- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted January 7, 2026 at 12:51 pm

The S&P 500 hit a fresh all-time high for a second consecutive session this morning as yesterday’s cyclical leadership passed the baton to today’s tech outperformance. The Dow Jones Industrial Average also marked a new record in early trading, bolstered by supportive economic data before reversing into modest losses. Solid job gains reported by ADP were followed by the sharpest acceleration in services sector activity in 14 months, as detailed by ISM. Coincidentally, the market didn’t pay much attention to a 14-month low in labor vacancies since the numbers are stale from November and the report’s quality could have been adversely affected by the government shutdown. Still, the JOLTS and ADP misses have investors reaching for duration, as the yield curve sinks in bull-flattening fashion led by the long-end. Another thing helping Treasuries is Washington stating that it will control Venezuelan energy supplies, which is generating a crude selloff and leading to lightening inflation expectations. Despite the rallies in equities and fixed-income, volatility protection instruments and the greenback are experiencing demand, against the backdrop of just 3 out of the 11 major sectors in stocks advancing. Commodities ex natural gas are getting battered and so is crypto as Bitcoin and Ethereum are both down over 3%. Conversely, forecast contracts are catching bids.

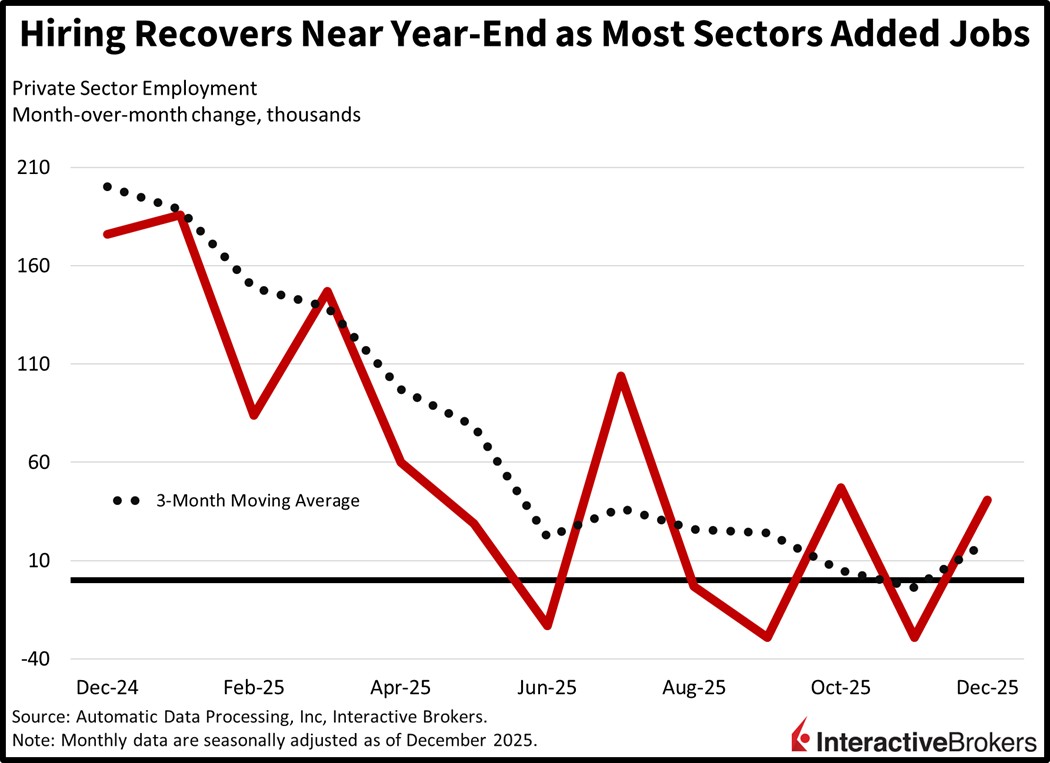

Private sector hiring recovered last month as business confidence strengthened against the backdrop of a reopened government, an improving economic outlook and expectations for additional Fed rate cuts this year. Still, the 41k payroll expansion depicted by the ADP National Employment Report missed the median estimate of 47k despite rebounding from November’s loss of 29k. The year-end gains were broad based as 7 out of 10 sectors added workers. The following categories and the number of new recruits expanded payrolls:

Conversely, professional and business services, information, and manufacturing dropped by 29k, 12k and 5k. Mid-sized businesses with between 50 and 249 employees led by adding 34k, but small and large firms also contributed, albeit more modestly, by boosting headcounts by 9k and 2k. Wage growth rose in aggregate, with the year-over-over (y/y) change in annual pay accelerating from 6.3% to 6.6% for job changers while remaining at 4.4% for stayers.

Services sector activity accelerated to a 14-month high in December with buoyant consumer demand creating a sharp rebound in hiring. The Institute for Supply Management’s (ISM) Purchasing Managers’ Index rose to 54.4 during the last month of 2025, the highest level since October 2024. The result flew past the expected 52.3 and the 52.6 from November. Exports were an additional tailwind, growing at a clip of 54.2, much higher than the previously reported 48.7. Despite the momentum, price pressures cooled with increases occurring at the slowest pace since March.

Job openings dove to a 14-month low in November as the 7.146 million headline missed the 7.6 million median estimate by a wide margin. Additionally, the Bureau of Labor statistics marked a sharp slip from October’s 7.449 million. The most notable month-over-month (m/m) changes featured declines in the accommodation/food services, transportation/warehousing/utilities and wholesale trade sectors, which saw vacancies drop 148k, 108k and 63k. On the other hand, construction for-hire signs increased by 90k.

The huge milestones of 7k on the S&P 500 and 50k on the Dow Jones Industrial Average are within reach, with today’s peaks on both benchmarks less than 1% from those big round numbers. The next catalysts that could send the indices above those levels are nonfarm payrolls and the Supreme Court Justices’ opinions on tariffs that are expected this Friday. Wall Street will be craving a jobs number similar to what we saw from this morning’s ADP, a result slightly below the 60k expectation that is supportive of lighter yields but doesn’t raise economic slowdown concerns. Turning to President Trump’s authority to implement broad duties on international nations, a blockage of the levies would lift interest rates in light of heavier term premiums resulting from a worsening fiscal picture; however, such a ruling would increase corporate earnings expectations due to lower import costs and smoother trade routes. That action would also weigh on the White House’s onshoring ambitions and reduce the impact of the 100% first-year depreciation on capital expenditure that was part of the administration’s signature taxation bill in 2025. Finally, the inflationary impacts of the policies are already behind us, with price pressures receding to the mid 2s and likely to be in the low 2s by April, widening the path for additional rate cuts in the coming Fed meetings, which alongside a reacceleration in growth, is conducive to a broadening equity market.

The Ivey PMI, which is based on purchasing activity in Canada, climbed from 48.4 in November to 51.9 last month and exceeded the contraction-expansion threshold of 50. It also surpassed the economist consensus estimate of 49.5.

The Australia Consumer Price Index was up 3.4% y/y in November, a deceleration from 3.8% in October. Relative to October, prices were up 0.2% with housing and communication costs climbing 0.9% and 0.6%. The alcohol and tobacco category was also up 0.6%. The education group, the transport category and insurance and the financial services sector followed with stickers up 0.4%, 0.3% and 0.3%. Costs of health care and furnishings, household equipment and services, meanwhile, sank 0.2% and 0.4%.

Prices in the euro area climbed 2% y/y in December, which matched the economist consensus and slowed from the 2.1% pace in the preceding month. Perhaps more importantly, the report is in alignment with the European Central Bank’s inflation target thanks to softening energy expenses. On a m/m basis, however, the preliminary Harmonized Consumer Price Index from Eurostat showed that prices climbed 0.2% after a 0.3% November retreat. When excluding energy, the benchmark was up 0.3%.

For the m/m result, services costs rose 0.7% and the energy, food, alcohol and tobacco category climbed 0.3%. Within the latter category, unprocessed foods were 0.8% more expensive. In a favorable development for consumers, energy costs slipped 0.8%. Relative to the year-ago period, unprocessed foods led price pressures with a 4.2% gain followed by the 3.4% hike for services. Energy, however, was down 1.9% relative to December 2024.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Forecast Contracts are only available to eligible clients of Interactive Brokers LLC, Interactive Brokers Canada Inc., Interactive Brokers Hong Kong Limited, Interactive Brokers Ireland Limited and Interactive Brokers Singapore Pte. Ltd. Forecast Contracts on US election results are only available to eligible US residents.

Futures, event contracts and forecast contracts are not suitable for all investors. Before trading these products, please read the CFTC Risk Disclosure. For a copy visit our Warnings and Disclosures Page.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. Eligibility to trade in digital asset products may vary based on jurisdiction.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!