- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted January 16, 2026 at 12:45 pm

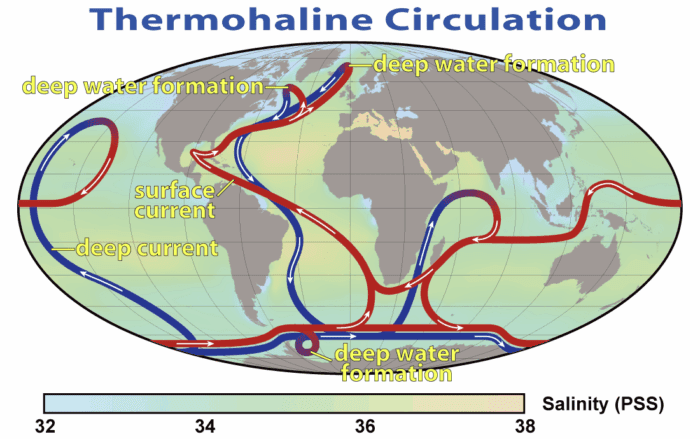

The Atlantic Meridional Overturning Circulation (AMOC) is an ocean circulation (C) that spans the Atlantic (A), is primarily oriented North-South (Meridional, M), and transports water between the surface and depth (overturning, O). Its most relevant characteristic for climate is that it moves warm surface water from the tropics northward toward higher latitudes in the North Atlantic basin. As water moves north, it loses heat to the atmosphere, becomes denser than water to the south, and sinks, then returns southward at depth as a cold deep current.

Popular stories on climate change often equate the AMOC with the Gulf Stream, but this is not accurate. The Gulf Stream is the fast, narrow surface current that hugs the U.S. East Coast and then turns eastward across the Atlantic. The AMOC includes the Gulf Stream but also the broader pattern of northward surface flow, regions where water actually sinks in the high-latitude North Atlantic, and the slow southward return flow of dense deep water.

If you have seen the movie The Day After Tomorrow, you have watched a Hollywood depiction of a shutdown of the AMOC, which suddenly plunges Europe and North America into an ice age. The depiction is loosely based on real ideas about the climate system, but, among other inaccuracies, it condenses ocean dynamics that would unfold over centuries into a few days.

Nevertheless, an AMOC shutdown is among the most widely discussed climate “tipping points” (or, technically, tipping elements): parts of Earth’s system that can shift into a very different state once a threshold is crossed, often with self-reinforcing feedbacks that sustain the new state. The AMOC is considered a tipping element because feedbacks involving salt and heat can, at least theoretically, make it bistable. In one state, the circulation is strong: dense, salty water forms in the subpolar North Atlantic, sinks, and pulls warm surface water northward. In another state, North Atlantic surface waters are fresher and lighter, reducing sinking, weakening the overturning, and decreasing the associated northward heat transport. Model experiments and paleoclimate evidence suggest that during past glacial periods, the AMOC may have switched between these modes, contributing to sudden climate changes (especially in the North Atlantic).

Since the AMOC transports heat northward in the Atlantic, a significant decrease in its strength would affect regional temperature patterns, rainfall, sea ice, and sea levels. Model experiments that artificially weaken or shut down the AMOC show cooling in the North Atlantic, warming in parts of the South Atlantic, and shifts in tropical rainfall belts. Paleoclimate records of past abrupt climate events generally match these patterns.

For a complete shutdown, some simulations indicate that the North Atlantic could cool by several degrees Celsius, the tropical rain belt might shift roughly ten degrees of latitude southward, rainfall over the North Atlantic region could decrease, storm tracks might change, and Arctic sea ice could increase (or decrease more slowly).

Advanced global climate models consistently project a weakening of the AMOC under ongoing greenhouse-gas emissions. The strength of the AMOC is usually expressed in Sverdrups (Sv), with one Sverdrup equal to one million cubic meters (of water) per second and analyses of CMIP6 (Coupled Model Intercomparison Project Phase 6) climate model simulations constrained by RAPID observations indicate a mean decline of approximately 6–8 Sv at 26.5°N by 2100, corresponding to about a 30–45% weakening relative to current levels (Weijer et al. 2020, Wang et al. 2023). This projected reduction is surprisingly similar across different emissions scenarios at least through mid-century, suggesting that the AMOC response over the next few decades is more influenced by the accumulated changes so far than by the specifics of future mitigation strategies.

However, a complete collapse (in which overturning essentially ceases) is not considered likely, at least in the twenty-first century. Specifically, the Intergovernmental Panel on Climate Change’s Sixth Assessment Report states that, while the AMOC is very likely to weaken over the 21st century, there is medium confidence that this decline will not involve an abrupt collapse before 2100.

Still, a 30–45% weakening could have notable regional effects, including cooling in the subpolar North Atlantic by a few degrees, changes in storm tracks over Europe and North America, and shifts in precipitation patterns. Importantly, these changes would occur on top of a globally warming background. In some regions, especially parts of Europe, AMOC-related cooling could offset some greenhouse warming, resulting in a smaller overall temperature increase than would occur without any AMOC slowdown. In other areas, such as parts of the tropics and the Southern Hemisphere, heat redistribution could amplify warming.

A subjective assessment of the scientific literature suggests that a significant weakening of the AMOC this century is likely, while a total collapse is considered a low-probability event. However, prediction markets can help us pinpoint the center of mass of sentiment with greater precision.

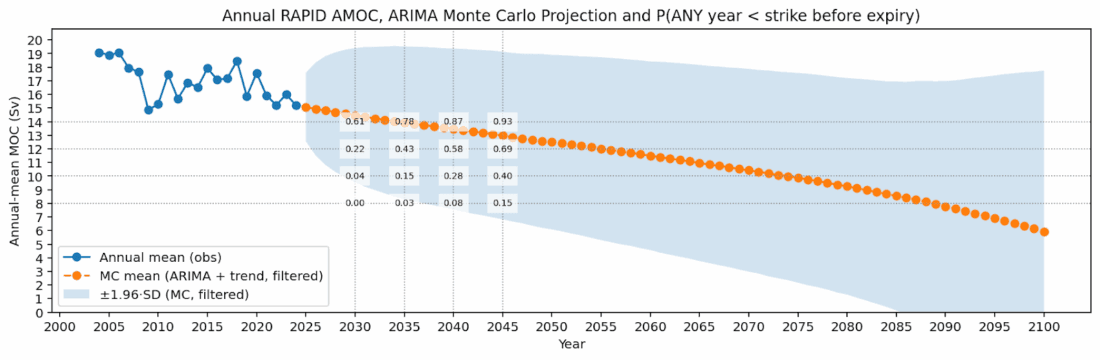

Since 2004, the RAPID (Rapid Climate Change–Meridional Overturning Circulation and Heatflux Array) program has been measuring the AMOC continuously at 26.5°N using a line of moorings stretching from the Bahamas to Africa. This array provides an ongoing, publicly accessible time series of AMOC strength, which serves as the observational foundation for ForecastEx’s prediction markets, which use it to define a set of binary AMOC contracts.

Each contract is specified by two numbers: a threshold for the annual-mean AMOC strength and a final year indicating the end of the observation period. The underlying measurement for all contracts is the annual mean AMOC in Sverdrups, as measured by the RAPID array, and the question is whether any calendar-year average will be below the threshold by the end of the observational period. Final years extend from 2030 to 2045 in 5-year increments.

Figure made in Python with Matplotlib

To calculate the initial seeding probabilities above, I used the RAPID array’s time series of AMOC strength (blue line above) to fit an autoregressive model with a linear trend that captures the long-term trend and how the circulation fluctuates around it from year to year. Using this fitted model, I generated thousands of Monte Carlo simulations of annual AMOC strength extending through 2100. Each simulation represents one plausible future pathway based on what we have observed so far regarding variability and the long-term trajectory.

Next, I incorporated information from physics-based global climate models. As mentioned earlier, CMIP6 models constrained by RAPID observations tend to show a 6–8 Sv decline by 2100. To reflect this, I retain only the Monte Carlo simulation trajectories whose long-term decline falls within a range centered on the climate-model-based estimate, and I exclude paths that exhibit unrealistic patterns, such as a sharp collapse followed by a full recovery. What remains is a set of future scenarios grounded in observations and aligned with the long-term decline forecast by physics-based climate models.

The filtered Monte Carlo ensemble not only produces the average path and confidence band shown in the figure above; it also offers a natural way to estimate the chance that each contract will resolve to YES. For each threshold–final year pair, I simply count, across all simulated futures, how often the AMOC crosses the threshold in any full year before the expiration. The fraction of simulations in which this occurs is an estimate of the probability that the contract resolves YES.

The goal of these calculations is to give a clear and defendable starting point. New RAPID data, fresh climate model results, or new early-warning signs could all change sentiment. Traders who believe these probabilities are too high or too low are free to take the opposite side.

Different participants might find these contracts appealing for various reasons, and their stances will mirror their substantive views on AMOC risk.

Someone inclined to buy YES may believe that mainstream climate models underestimate AMOC instability or that recent observations already indicate an approaching tipping point. They may emphasize early-warning indicators such as changes in AMOC variability or spatial patterns that are not fully represented in standard model ensembles. They might also expect higher-than-mainstream estimates of greenhouse gas emissions and/or freshwater sources associated with rapid Greenland melt, which could accelerate the AMOC’s transition toward a weak state.

YES can also serve as a hedge against risk. A European utility that must purchase energy to meet heating demand could buy YES contracts as a form of financial protection. Insurers and reinsurers with large portfolios in North Atlantic and European markets, or long-term investors in North Atlantic coastal infrastructure, might use YES contracts to hedge exposure to shifts in storm tracks, flood risk, or agricultural yields that could result from a weakened overturning.

On the other hand, a trader inclined to buy NO is likely to view the AMOC as more stable than the public debate suggests. They might highlight the short length and noise in the RAPID record, interpret recent trends as part of natural variability, or view “tipping point” stories as exaggerating what models show. They may accept that the AMOC will weaken but believe the thresholds and timelines in the ForecastEx contracts are too aggressive, concluding that the market will overpay to hedge against low-probability tail events.

Overall, the AMOC sits at the crossroads of sensational public narratives and serious scientific concern. Popular narratives often convey AMOC as a “climate tipping point” that will tip Europe into an instant catastrophe. Research supports the general notion that the AMOC is a “tipping element” and that a substantial weakening this century is a realistic possibility, even though a complete collapse remains unlikely.

The AMOC contracts at ForecastEx represent a means by which risk can be priced, hedged, and debated quantitatively. The AMOC forecast contracts won’t tell us with certainty whether a major weakening will happen, but they will indicate what the capital-weighted consensus thinks the odds are at any given time.

New to Prediction Markets?

Open a Prediction Markets AccountThe analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Interactive Brokers LLC is a CFTC-registered Futures Commission Merchant and a clearing member and affiliate of ForecastEx LLC (“ForecastEx”). ForecastEx is a CFTC-registered Designated Contract Market and Derivatives Clearing Organization. Interactive Brokers LLC provides access to ForecastEx Forecast Contracts for eligible customers. Interactive Brokers LLC does not make recommendations with respect to any products available on its platform, including those offered by ForecastEx.

This is commentary on economic, political and/or market conditions within the meaning of CFTC Regulation 1.71, and is not meant provide sufficient information upon which to base a decision to enter into a derivatives transaction.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!