- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted March 31, 2026 at 12:56 pm

News that President Trump is considering an end to the Iran war even without a reopened Strait of Hormuz is sparking a Turnaround Tuesday on Wall Street. A pair of economic reports depicting a slight increase in consumer confidence alongside stable job openings also supported a revival of animal spirits in markets while dampening slowdown angst. Major averages are all advancing more than 1.2% on the session as a result and rebounding from yesterday’s intraday reversal with almost every sector and subcomponent gaining except for the defensive utilities and staples categories. Treasuries are rallying too and were additionally helped by Federal Reserve speakers, including Chair Powell, that were relatively dovish compared to their global counterparts on how the Middle East conflict could influence increasingly restrictive monetary policy. Comments over the past few days have effectively eliminated a rate hike from the conversation in 2026 although the central banks of Australia, Japan, Europe and the UK are poised to lift their benchmarks. There’s certainly a heavy amount of confusion and uncertainty in the skies and commodity traders appear the most pessimistic of them in today’s tape, with the entire complex higher while WTI crude is still climbing north of $105 this morning despite the optimism in other asset classes. Elsewhere, cryptocurrencies and forecast contracts are catching bids, while volatility protection instruments and the greenback slide in light of risk-on attitudes and looser financial conditions.

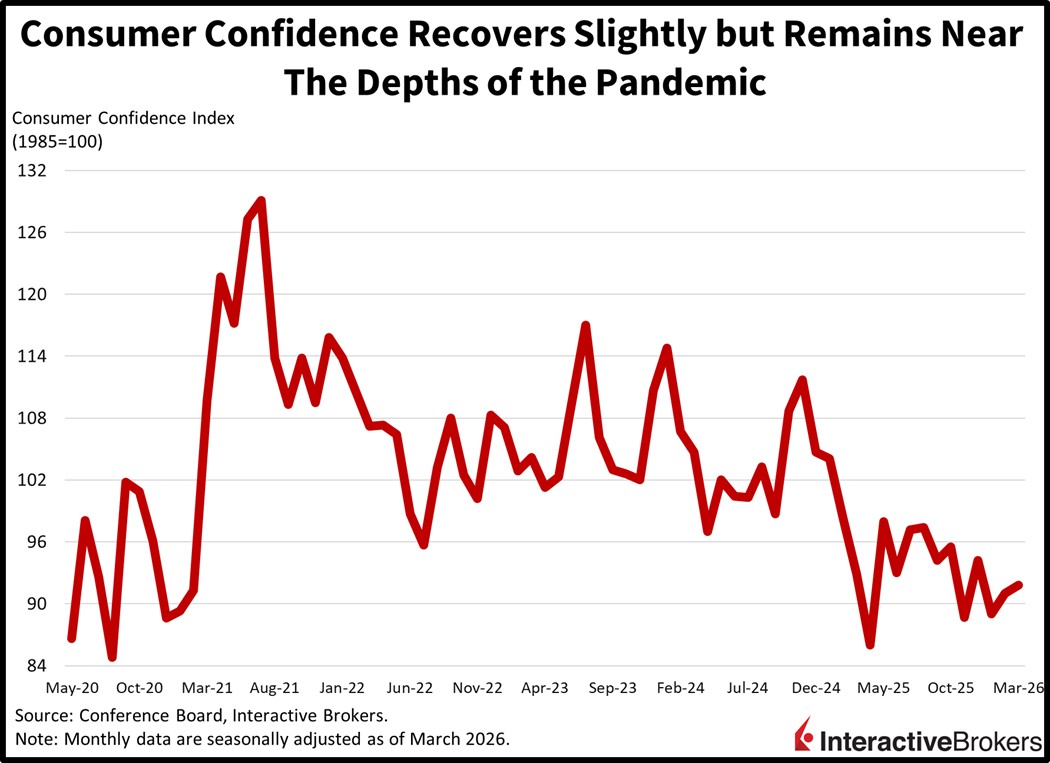

Consumer confidence improved slightly this month although shoppers’ moods remained nearly as pessimistic as they were during the pandemic. The Conference Board’s 91.8 headline March number was well above the median estimate of 88 and February’s 91. The current conditions sub-component increased, which offset the decline in the expectations segment, as the indicators moved from 118.7 and 72.6 to 123.3 and 70.9. Folks felt better about present business opportunities while views on employment were steady. Regarding the future, however, respondents were increasingly negative as it pertains to entrepreneurial possibilities and labor prospects while not as gloomy about their personal outlooks for income generation. Overall, participants appeared burdened by the cost of living and the Middle East conflict’s effect on gasoline prices. Indeed, survey participants hiked their projections of inflation and interest rates as a result. Additionally, shoppers believe the probability of a recession has increased and individuals are less bullish on stock market performance.

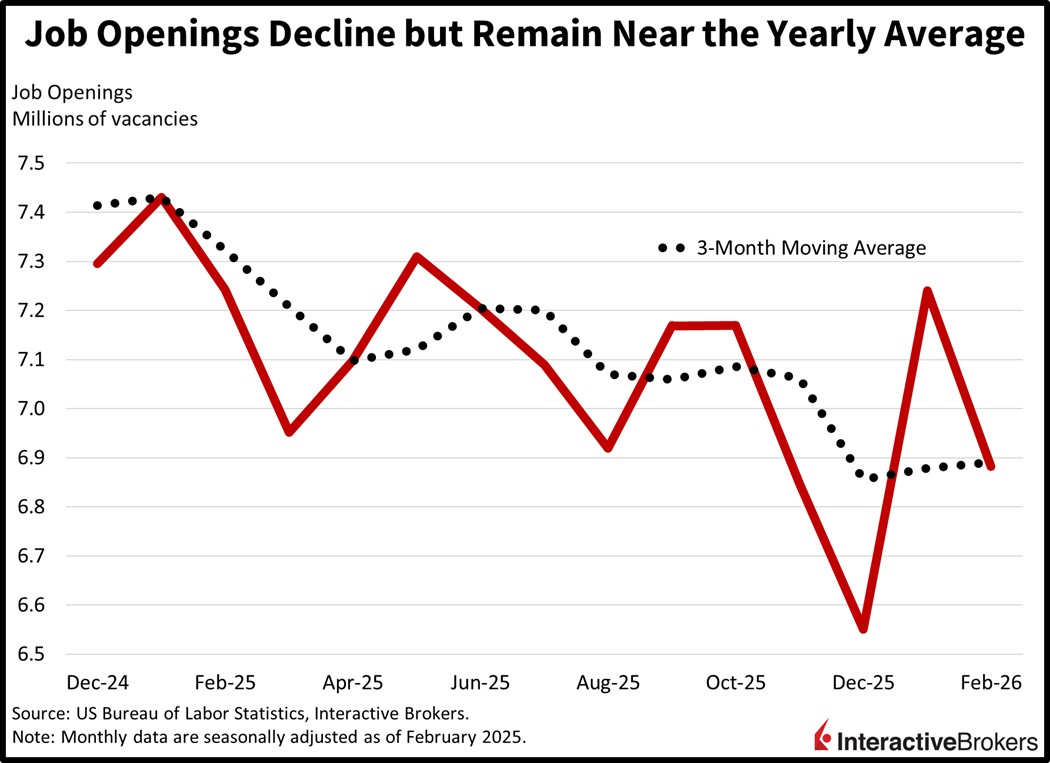

For-hire signs declined in February but remained in a healthy range near the indicator’s 12-month average, serving to support optimism about employment conditions. Job openings slipped to 6.882 million last month, slightly under the median estimate of 6.92 million and beneath January’s 7.24 million. The largest reductions were in the accommodation/food services, manufacturing, government and healthcare/social assistance which saw vacancies drop 211k, 71k, 51k and 51k. Conversely, other services, professional/business services and retail were offsetting factors, adding 77k, 64k and 24k. Quits, released in the same report, decreased from 3.131 million to 2.974 million, signaling reduced worker confidence as it pertains to replacing their employers.

If and when a ceasefire deal is finalized, a key factor for market watchers will be how low oil prices will go after peace in the Middle East is reached. Of course, an end to the war would bolster economic fundamentals and cyclical health; however, the damage that has been done to energy infrastructure facilities in a region that houses a third of global crude supplies is significant. Furthermore, we started the year with West Texas Intermediate (WTI) at around $57 against the backdrop of analysts expecting a plethora of barrels in the pipeline amidst downside risks to the commodity’s cost. But a return to normalcy is highly unlikely to get us back to the 50s, as we’re poised to stay somewhere in the 70s, which while marking a material improvement from the $105 level of the moment, would still weigh on rate cut prospects, profit margin profiles and the growth/earnings outlook while lifting inflation expectations and sustaining elevated Treasury yields.

Euro area inflation as depicted by the preliminary Harmonized Index of Consumer Prices accelerated from the 1.9% year-over-year pace in February to 2.5% this month with the Iran War pumping up energy costs. The gauge, while being a tad cooler than the economist median estimate of 2.6%, places inflation considerably above the European Central Bank’s 2% target. Relative to the preceding month, costs climbed 0.7%, matching February’s month-over-month (m/m) gain.

For the y/y result, the following categories and the extent of their changes contributed to the headline increase:

When excluding energy and food, which have volatile prices, the euro area preliminary Core CPI depicted easing price prices with the annual rate falling from 2.4% in February to 2.3%

Two weeks ago, the European Central Bank left its key interest rates unchanged while warning that the Iran war could cause inflation to soar above the organization’s target and that a prolonged Middle East war could keep price growth strong for years.

Canada’s gross domestic product grew 0.2% m/m in February, according to a preliminary print. The result is a slight increase from the 0.1% expansion in the preceding month. In February, finance, insurance, manufacturing, mining and quarrying contributed to the positive number while agriculture, forestry, fishing and hunting were headwinds.

Prices in the UK climbed 2.2% y/y in March after ascending only 1% in February, according to the Nationwide Housing Price Index (HPI). On a m/m basis, prices were 0.9% higher, a stronger showing than both the economist consensus estimate for a 0.6% increase and February’s 0.3% gain. The strong results occurred in most major regions, but financial services firm Nationwide cautions that the Middle East war is creating headwinds that could dampen demand for housing. Nationwide anticipates that the conflict will cause inflation to climb and economic growth to slow. Meanwhile, the outlook for interest rates is highly uncertain as it’s unclear to what extent the conflict will have on supply and demand. With recent developments, markets have increased their expected number of BoE rate cuts this year from two to three, which is likely to cause mortgage rates to climb. On a positive note, aggregate household finances are strong with low debt levels and significant savings, which could buffer the economic impact of the ongoing war.

Retailers increased their prices by 1.2% in March relative to the year-ago period with high costs working their way through supply chains, according to the British Retail Consortium Shop Price Index. The ascent was slightly stronger than the 1.1% y/y print in February but matched the economist consensus estimate. The survey was conducted from March 1 to March 7, so it doesn’t reflect more recent inflationary pressures. For the y/y result, food inflation hit 3.4%, easing from 3.5% in February, and non-food items rose by 0.1% after sinking 0.1% in the preceding month. The organization warns that new labor and healthy foods laws could also increase retailers’ costs and push up inflation.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. Eligibility to trade in digital asset products may vary based on jurisdiction.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

")

These types of short-covering rallies can be ferocious. Getting ahead of overhead resistance might not be as easy.