- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted March 4, 2026 at 12:57 pm

(Today’s theme song by Jimmy Cliff)

Although US markets have seen volatility increase in response to the situation in Iran, it pales in comparison to various markets abroad. Compared with most major global indices, the S&P 500 (SPX) has been downright somnolent. On the positive side, after months of underperformance, the placidity of SPX has proven a boon to US investors this week. As we see a resurgence in risk assets this morning, we should also be looking ahead to this afternoon’s earnings report from Broadcom (AVGO).

I got my start trading international equities, and old habits die hard. Like many of you, I check the performance of overnight US index futures shortly after the alarm rings. (I am also convinced that at least some of you then hit the “buy” button almost immediately.) I then move quickly to see what Treasuries and key global indices have done while I was asleep. This week, while there have been some relatively large drops in US futures, the moves in various foreign markets have been far more substantial. But that’s the flip side of a months’-long pattern – many of those markets were significant outperformers on the upside.

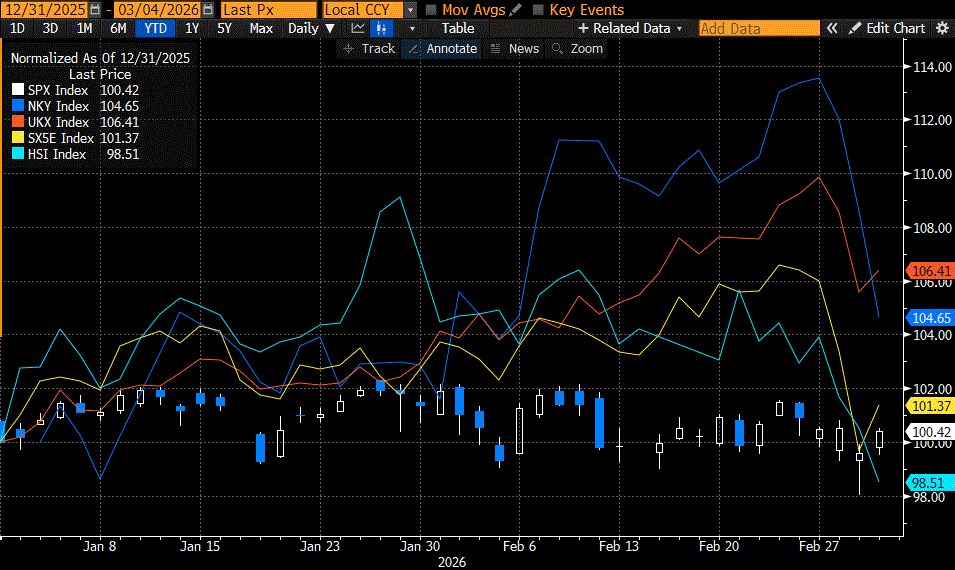

Coming into this morning, SPX was essentially flat. As of yesterday, it was down less than ½% on a year-to-date basis, and as I type this, thanks to today’s bounce, that index is up by a similar amount. This return is rather unexceptional when compared to several other countries’ flagship indices, particularly in Asia and emerging markets. At their peaks, indices like Japan’s Nikkei 225 (NKY), Brazil’s Bovespa, and especially South Korea’s KOSPI had put in double-digit gains in just the two months since the start of the year. The chart below shows the normalized year-to-date performances of various key developed market indices. Depicting SPX with candlesticks saves it from looking like a nearly flat line.

Source: Bloomberg

But the truly stellar chart belongs to the KOSPI. You may have seen headlines about a market crash in Korea, and they are hardly hyperbole. That index fell 12% overnight, a record percentage drop, bringing its two-day loss to 18%. That’s almost a bear market! To be fair, this comes after an absolutely phenomenal run-up; the index is still up over 20% year-to-date! The key catalyst was the global demand for memory chips, pushing key manufacturers like Samsung and SK Hynix to heavy weights in that index and accelerating performance. As a result, the move in KOSPI is stunningly reminiscent of another recent parabolic run-up and bout of profit-taking — that of silver.

Source: Bloomberg

On a morning like this, or after the substantial intraday bounces over the past two days, we might think that US investors are relentlessly optimistic – and that’s largely true. Dips are continually perceived as buying opportunities, and stocks are prone to rally sharply on any optimistic developments. But when compared to the mood in many markets, our exuberance seems hardly irrational.

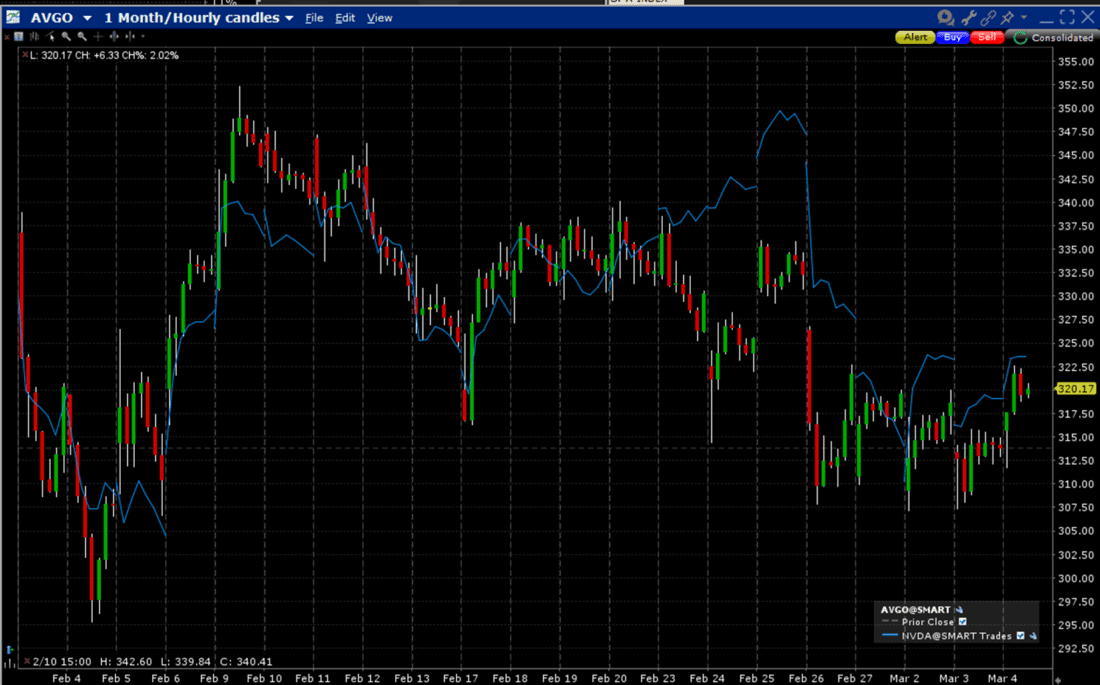

Today we get a key set of results in the tech sector when AVGO reports after the close. The stock has been on a bit of a decline since about three weeks ago, with last week’s selling in Nvidia (NVDA) after a set of positive results further dampening the mood:

Source: Interactive Brokers

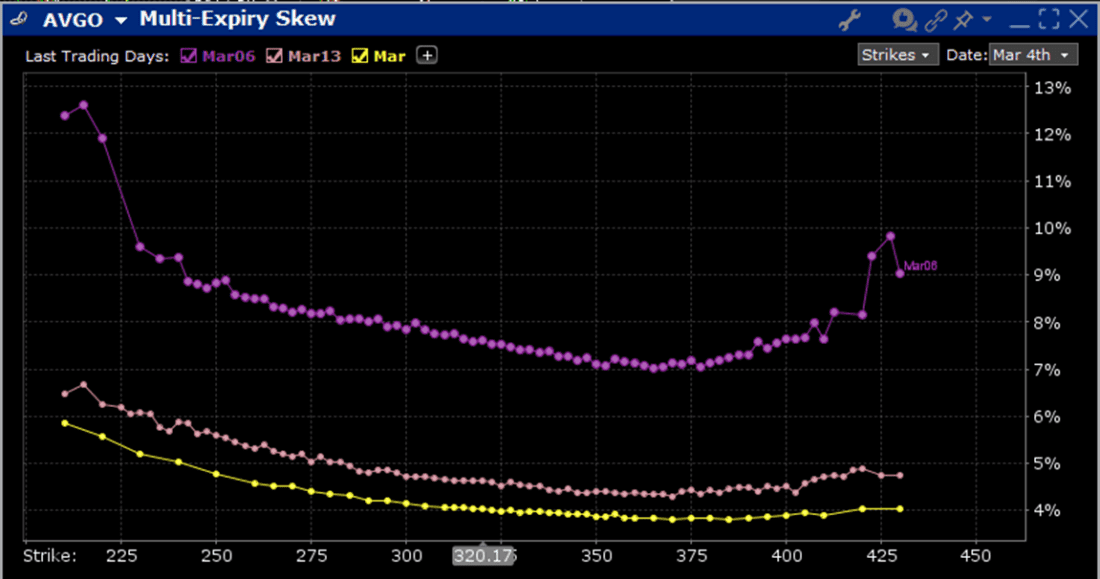

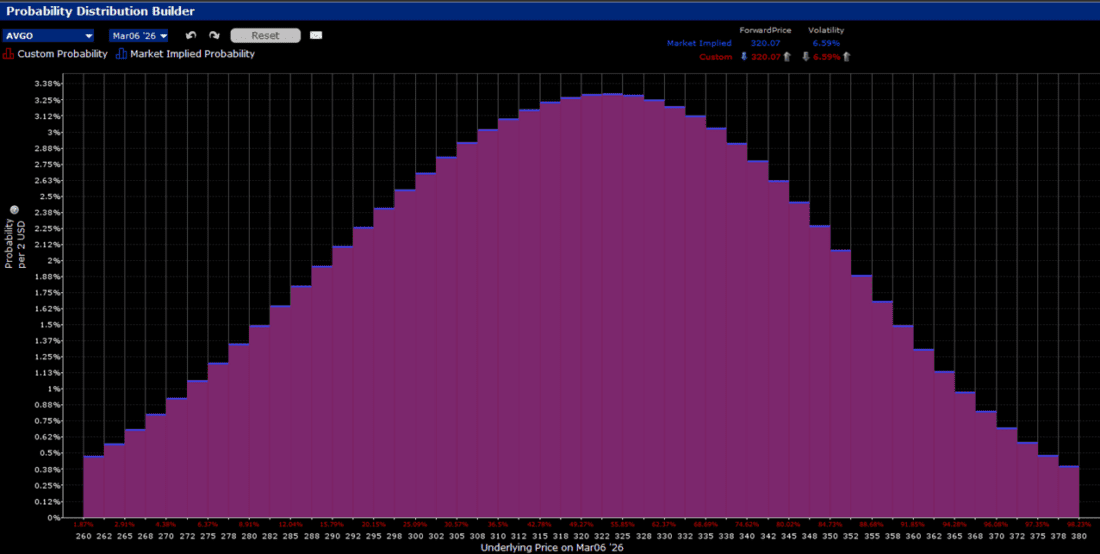

In turn, options traders are pricing in some modest risk aversion. At-money options expiring on Friday are pricing in a roughly 7.8% daily move, which seems substantial, but which is well below the 11.5% average move after the last six quarters’ reports (-11.43%, 9.41%, -5.0%, 8.64%, 24.43%, -10.36%). Despite this, skews show a modest downside bias, though the IBKR Probability Lab is generally symmetrical:

Source: Interactive Brokers

Source: Interactive Brokers

New to Interactive Brokers?

Open AccountAlready an Interactive Brokers Client?

Request Trading PermissionThe analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Options involve risk and are not suitable for all investors. For information on the uses and risks of options, you can obtain a copy of the Options Clearing Corporation risk disclosure document titled Characteristics and Risks of Standardized Options by going to the following link ibkr.com/occ. Multiple leg strategies, including spreads, will incur multiple transaction costs.

The projections or other information generated by the Probability Lab tool regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results and are not guarantees of future results. Please note that results may vary with use of the tool over time.

Related Articles

")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!