ‘traditional’ now, you know, compared to ‘digital’. At IBKR, we have ForecastTrader – that’s a CFTC regulated prediction market platform. But in the digital asset world … in the blockchain-based permissionless markets…. I’ve seen this term a lot. I want to ask what that is. Does that just mean it’s not regulated by any government authority – that it’s called a ‘permissionless market’?

This is a phenomenal question, and there are two layers If you want to understand the technology of prediction markets and what they offer for users like you and I and institutions.

So, the first one is that prediction markets are technology based. And they’re not built by proprietary databases by a single entity, they’re built on public networks, like, for example, Ethereum …or any of the networks that looks at this. So, for investors, essentially Ethereum is a platform that allows entrepreneurs to build applications like we know today, whether it’s Zoom, Slack, WhatsApp, PayPal on your phone can use it and leverage it for different use cases.

But instead of having Apple or Samsung controlling it, you’re able to build it in a decentralized way and not have a 20% tax on the product that you’re building. So, that’s one.

So, prediction markets are physically built on public networks, and the technology is to some extent decentralized. However, when it comes to the distribution, the distribution has to be regulated by local authorities.

And that’s why you’ve seen prediction marketplaces like, for example, Polymarket that people know really well, and another called Kalshi.

So, to respond to your question specifically, when we talk about traditional prediction markets andpermissionless markets, it’s not about the fact that one of them is regulated and the other is not,because both of them are actually complying with local jurisdictions when it comes to distribution in local jurisdictions.

And that’s incredibly important. So, this is a fascinating technology to me, that, of course, has been around for a while – people have been using pollings and betting on sports, et cetera., but not in a decentralized way, where people have an internet connection to be able to even help people to better understand the world order that we know today that is changing back and forth with geopolitical conflicts.

But the good thing is, people like our mothers and even grandmothers, are able to use and actually follow the news without realizing on their phone that this is a blockchain-powered application. And that’s the whole point of it. That’s why you, Steven, you’re incredibly impressed that…and you didn’t know that actually Polymarket was built on a blockchain. And you don’t even need to know. You don’t even need to know that we’re using TCP IP to make this conversation – and that Adrian and I are in Europe and you’re in the U.S. to have a conversation. What matters is how this podcast really helps your audience to get from 0 to 1, and 1 to 10, in the crypto space, and this is what we’re here for.

I guess the question here is: can you really replicate what’s happening, say, with blockchain-based prediction markets with, say, traditional infrastructure? I mean, we have ForecastTrader here at IBKR, so there are these differences between a regulated, traditional approach like ForecastEx [Forecast] contracts on IBKR ForecastTrader, versus, say, blockchain-based permissionless markets, as we’ve been talking. But, I would think that with the regulated markets, you have, maybe, some greater legal certainty, Maybe there’s more legal protection for participants? it sounds like there’s room for maybe both of these models to coexist, but, you know, I’d love to hear your thoughts on whether there’s really is more of a benefit for, say, the blockchain-powered solution, or whether there’s more of a benefit to regulated approaches. And what are the risks?

Yeah, I think you already said it. I think it might be a combination of both. I do think some of those traditional infrastructures – they can replicate some of the economic functions, but usually it comes with a more centralized onboarding, maybe with more compliance constraints, maybe product approval processes.

So, those traditional platforms, obviously they’re optimized for legal certainty first, while thoseblockchain platforms are optimized for openness and for speed. So, one is compliance first. The other one is more innovation first. But I think in the long-term it’s neither-nor. I think it’s a convergence of both models. I think it will just merge together and get the best of both worlds.

Yeah, I’d like to think that there’s not going to be such a loss of dimension, becausewe’re losing the third dimension in a sense – of traditional finance. But that there will be these layers of dimensions within the digital world. And I think that there already are, you know, if I really look at it in terms of all the different mechanisms and operations happening within the ecosystem. It has a sort of three dimensionality to it.

And given that, I know we were going to talk about tokenized, real-world assets and the volumeprojections, I think we should actually start to really talk about that. And I know there’s been some activity…I know in your outlook, in your State of Crypto for 2026, there was mentioning of NRSROS, that’s the Nationally Recognized Statistical Ratings Organizations, like Moody’s and S&P and Fitch, on how they might well be assigning investment-grade ratings to digital vaults. I mean, I’d love to talk about that, too. And maybe that’s a part of this discussion about projections, in general.

If we’re going to, say, bring all real-world assets that are off-chain, on-chain, we’re looking at something like $400 trillion worth of assets. And it seems like some of these are already well under way in being tokenized. You’ve got maybe $200 billion to $300 billion, I think, right now if I’m not wrong about that. There’s a small amount in comparison to what the opportunity is to tokenize, but I see mainly private credit. I see U.S. Treasuries. I know there are some funds out there like BlackRock’s BUIDL and Franklin Templeton. They tokenized money market funds. [There are also tokenized] commodities, and, to a lesser extent, stocks.

Source: RWA.xyz

But the sheer volumes of tokenized real-world assets, in general, it seems, are set to spike, I’m reading that could reach, anywhere between $4 trillion to $16 trillion by 2030. Is that right? What are what are 21Shares’ projections on this? And what’s behind these massive growth estimates? We’re talking about, what, like 5 to 10 times growth from the current $200 billion to $300 billion – to $1 trillion to $2 trillion by the end of this year? Am I right in saying all of this?

No. You’re right. Absolutely. I do think that it’s good to step back for your audience,and to echo what Adrian said when it comes to the blockchain benefits; it’s mainly operational, it’s on the back-end, invisible to you. It’s helping institutions to actually issue assets at the cheaper cost, and at a faster rate for transactions for goods.

So, for example, concretely, if I want to send you one dollar, it would cost a few cents. But most importantly, it would basically be sent like a WhatsApp message or other iMessage, you know, using WhatsApp. And mostly in America people use WhatsApp. So, I would send an iMessage, and within a few seconds, actually milliseconds, you’re able to receive it, and you don’t have to wait for, you know, market opens, or market closes to be able to make that transaction.

So it’s really about operational efficiency. And what we’ve seen is that the best product market fit beyond Bitcoin as a long duration and emerging store of value … we’ve seen that medium of exchange of dollars across the world. So, sending out dollars for payments, and transfers, and trading has been the best performing use case I’ve seen in the cryptocurrency space – and that’s the concept called ‘stablecoins’. Basically. 100% backed dollars in the bank account, where if you have a crypto wallet across the world, you’re able to send a dollar, essentially like an iMessage, which is really something that we’ve never really seen before with the decentralized infrastructure.

So, that’s why for us, beyond dollars, beyond fiat currencies, we’ve seen the emergence of government bonds and also Treasuries, as well as private equity completely built on these decentralized blockchain, but distributed in regulated venues, where basically, you know, regulated securities have to be distributed.

That’s why most of the distributors of these tokenized assets really have to comply with the SEC or the CFTC, depending on the treatment of the underlying asset. So, really, this is the beauty of the operational efficiency that we’ve seen, and we’ve seen an unprecedented growth from institutions and banks and even central banks and little-known regulators to take the tokenization really seriously.

That’s why you’ve seen regulatory clarity in the U.S. – first with stablecoins, because that’s the first use case that people mostly used with the GENIUS Act. And then the CLARITY Act – that is pending – to make sure that investors can treat tokens, whether they’re equities or commodities or currencies, in a way that would be under the purview of either the SEC for equities or the CFTC for commodities.

So, that distinction has been pending. And that’s why we are heading towards regulatory unification. And that unification and harmony is going to really help spur innovation, as we’ve seen with the Internet. In the early 2000s, Steven, the three of us – Adrian and yourself and myself – we were actually worried to use credit cards to make payments for flight ticket. Today, it’s second nature. Even not using our PIN code to make payments at the grocery store and just using, you know, the ‘tap’ is something that felt really worrying 17 years ago.

So, I do think that CLARITY is going to help protect consumers and spur innovation to a level that we haven’t seen before, especially for now, under this current [U.S. President Trump] Administration. And that’s why we believe that tokenized assets can really reach a higher level than we actually haveexperienced so far.

And to give you a number, stablecoins – on fiat currencies on the blockchain – so, in dollars represent U.S. $300 billion in total assets, which is really an impressive amount, and we’re expecting to reach $1 trillion dollars.

Steven, when it comes to tokenization on my end, I have a strong opinion—and it’sthat tokenization is actually very boring. It’s very, very boring.

Really?

And the future of crypto and blockchain is quite boring, in my opinion, because what does it really mean? I mean, everything that is being built here is financial infrastructure. So, eventually it will all blend into the background and we all will be using it on a daily basis, but we won’t be noticing it. So that is pretty boring, actually. But it’s also very disruptive and necessary.

And we’ve seen a lot of efforts around the globe with Nasdaq and Kraken, one wanting to tokenize, assets and equities – The New York Stock Exchange – and ‘tokenization’ is just a fancy term.

You might remember the days when we got digital cameras.

Yes.

And it was a big deal. We called it ‘digital’ cameras. No one says ‘digital’ cameras anymore. Now, we call them analog ‘cameras’, because every camera’s digital. It’s the same with tokenization. I mean, in the long future, when we trade assets, all of them will be tokenized, but we will just drop the word ‘tokenized’. And I think that’s really how the future’s going to look like.

Yeah, it’s happening very quickly, it seems.

Adrian Fritz

Yes.

I do remember digital cameras, and I was a little upset about the introduction of the digital camera, because I was very, adamant about the film camera, about loading my film. I liked that. You know, I loved the idea that I only had 24 to 36 pictures, and now they were allowing somebody to shoot just as many as they wanted, it seems. And it was trying to do everything it could possibly do to replicate what could already be done.

And that, to me, is how I first thought about the entire digital [financial] ecosystem – that it’s trying to do something for the financial system that has already been done and works really well. But now I’m starting to see that there aren’t all sorts of benefits to this, as I look further into how the infrastructure is being built.

For example, I know Eli, you mentioned CLARITY in the U.S., and I know that there are other regulations that are going on, globally. There’s MiCA [Markets in Crypto-Assets], I guess you call it, in the EU. The UK has got their own … Singapore, I suppose, and Hong Kong. I’m sure there are others that are developing their own regulations, in a sense, to help clarify trading these tokenized assets. And, so, it seems like there is a concerted effort of a more global type of system that can maybe more easily be transacted within.

Stablecoins are allowing all sorts of transactions to take place that would otherwise be cumbersome in the traditional markets like, I guess, cross-border financing, for example. So, I get very excited about the prospects that can come from the digital [financial] ecosystem, whereas at first, I was very skeptical about it.

I do like digital cameras now, but I still use a film camera, so, I’d like to know that there’s still a place for me to go that is off-chain, if I needed to. And do you think that at some point that’s just all going to go away? Or become a part of a distant nostalgia?

That’s a very good question, actually—almost a philosophical one. And I don’t knowto be really honest. I think it will take a while. I think we’ve seen the same with ETFs being introduced – that kind of made mutual funds much more liquid, much more transparent, much more exchange-traded, as the name implies. And I think tokenization is just the next evolution of that, where you have programmability and 24/7 trading.

But I would say with all innovations, it’s almost a curse and blessing. I would say a lot of people in traditional finance would say it’s quite nice that markets are closed on a weekend, because it’s stressful. And now we’re moving to 24/7 markets, so that’s going to change a lot. It’s going to change a lot how firms and institutions operate, because they’ve got to cover markets 24/7.

I’m also curious how it’s going to look like in regards to liquidity, because usually in TradFi, liquidity is around the opening and the closing, while when it’s open 24/7, will we also see a bit of clustering?Will it consolidate during certain market hours? Or will it just kind of dilute?

So, there’s a lot of open questions, and I think it’s going to take a while until this world establishesitself. But I’m curious how it’s going to look like, and where we are going to spend our time off-chain?

It’s really important to also add the fact that we are seeing the rise of AI, and the agents, that could replicate what humans and traders could be doing in the future. Not yet, but to a large extent.

So, I do think that there will be a convergence between blockchain infrastructure that is invisible, and what AI agents really help to trade 24/7, and being able to overload the market for institutions and trading desks. And this is already happening to a large extent. But this is, I think, the same evolution as high frequency trading, but it would be on the blockchain powered by AI agents.

And because most importantly, AI agents are not going to open a bank account – traditional bank account or a brokerage account – it would be mainly humans – so, the use of functions by AI agents is going to be significant. And that’s why, I think, to Adrian’s point, how this is going to look like? We don’t know. But I think we have a good sample today to understand that there would be a convergence between, especially blockchain technology and AI in this 24/7 environment that we don’t know today, which means that most likely humans are going to touch more grass, and get the CIA briefing everyone to understand markets.

We’re going to be pushing a lot of buttons, I think.

So, let’s go back to these NRSROs like Moody’s, S&P, and Fitch. Now that we’re talking a lot about the tokenization of things – more specifically, and I don’t understand how this works, and I know you mentioned it in your in your state of crypto outlook for 2026 – we’re talking about, say, pension funds or insurance companies that need to adhere to certain ratings requirementslike investment-grade ratings for corporate bonds, I suppose.

So, if the ratings agencies assign, say, an investment-grade rating to a digital vault, how exactly does that work? And I would think that if they could, it would prompt more activity of tokenizing, say, corporate bonds to put in digital vaults – or other investment-grade-rated assets that could be tokenized.

But how does that work, exactly? I mean, is this only for credit products? Because, they’re assigning a credit rating, right? So, are they just credit products? Does that same vault house other tokenized assets like real estate alongside these high-grade credit products? Less-than-[investment-grade] credit-quality products? I don’t understand how this works. Do investors have separate vaults for separate assets? Or is it like a single vault for the investment-grade credit products only? And that’s what we’re talking about – the opportunity [for these off-chain assets] to get tokenized, because we’ll have these [investment-grade credit] ratings. And then investors like pension funds and insurance companies can take full advantage of that type of mechanism for their portfolio.

Okay, perfect. So, essentially a vault, or a computer program, that allows you to do lending and borrowing at a certain rate, space, and credit ratings, and they do that for specific assets and based on investors’ risk profiles. And this is something that is really interesting but cannot be done, to your point, without the equivalent of the Moody’s of the world that would really allow institutions to feel comfortable. That’s the first step. And then the second step is to allow institutions to come in.

What is really important to highlight is that AML and KYC is also incredibly important. Anyone can open a, crypto wallet and then trade against each other. But for the institutions, they have compliance mandates. And this is, of course, a non-negotiable. And that’s why these transparency, and KYC, layer is incredibly important for the investors to feel comfortable to allow, then, the BlackRock’s of the world to come in and be able to trade against one another.

But that’s what we’ve seen so far, actually. We’ve seen that the Apollo’s of the world, the BlackRock’s of the world, actually coming in and allowing their tokenized products – or investing directly in these lending marketplaces, whether Aave or Morpho, which are lending marketplaces in the crypto space,or even spot marketplaces that can do swap, as well, to give you names for the audience.

Of course, what we discuss today is not financial advice, but what is interesting is that we’re seeing these watershed moments of the early innings of credit ratings that really allow investors, to really feel comfortable and be able to have familiar formats when it comes to compliance with ratings, as well as ‘KYT’, which is basically the equivalent of KYC on the blockchain; it means ‘Know Your Transactions’.

I think we’ve covered quite a lot. I know you’re a bit bored by tokenization and infrastructure, Adrian, but let’s hear from both of you – what each of you are most excited about seeing in the next 1 to 2 years.

Do you see any progress with mainstream adoption? What are your thoughts on all this?

I think we clearly see some more institutional adoption. I think our job is slowly becoming slightly easier. What I mean by that – compared to kind of previous bear markets, where almost none the traditional investors even wanted to take the meeting with us, now those conversations have changed completely. Now they truly want to understand and get that educational insight to make sure they handle this new asset class correctly.

And once again, it’s going to impact them – if they want or not – either from an investment point of view – so, if they ever decide to make an allocation into this asset class or from the technological point of view, meaning in regards to stablecoins, tokenization, everything that we just mentioned, it will need some sort of change, if they want or not.

And I think they’re starting to understand that, and that’s why they truly understand what’s going on.

So, they’re coming with some interest as opposed to selling them on the idea.

Yes.

That’s great. Eli, what do you think? What do you think about Bitcoin, too, because we started with Bitcoin. Where do you think it’s going to fit now that the tokenized asset ecosystem is growing? I mean, is it still going to be like this ‘digital gold’ or…?

Yeah, we definitely do not provide financial advice. But, jokes aside, I truly believe that … it’s interesting, because I had the same question last week from a very large institutional client that we discussed with, and they were asking the questions around, ‘Well, we got tokenized gold now on multiple blockchains, what about ‘digital gold’ that we call ‘Bitcoin’?’

And I do think that, fundamentally, Bitcoin will always be complimentary to gold in a diversified portfolio. And we’ve seen that over the past eight years. And we had in the first Bitcoin allocation research that we published in 2019 at 21Shares, where we saw the benefit of Bitcoin with a declining volatility over time, despite the fact that this is more the go-to asset compared to NVIDIA or an Apple stock. But we’re seeing a declining volatility over time. With, of course, a small allocation, we’ve seen benefits in the diversified portfolio. But rebalancing is key for the indexers.

So, I do think that for the disciplined investors with a long time horizon, they are going to actually seethe benefits of Bitcoin over time. And that’s one way to look at Bitcoin – as a hard asset.

But then when it comes to the system itself, which is a tech play, there will be a premium to it,because Bitcoin is also similar to Swift. But Swift is controlled by a company, but Bitcoin is not controlled by any organization. So, in a world where we become more fragmented, we have more volatility and more geopolitical conflicts, international and censorship resistant monetary system around Bitcoin is going to be more in demand over time. And we’ve seen that in several places around the world, where there is even China that actually banned Bitcoin a few years ago. But even in places like Lebanon and Ukraine, when people fled the country to leave the war. So, we definitely see that Bitcoin – in a geopolitical, conflictual environment – is beneficial for many people around the world and not just institutional investors.

And then the second thing is – when it comes to what I’m excited about – is the early innings of the adoption of blockchain technology beyond trading. And I’ve seen that when my very own mother has been actually seeing the news, and Polymarket around the U.S. elections, and understanding what’s going on in Iran, without actually spending more time on CNN or CNBC, which, of course, I really respect these two channels.

What I’m saying is that we’re seeing a complementary, media outlet in prediction markets where people follow the news, without actually understanding that this is based on any blockchains. They just see the information being incredibly useful to them on what it means for the future. And I do think that this is where blockchain is going to be, as Adrian mentioned, a back-end, or boring technology to some extent.

But the user applications, the consumer applications, that we know today are also going to become blockchain-based. And that’s why, Steven, if I asked you in the early 90s if you would be comfortable to take a car with a stranger, you would say, ‘no’, but today, you would do it, because of increased trust built around it, because there is trusted regulation, and there is user experience that is incredibly exciting and simple for you.

And I do think that this is where we’re headed for consumer applications – blockchain-based. Andthat’s why people have to watch this space. And I think Polymarket and even Hyperliquid, which is the futures exchange, really allows that to remove the complexity that of course people are experiencing today, or even Adrian and I from the last ten years in this space.

It’s crazy how quickly things change—and how much behavior changes as a result ofthe innovations. It’s so true. Even hailing a taxi in New York City was something of a risk that people were reluctant to take. It was a common behavior, but it was always, you know, ‘Are we going to be taken for a ride? And to where? Hopefully, our destination.’ And hopefully we will go to our destination, or at least the one that we imagine is going to be this digital [financial] ecosystem at the end of the day. I think it’s developing in such fast ways.

But this was really, really terrific. Eli, Adrian, thank you so much, again, for taking the time to do this! Is there anything else that you’d like to say before we sign off?

I would always say, ‘start small and start learning’, because this is not a trade. It’s truly a structural shift that is happening. And even if you don’t believe in crypto, I think you truly need to understand what you’re opting out of. And, so, that’s my message.

As a friend of mine says, you may not agree with, or be interested, or even have any kind of real direction in terms of your investment strategy, but it’s not going away. And I just keep hearing that, and I just keep thinking it’s true. And since it’s not going away, and there’s so many developments happening in so many different spaces – regulatory and institutional and otherwise, it almost feels like an inevitability, but I guess time will tell.

But, anyway, I hope you’ll both be back with us. It’s an ever-evolving space and the depth of information that you’ve given us is amazing. And, so, thank you so much for that!

For our listeners, you can learn more about 21Shares at 21shares.com.

You can also read more commentary and market analysis, including on crypto markets, at IBKR Traders’ Insight. There’s a lot of content there. You’ll also find more information about Interactive Brokers’ crypto offerings on ibkr.com.

And for a full list of financial education resources, visit IBKR Campus, where—as always—all educational material is provided to the public at no cost.

And until next time, I’m Steven Levine with Interactive Brokers.

Thanks for joining us.

LEARN MORE

21Shares State of Crypto #16: Market Outlook 2026

Open an IBKR Account / Start a Free Trial

Getting Started with Cryptocurrency

Combating Crypto Skepticism (WisdomTree, Dec 8, 2025)

The GENIUS of Stablecoins (Abra, Dec 1, 2025)

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. For more information about the risks surrounding the trading of Digital Assets please see the "Disclosure of Risks of Trading Digital Assets".

Cryptocurrency based Exchange Traded Products (ETPs) are high risk and speculative. Cryptocurrency ETPs are not suitable for all investors. You may lose your entire investment. For more information please view the RISK DISCLOSURE REGARDING COMPLEX OR LEVERAGED EXCHANGE TRADED PRODUCTS.

TRADING IN BITCOIN FUTURES IS ESPECIALLY RISKY AND IS ONLY FOR CLIENTS WITH A HIGH RISK TOLERANCE AND THE FINANCIAL ABILITY TO SUSTAIN LOSSES. More information about the risk of trading Bitcoin products can be found on the IBKR website. If you're new to bitcoin, or futures in general, see Introduction to Bitcoin Futures.

Investments in certain commodities (precious metals) may be subject to significant price volatility and often involve risks related to market fluctuations, liquidity constraints, geopolitical events, and changes in global economic conditions that could adversely affect their value.

U.S. Spot Gold trading through IB LLC accounts is only available to legal residents of the United States that do not reside in Arizona, Montana, New Hampshire, and Rhode Island.

Interactive Brokers LLC is a CFTC-registered Futures Commission Merchant and a clearing member and affiliate of ForecastEx LLC (“ForecastEx”). ForecastEx is a CFTC-registered Designated Contract Market and Derivatives Clearing Organization. Interactive Brokers LLC provides access to ForecastEx Forecast Contracts for eligible customers. Interactive Brokers LLC does not make recommendations with respect to any products available on its platform, including those offered by ForecastEx.

Any discussion or mention of an ETF is not to be construed as recommendation, promotion or solicitation. All investors should review and consider associated investment risks, charges and expenses of the investment company or fund prior to investing. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Alternative investments can be highly illiquid, are speculative and may not be suitable for all investors. Investing in Alternative investments is only intended for experienced and sophisticated investors who have a high risk tolerance. Investors should carefully review and consider potential risks before investing. Significant risks may include but are not limited to the loss of all or a portion of an investment due to leverage; lack of liquidity; volatility of returns; restrictions on transferring of interests in a fund; lower diversification; complex tax structures; reduced regulation and higher fees.

There is a substantial risk of loss in foreign exchange trading. The settlement date of foreign exchange trades can vary due to time zone differences and bank holidays. When trading across foreign exchange markets, this may necessitate borrowing funds to settle foreign exchange trades. The interest rate on borrowed funds must be considered when computing the cost of trades across multiple markets.

Stablecoins may lose value, de peg from the U.S. dollar, face liquidity, operational, or regulatory risks, incur blockchain or conversion fees, and are not insured; you could lose some or all of your funds. Stablecoin transfers and conversions facilitated through Zero Hash for Interactive Brokers LLC (IBLLC) clients may be subject to additional network or conversion fees, and all stablecoin transactions remain the responsibility of the client.

ll exchange and custody services in connection with trading and holding cryptocurrency tokens and other digital asset tokens through IBKR trading platforms are provided by Cryptocurrency Service Providers.

IB is not party to any transactions in digital assets and does not custody digital assets on your behalf. All digital asset transactions occur on the Paxos Trust Company ("Paxos") or Zero Hash LLC ("Zero Hash") exchanges. Any positions in digital assets are custodied solely with Paxos or Zero Hash and held in an account in your name outside of IB. Digital assets held with Paxos or Zero Hash are not protected by SIPC.

Any trading symbols displayed are for illustrative purposes only and are not intended to portray recommendations.

Stablecoins and Tokenized assets are not legal tender, are not insured by the FDIC or any government agency, and may lose value; they carry risks including issuer insolvency, regulatory changes, operational failures, and potential inability to redeem for fiat currency. By transacting in stablecoins, you acknowledge and accept these risks.

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!