- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted December 1, 2025 at 1:26 pm

An in-depth conversation with Abra CEO and Founder Bill Barhydt about the recent groundswell of interest in U.S. dollar-backed stablecoins. We also explore how U.S. legislation might impact market and monetary policy , innovation, the future of banking, wealth management, and more!

The following is a summary of a live audio recording and may contain errors in spelling or grammar. Although IBKR has edited for clarity no material changes have been made.

Hello, and welcome to IBKR Podcasts.I’m Steven Levine, Senior Market Analyst at Interactive Brokers.Today, I’ll be co-hosting this podcast with my esteemed colleagues, Tim Troiano and Jawahar Ayyakannu Tangaraj – both developers here at Interactive Brokers, and both with a very keen interest in everything crypto, including today’s topic on the ongoing, growing interest in stablecoins.There’s a lot of interest in this topic.

And to get what I’m sure are going to be some really fascinating insights on this, we’re very fortunate to have here with us Abra CEO and Founder Bill Barrhydt. Welcome, Bill!

Hey, thank you. Great to be here. Looking forward to it.

Thanks so much. It’s great to have you here. Thanks for taking the time to do this!

My pleasure.

So, Bill, maybe we should start here with a bit of background about yourself, about your company, and then we’ll just dive right into what seems to be a really, rapidly evolving stablecoin market.

Sure. I’m a longtime tech entrepreneur here in Silicon Valley. I worked on pre-consumer Internet back in my NASA days. I was at Netscape in the very early days, working on early payments and encryption technology. Most of you would know HTTPS, which I was involved with the creation of, and the distribution of, into international browsers. I’ve been working on myriad payments deals for the last 25-30 years as either a founder, investor, or operational exec, and started Abra about 10 years ago. It was kind of the dream job that allowed me to kind of integrate my understanding of encryption and payments.

And I did a lot of work in cross-border money transfer even, and with my libertarian views, right? So, all of a sudden it was like, wow, this is all coming together. It was super interesting.

And we started Abra about 10 years ago, and through different stops and starts as happens with startups, we’ve really zeroed-in on a fantastic business, which is really … think of it as a wealth management business for digital assets. So, we help high net worth investors, family offices, [and] institutions get exposure to the crypto space, manage allocations, investment advice as a fiduciary. We help them borrow against digital assets now – that’s probably our fastest growing business. And, also, yield products, staking, and whatnot.

Wow. And you mentioned NASA in all of that. That’s a very storied background. It’s amazing. You gave one of the earliest TED Talks too, I understand.

Yes, I was a longtime member of TED and was honored to do the first TED Talk on Bitcoin. I think it was in 2011. I think Bitcoin was trading at something like $3. And even though it’s a tech audience, just to put it in context, most people had either never heard of it or like, ‘I’ve heard of it, but I have no idea what it is.’ And so, I was astounded that they even asked me to do it, just given the nature of … Silk Road was just getting going, And those who were in the know kind of associated Bitcoin with Silk Road at the time.

I wish I had listened to you then. I’m sure a lot of people probably wish the same. This is really terrific. So, we’re really excited to talk to you about stablecoins. I mean, this is some topic. There’s also some recent, related legislation – their implications … innovation in this space … really just a great deal going on.

But before we get too far with what’s happening with these assets, maybe you could explain for those listeners, who aren’t yet totally aware of exactly what they are – what are stablecoins exactly? Why do we have them … in terms of utility? How are they used?

And what would you say would be the main attraction to transacting with them?

What are stablecoins?

Okay. So, there’s a couple of ways to explain what a stablecoin is. In the simplest of terms that integrates the idea of crypto and digital assets with the idea of traditional fiat money -“fiat” referring to the government-issued money that we spend every day. So, traditional crypto was based upon this idea that you could have a digital asset that didn’t require any intermediary at all. Meaning, if I could store my money on my hard disk, I could literally send it to you by just knowing some long stream of numbers that you would give me, and there would be nobody in the middle of that transaction. We thought that problem was impossible to solve. Turns out this mysterious Satoshi character solved the problem. But that’s all Bitcoin did. It allowed you to move the ones and zeros between those two addresses.

Now, Ethereum came along and changed the definition of what that all did by making those assets themselves programmable. Meaning, you could attach computer code to those assets and the ones and zeros that you were moving around. Turns out that one of the killer apps for being able to attach code to those ones and zeros moving back and forth was the creation of new types of tokens. And the first kind of token that we ended up creating to take advantage of that were these so-called stablecoins.

So, stablecoins basically take the best of the decentralized world, where there’s nobody in the middle of the transaction, and in theory, depending on your feelings of government, the best of the traditional government money-issued world, where now instead of moving paper around, you can move these digital tokens around. But what gives the digital token its value? Why are we allowed to call it a stablecoin?

Okay, so when I create one of these stablecoins that’s worth a dollar, my expectation is that there is a dollar – or dollar equivalent, like a treasury bond – in a bank account somewhere, backing that stablecoin. So, you’ve taken a trustless system, and you’ve added a certain amount of trust to it, which you have to do in the physical world, right?

So, that stablecoin now can be equal to however many dollars I have in a bank account representing the value of those tokens, hence the term ‘stablecoin’. It has nothing to do with the purchasing power of the dollar, which of course is not stable; it continues to fall precipitously, but the actual dollar value of the tokens should always stay the same.

And then what you would do is you would ideally audit the bank account, or bank accounts, of that stablecoin issuer to make sure that if they have $100 billion in stablecoin tokens floating around, that they have $100 billion worth of dollars, or dollar equivalents like treasuries, in those bank accounts.

So, a $1,000 stablecoin is backed by $1,000 in cash or cash equivalents.

Correct.

And is it a really liquid market? I’m assuming that it’s becoming more and more liquid as time goes.

That’s right. Stablecoins started out solving a problem, where exchanges literally could not open bank accounts; because everybody just thought that all these crypto tech bros were just a bunch of shadowy super-coders who they shouldn’t open bank accounts for. So, someone came up with this idea, ‘Well, how do we solve the problem? Well, if we can’t open a bank account, how do we get dollars in and out of the exchange?’ So, somebody came up with this idea, ‘Well, if we just move stablecoins around as digital dollars, we don’t need bank accounts, and we’ll just give on- and off-ramps to established institutions to do that. And Tether was the first big example of a company that did that.

But now there are hundreds of billions of dollars worth of these stablecoins floating around from multiple companies, not just Tether, and they’re solving all kinds of problems beyond just this bank account problem that I mentioned.

It’s amazing. I mean, it’s really, really fascinating stuff. And we’re going to get more into the issuers and the dominant players in this market, Tether as one of them. Do you see any real risks associated with transacting with them?

What are the risks?

There’s two big risks associated. Now, before I talk about the risks, let me say I’m talking specifically about dollar-backed stablecoins or euro-backed or Swiss franc. There are other types of stablecoins: there’s algorithmic, there’s synthetic dollar. I’m not going to get into what those are. It’s too involved for this conversation. So, when I talk about the risks, I’m specifically talking about the risks for dollar-backed stablecoins.

There are really two risks you have to be aware of. The first is what I said before, which is, are the dollars or dollar-backed securities really in the account that back those tokens?

Are they audited? Meaning, can I see somewhere a public-facing audit that those dollars that issuer says are there are really there? Okay, it’s common sense.

And the second risk is technology risk. In other words, if I have created a new token or digital asset representing those dollars, can that token’s code be hacked? In other words, could I somehow issue myself $100,000 worth of some stablecoin that isn’t actually backed by dollars? And the next thing you know, I’ve got 10-times the number of stablecoins floating around than I do dollars.

Now, the good news is, is that I think we’ve, at least for the stablecoin-specific type of product, have really addressed the technology risk. Those type of tokens have been around for several years now and have proven to be very stable from a technology perspective, not hackable, and generally reliable, very reliable. The only issue with them from a technology perspective is the fees can be highly volatile, and that’s been solved by competitive technologies like Solana, and I’m not recommending anything, but you have Solana, you have Base.

There’s a lot of competitive blockchain technologies now that have addressed that fee problem. And of course, more of these issuers are providing public-facing audits, and the regulators are requiring those audits, including the new GENIUS Act legislation that was passed in the US.

The GENIUS Act, I understand, was signed into law earlier this year – I believe back in July, I understand — had great, strong bipartisan support. Then there’s the CLARITY Act, which is still a bill, I understand. It’s not yet law. But in general, I understand the GENIUS Act is centered solely on stablecoins. It’s aimed to not only help provide strength to the US dollar as the global reserve currency, but also addresses issues like consumer protection.

[The] CLARITY Act, I’m understanding, offers a more structured approach to the broader digital landscape. So, this includes classification, regulation – stablecoins included, I suppose.

Yes, that’s right.

And then there’s these reserve requirements…. What else can you tell us about these new laws or these new rules – [and] why they’re important to investors, both in traditional and digital asset spaces.

Sure. So, the stablecoin law referred to as the so-called GENIUS Act, which was signed into law in July of ‘25, as you said, basically it gives us for the first time a regulatory framework for what the government calls ‘payment stablecoins’. Now, I think in this case, that refers to stablecoins that are actually backed by dollars, where you can actually audit the dollars. None of this kind of synthetic dollar or, you know, other types of stablecoins, which I mentioned earlier, we won’t bother getting into for today. They’re a little bit more, you know, esoteric. The law clarifies who is permitted to issue these payment stablecoins. It has to be, for example, a subsidiary of an insured depository institution, or a non-bank issuer approved by the OCC, or a state-qualified issuer approved by a state regulator.

So, it’s getting closer to being part of traditional banking regulation.

And so, for example, a couple of international issuers of stablecoins have to now create US-specific versions of those stablecoins in order to comply with the GENIUS Act, because they would be deemed uncompliant based upon the international versions

for their products that are issued outside the US without having a recognized bank be the issuer, for example. And I’m using the word ‘recognized’ bank very, very loosely here, you know, per the law.

Very interesting stuff.

How are reserves audited?

I was interested about proof of reserves for these stablecoins from the GENIUS Act.

[It] seems like it deals more with how traditional finance does these kind of audits, less how blockchain [does], because I know there are solutions in the space for on-chain audits and transparency around that. How do you see that going? Do you think that the current auditing systems are appropriate and sufficient? Should people feel relatively safe with how this is set up? Because there’s been other issues in the past.

I mean, I think this is the problem, and I’m using ‘problem’ here loosely, because I think some of the US-based companies were already compliant with what became the law,

which meant that existing rules kind of dealt with the issue. This is just kind of formalizing what they were already doing. But, basically, what you’re taking is you’re taking a decentralized system, like Ethereum or Solana or Sui, whatever, which has no trusted counterparties in the middle, and you’re adding a trusted counterparty into the system by saying, ‘Okay, anybody can create tokens.’ Any of us can create tokens. It’s actually very easy. You just go to a website, and it will let you create tokens.

The question is, if I’m creating a token and then marketing the fact that these tokens are guaranteed to be equal to a certain number of dollars, the government is now saying, you have to be a regulated financial institution to do that. And the assets that guarantee that the tokens are equal to a certain number of dollars must consist of high quality, liquid assets. Again, the government’s definition of high quality liquid assets – such as US currency, US Treasury bills, maybe overnight repos backed by Treasuries, things like that. And because you’re now a financial institution, you’re getting audited anyway. So, in other words, you’re in a position to publish the fact that those reserves exist because the government is forcing you to go through those audits anyway as a financial institution.

So, you have that redundancy baked into the definition of what it means to be a qualifying financial institution.

That makes a lot of sense.

Yeah.

I have only one question regarding the Tether. So, Tether is the largest holder by market cap of stablecoins, which is around $180 billion, I guess. Now, they are not allowed to operate in New York, due to some violations in 2021, but once the GENIUS Act was announced, they said that they’re going to comply with it, because it gives them three years of time to get complied with. So, Tether’s said that they’re going to introduce a new stablecoin. So, do you have any thoughts about it?

Yeah, the law is very clear now, right? So, what they’re doing outside the US, and I won’t opine how it works, I’m not in the weeds, but they acquiesced and said, ‘Okay, we recognize that as the law is now created, which hasn’t taken effect yet, but will soon, we don’t comply. And we as Tether don’t comply.’ So, they basically said, in my understanding, ‘We’re going to create a US subsidiary with a US banking partner that will issue that stablecoin.’ And they hired somebody, I think it was even from this administration, to lead that effort. And they’ve announced that they will in fact create a US-based version of the Tether dollar, which is then in compliance with the GENIUS Act as it was approved by Congress and signed by the President.

Awesome. Thank you.

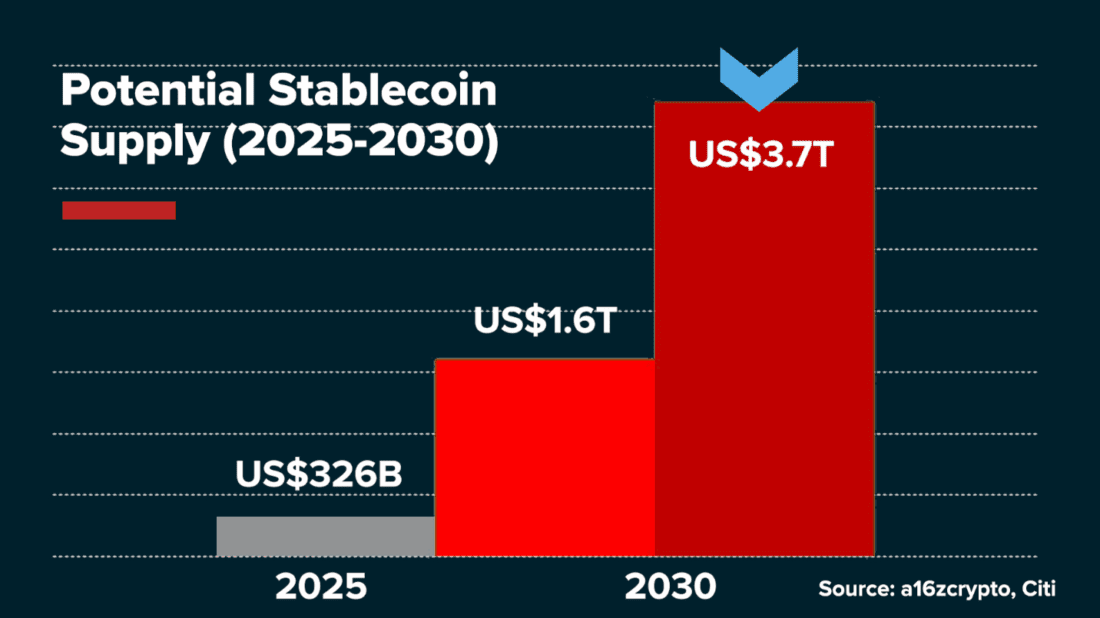

Stablecoin supply set to spike?

Implications on U.S. rates and monetary policy decisions

What really got me, in general, was the projected amount of supply that…. I mean, I read in this industry report, I think it was Citi, and they were projecting that stablecoin supply could reach somewhere between like $1.6- and $3.7 trillion – that’s with a ‘t’ – by 2030. What is it today? It’s like a little bit more than maybe $325 billion, I understand.

And I saw this Fed governor, Stephen Miran, there was an article on him and his speech at the New York Harvard Club recently. He was also talking about this. And it’s a pretty astronomical increase from today, these projected amounts. I mean, it could be a potential rise of, say, 400% to 1,000% at the top end in just five years.

Sources: a16zcrypto, Citi

So, when we’re talking about reserves, when we’re talking about cash equivalents in, say, short-dated Treasuries that are backing these, it triggers some questions about the Treasury market and the Fed.

So, in general, how do you expect these increased purchases of, say, short-dated Treasuries by stablecoin issuers might impact the Treasury market? Do you think it will have some effect on rates and the FOMC’s decisions on monetary policy?

There’s more to it than this as well. There’s also these concerns about maybe potential outflows of foreign currencies into stablecoins. That could also strengthen the U.S.

dollar. That could also have an effect on policy.

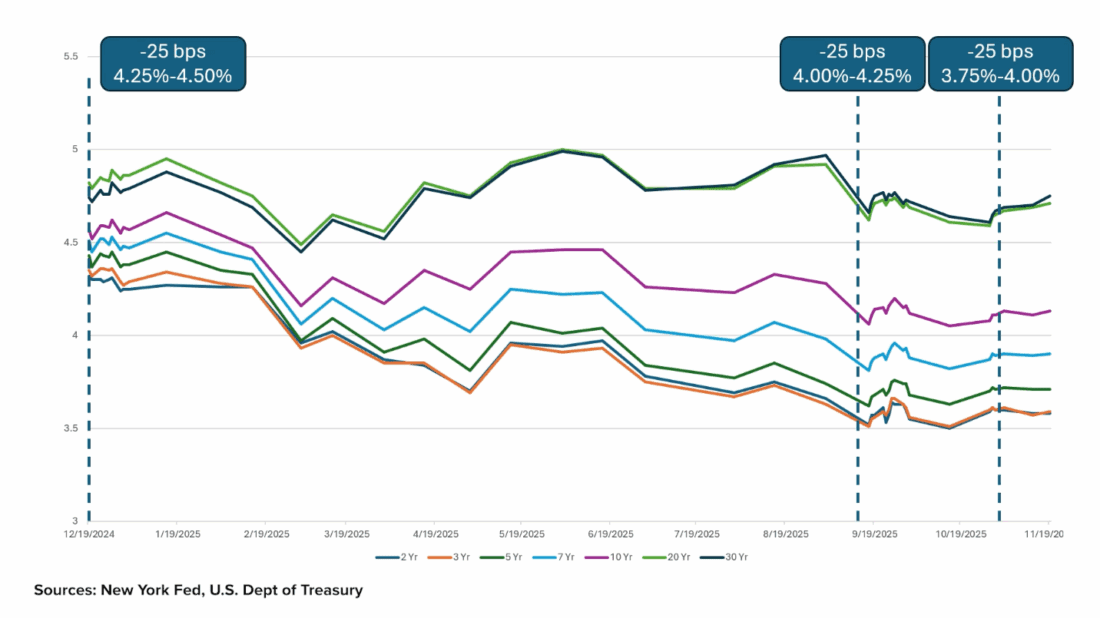

Yes, for sure. Let me rewind a little bit and explain why the Treasury Department and this administration is so bullish on stablecoins. It’s not some fly-by-night, cool thing that they just said American consumers should embrace. There’s actually a very good reason why this is happening the way it’s happening. So, let’s just take what’s happened in the last 18 months independent of stablecoins. The Federal Reserve has lowered rates three times, as I recall, as of this recording. And each time, now historically when you do that, when you lower Fed lending rates, it’s supposed to have a trickle-down effect normally on treasury rates, mortgage rates, et cetera, et cetera, because it’s increasing liquidity in the system, which, in English, means it should lower those other rates as well relatively quickly. In all three cases, the opposite happened, immediately – mid-duration and long-duration bonds yield spiked.

Sources: Federal Reserve Bank of New York, U.S. Department of the Treasury

That’s not supposed to happen. Why did that happen?

I believe it happened for two big reasons:

One, fixed income markets are really worried about the so-called ‘game being up’ and believing that you’re $38 trillion in debt, Mr. Creditor or Mr. Debtor, and nobody wants to buy your debt anymore, which leads to part two, which is that Japan, China, Germany are all net sellers of US debt now. So, if we’re going to refinance all this debt that we have, who’s going to buy it? Well, it turns out that there are only, to my knowledge, three net buyers of United States debt right now, meaning not net sellers or neutral. The first is the banks. And that hasn’t been going so well, because if you allow banks to basically value their Treasuries based upon the actual maturity date, fine; but if you actually do true mark to market, many banks are insolvent by that definition. That’s a very scary proposition.

This is very scary.

Right. The second net buyer is the Fed itself, which means you get to print money in the basement, buy the debt that underlies that money, and try to convince the public that you’re not devaluing the money they’re holding at the same time. And during COVID, we saw what happened when they increased the money supply by 25%. We have lingering inflation they just can’t get contained. And they’re not going to be able to, right? Which has led to the net selling of debt. I think the Russia-Ukraine invasion also created a problem, because we canceled Russia overnight from the banking system, more or less.

But the third net buyer is Tether. Tether is now, to my understanding, a top 15 holder of U.S.

Treasuries globally – and growing. That is an astounding statistic for a space and a company that didn’t exist 15 years ago. It’s incredible. Now, [U.S. Treasury Secretary] Bessent knows this. He’s a very, very smart man. So, he’s saying, ‘Look, I have these two other problems, because there’s nobody else willing to buy my debt the way I really would want them to. But yet I have this new space that’s basically exporting our inflation to countries that do want to hold dollars, Nigeria and other places.’

Tether has hundreds of millions of users in developing markets who would rather hold dollars because their local currency is depreciating way faster than the dollar. Say what we will about the dollar, it’s not depreciating as fast as the Nigerian, I think Naira it’s called, [for example]. So, that has created significant demand for these stablecoins. Also, created demand among people who are willing to forego the yield, because their local currencies are devaluing so fast that they’d still rather hold the dollar even without the yield that goes along with the Treasuries, because Tether is not sharing that yield. They’re keeping it for themselves, which is why they’re the most profitable company per employee in human history, most likely. So, again, when you dig in, this makes sense now.

So, the Treasury Department is saying, ‘Well, wait a minute, if we can get more and more people to adopt the dollar stablecoin around the world – now 300 million and growing quickly, according to them, and Circle, and others. This could, it won’t stabilize rates, but it could certainly dampen them, which is what they want. And, so, the idea that this market could offset the net selling by other countries is extremely compelling. And they understand this even better than we do.

So that’s, I think, a big part of the push to get dollar stablecoins out there, and also why the GENIUS Act focused on the dollar-backed stablecoins, and the reserves that are backed in Treasuries, as opposed to the synthetic dollars and other kind of fancy stablecoins that aren’t mentioned in the GENIUS Act.

Very, very fascinating. And when you think about the holders of US debt, traditionally it comes to mind: it’s China, Japan. These are the two, and I understand they’ve been sellers of Treasuries for some time now.

They couldn’t do it overnight because it would cause rates to spike, and it could create a cascading effect, which could lead to a depression in their home market as well. So, they have to be very careful how they do it, but their stated goals are very clear. They would rather hold gold than our debt. Now, say what you will about China-US relations. We very effectively exported our inflation to China and Japan for 30 years. And that jigs up, right?

So, we need other means to get inflation down – to basically stave off hyperinflation and depression in this country. And so, stablecoins are no magical cure, but they certainly don’t hurt.

Steven Levine

The devaluation of currencies in other countries that you mentioned too, that just brings to mind the swap line that we did with Argentina not long ago. And I know that we’ve had podcast material about Argentina, where that country would prefer, if they could, to hold the US dollars as their alternative currency, or their reserve in general, so that they could transact with them.

In terms of issuance – we talked about Tether. There’s also Circle. I understand Tether’s the USDT. Circle is the USDC. I think they represent something like 85%-90% of the issuance today. And I know you mentioned there were other issuers that are now like exploding into the market. I think JP Morgan, I don’t think this is a ‘true’ stablecoin, but I think JP Morgan rolled out something called a JPM Coin. It’s a Deposit Token. [It] looks like it’s backed by cash deposits held at the bank. There’s also a company, recently, called MoonPay. And they just announced that they are starting a stablecoin business and issuing stablecoins and managing reserves.

It’s just so much activity for me to even keep up with … to even just have this conversation, which is incredible.

Do you think, say, over the next one to two years that Tether and Circle are still going to be the dominant issuers of stablecoins in the market? Or do you think there’ll be other competition – big banks, other big firms?

Nobody’s going to catch Tether and Circle in the short-term, in my opinion, but I do think that their dominance will be diminished over time by a few different things. PayPal is issuing stablecoins now. Ripple is issuing stablecoins. There’s other smaller issues. There’s a few banks, there’s a few crypto companies that are also regulated banks, or have certain licenses, that allow them to issue stablecoins for other companies. And so, they’re just issuing new stablecoins as fast as they can. Again, not a lot of functional difference, but the issuer matters, meaning if it’s JP Morgan, it will have a different use case than if it’s PayPal, obviously. So that’s interesting. And that doesn’t even account for the synthetic or decentralized stablecoins that are out there, like Ethena or Dai, which we’ve not even talked about for now because we’ve really focused on dollar-backed [stablecoins]. But those products are now holding billions of dollars as well. And they have a very different set of use cases, which is much more kind of crypto trading-centric for now; but I think long-term [will] solve a lot of problems in supply chain finance, in cross-border trade, where you may not want to touch the US banking system for whatever reason. I’m not opining if that’s good or bad. It just is. And so, more of these kind of fancy products are going to nip away at the incumbents as well.

It’s just fascinating. There’s all sorts of opportunities, especially with the new framework that was introduced by the legislation, by the GENIUS Act, et cetera. I mean, there’s all sorts of opportunities to innovate now, it seems. I saw Visa and Mastercard – I don’t know how long they’ve had these for, but they’re stablecoin-based debit cards.

Innovation

Stablecoin-based debit card basically means you can bypass the traditional banking system and generally pay your bills, travel, and live a dollar-based life if you want to, even if you’re not in the US. I would say the initial dollar-based stablecoin debit card products I’m seeing so far are more popular outside the US than they are in the US, because for Americans, most people … this is a hard conversation to follow, I’m trying to keep it simple … but the reality is, for a lot of people who have a bank account, they’re like, ‘Okay, I may not like my bank, but what’s the problem again?’

And so, for international people in developing markets, especially, and I did a lot of work in remittances where they just get crushed by fees, this helps a lot because the more hands you take out of the pie, the more of the pie that’s left behind, which is what the consumer wants – or they have access to dollars in the first place, which they don’t today. But now extend that to supply chain finance, other types of cross-border trade, eliminating bank wires. When was the last time you sent a bank wire and said, ‘Oh my God, that was such an amazing experience. I can’t wait to send another bank wire.’

I don’t know if Swift lives up to its name anymore? Is it so swift?

It’s good marketing. But exactly, right? So, again, the easiest way to deal with those things is to shut them down by eliminating the need. So, you know, out with the old in with the new, as they say, and this is the new.

I was going to ask in that space, for the average consumer – obviously internationally, there’s huge benefits to taking out these intermediaries and shortening that time for transactions. For a US consumer or investor who just wants to park their money, are there any advantages to something like USDC over a high yield savings account, or something that would have an insured backing, something that people might feel more safe with?

Yes. So, here’s what I think is going to happen, which – and I’ll relate this to your guys’ world, at IB, for example…. Today, if you look at how crypto works – tokens – and you look at how stocks work, meaning with their custodians and settlement, or bonds, or even real estate with titles, when you buy and sell a house, you reissue a title and you have an escrow for that. That’s all about to be tokenized, all of it.

So, what we’re calling a ‘stablecoin’ now is actually, in reality, a tokenized real world asset [RWA]. The real world asset in this case happens to be the dollar. What you’re about to see happen is you’re going to see real world tokenized versions of stocks, bonds, real estate…. And that’s what Abra does – we basically provide vaults to clients where they can store their digital assets. Today, those digital assets are a combination of crypto and stablecoins. They’re about to become everything.

And you might say to yourself, well, why does that matter? I think there’s three reasons why it matters. The first is, today you operate in your world, in this highly regulated world of stock trading where stock markets are closed more than they’re open, whereas crypto trades 24-7, and you can’t shut it off. So, you’re about to merge tokenized stocks into that world. So, you’ll have 24-7 liquidity, and all of those assets will be fungible, meaning I’ll be able to trade my tokenized Apple for Bitcoin, my tokenized Apple for USDC, my USDC for tokenized Nvidia, whatever, or even for gold.

The third part is the same way I can borrow against Bitcoin now, I can borrow against the value of all of those tokens because they’re all fungible. The only thing that’s required for me to be able to borrow against something is that I can easily sell it if you don’t pay back the loan. You don’t pay back your HELOC loan on your house, eventually the bank’s going to confiscate your house and sell it to pay back the loan.

So, if you can tokenize Apple shares or Nvidia shares or gold or even your house for that matter, they all become fungible for purposes of borrowing against them. That’s actually, in my opinion, the future of wealth management, the future of banking, and they merge.

And that’s what we’re focused on at Abra is helping even companies like yourselves to be able to facilitate that over time. And that’s where this is headed.

I’d love to hear more about what Abra is working on, or has either in the works, or has initiatives currently, that align with your vision for how you see what investors probably are looking for in, say, the next one to three years in the space?

That’s a good question. Today, what we’ve done is we’ve built the next generation wealth management platform to be able to deal with these digital assets. Our clients are high net worth investors, family offices, institutions that want exposure to the space, want to earn yield on the assets they’re holding, whether it’s Bitcoin or Ethereum, Solana, whatever.

They want to be able to borrow against those assets. A lot of our clients got in very early in Bitcoin. It went from 1% of their holdings to 50% of their holdings, because the price went up so much. They don’t want to sell, because they believe the price is going to continue to accrue and they don’t want to have to pay taxes on those gains. They can very easily, in our system, borrow against the value of the Bitcoin at a relatively modest LTV. And if the price goes up more, they can borrow more. And, like I said, in the future, that will include other types of tokens, whether it’s tokenized stocks or the tokenized title to your house or whatever the marketplace deems is liquid enough to be able to facilitate those types of credit instruments.

I think the bank account of the future will be a vault that will be the sum total value of all of those tokenized assets. A credit card will simply give you a credit line against all of it, and it won’t be a physical credit card. It’ll just be some virtual set of numbers. So, that’s where we’re headed.

Today, what we’ve done, is we’ve built a very simple model to help our own clients navigate the space, be able to buy, sell those tokens, be able to earn yield on them, borrow against them. We’re now helping other wealth advisors do the same thing for their clients. And then the next generation for us is helping to facilitate this tokenization of real world assets as well. Stocks, other types of stablecoins, potentially fixed income instruments, et cetera, et cetera.

This is a very, very interesting thing to my mind with tokenizing stocks and other assets.

I think it’s all really interesting. I mean, just one question quick about taking out loans on something like Bitcoin that many would consider as a highly volatile asset. Even in the last month being down almost 20% … how does that work if someone takes out a loan, and the asset price drops? Does that change the loan structure, those thresholds?

Source: IBKR Trader Workstation

When you take out a loan against an existing asset, like a home equity line of credit,

or a loan against your Apple shares, you end up with what’s called a loan to value ratio. And anybody who’s taken out a loan against one of those knows what an LTV or loan to value ratio is. So, for Bitcoin in particular, because it’s what we call a ’30-vol asset’, which means the average volatility over a 12-month period would fluctuate 30% in either direction. We would recommend that they keep that LTV for the initial loan, probably in the 35% to 45% range. And this would allow them to keep from getting liquidated if the price falls, like you said … 25%, 30%. And if there’s a spike down, our system monitors what’s happening and would send the client a notification that says, ‘Oh, your LTV is getting too high. You may want to consider adding more Bitcoin collateral, so you don’t risk selling any of the Bitcoin’, which is usually the number one requirement from our clients. ‘I don’t want to sell my Bitcoin.’

The system is very good at monitoring that. And we, as a fiduciary, generally recommend to our clients – keep the initial LTV relatively low, and then you can either add more Bitcoin over time, or as the price increases, you can draw down more. And generally our clients follow that advice.

Are these loans handled by Smart Contracts? For example, there’s a quick drop.

Do they have a buffer to be able to recalibrate that, or is there more urgency to those sorts of matters?

They’re self-regulating Smart Contracts is the tech way to explain it. From the consumer’s perspective, it’s just a marketplace, which basically has buyers and sellers. It has people who want to borrow one asset and earn yield on another asset. And the system marries the two, which creates the dollar supply that’s available to borrow at any given time, creates the rates for depositing Bitcoin to earn yield. And we help facilitate liquidity into those marketplaces via large depositors and large borrowers in our marketplace.

Awesome. Thank you.

Awesome. Awesome.

This was really great. Bill, thank you so much.

Thank you. Thank you.

Absolutely.

I also wanted to thank Celisa Morin, who runs your strategic partnerships. She’s been really great. She really helped me with a lot of material. So, thank you, thank you, thank you. Abra’s been doing me a lot of good in my own education, which is really terrific.

Tim, Jawahar, thanks very much for taking the time to do this, too.

And I want to let our listeners know that they can learn more about Abra at abra.com.

And you can read more commentary and market analysis, including about the crypto markets at IBKR Traders Insight – a lot of great content there. We also have more information about IBKR’s crypto offerings on our website, just go to ibkr.com.

And for a full list of financial educational offerings, visit the IBKR Campus, where as always, all of our educational material is provided to the public at no cost.

Until next time, I’m Steven Levine with Interactive Brokers.

Thanks for joining us.

LEARN MORE

Central Bank Digital Currencies – The Future Shape of the Financial Sector (May 3, 2022)

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Stablecoins and Tokenized assets are not legal tender, are not insured by the FDIC or any government agency, and may lose value; they carry risks including issuer insolvency, regulatory changes, operational failures, and potential inability to redeem for fiat currency. By transacting in stablecoins, you acknowledge and accept these risks.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. Eligibility to trade in digital asset products may vary based on jurisdiction.

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!