- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted March 4, 2026 at 1:04 pm

Animal spirits are making a comeback on Wall Street as developments from Washington and Tehran raise the chances of peace being reached sooner rather than later. The Trump administration sought to quell energy supply nerves as Treasury Secretary Bessent signaled that the US government is ready to step in with a series of measures to protect shipments and ensure that oil is readily available globally. Meanwhile, disputed news that Iran contacted the CIA seeking to end the war was denied by Tehran; however, traders are increasingly believing that the cost of the battle is too elevated to continue, and that sentiment is reflected by crude prices diving to $73.30 per barrel this morning after reaching a 14-month high of $77.98 yesterday. A double beat on the economic calendar alongside well-received retail earnings are also supporting investor optimism, as ADP-jobs and ISM-services surged past expectations, reaching 7- and 41-month highs, which together with robust shopping results, is strengthening confidence that ongoing hiring and buoyant consumer demand will indeed drive an acceleration in growth this year. Yields are flat against the backdrop, as fixed-income observers balance softening commodity costs with momentous activity figures. Meanwhile, stocks and cryptocurrencies are rallying in broad fashion as rebounding market enthusiasm has participants chasing risk assets. Elsewhere, the greenback is sinking slightly while forecast contracts catch bids.

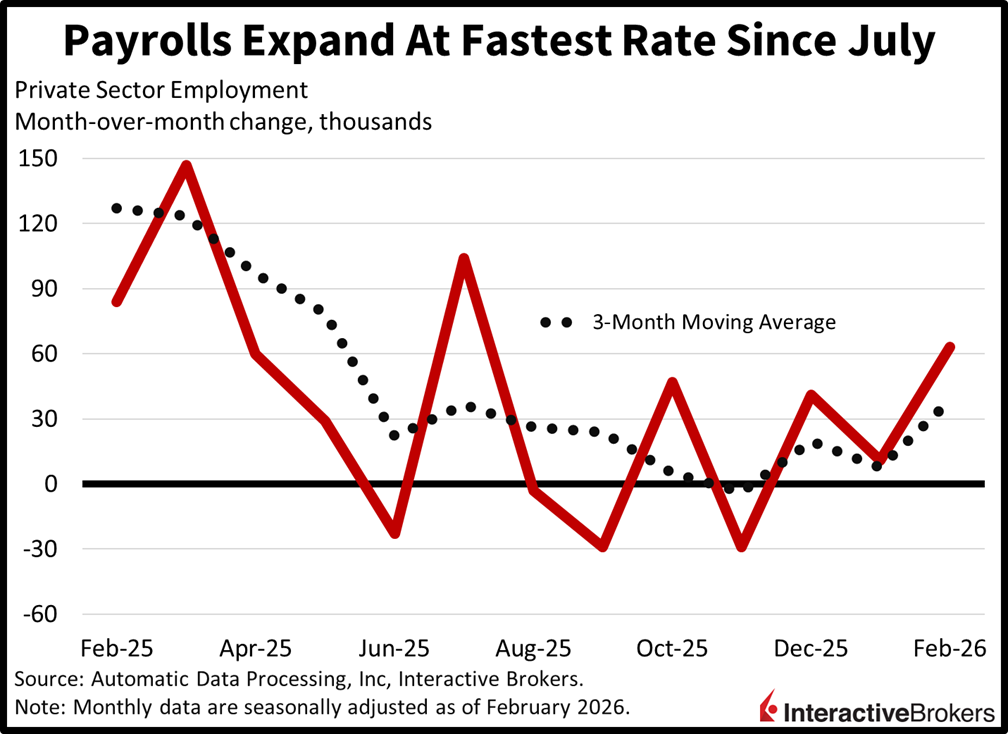

Private sector employers last month hired workers at the fastest pace since July amidst broad expansion throughout industries. The 63k headline number exceeded the expected 50k and January’s 11k as the education/health services, construction and information sectors drove the gains, boosting rosters by 58k, 19k and 11k. Finance, mining, leisure/hospitality and other services also contributed, albeit they all came in under 10k. Conversely, profession/business services, manufacturing and trade/transportation/utilities trimmed payrolls with subtractions of 30k, 5k and 1k. Small and large businesses, meanwhile, added 60k and 10k, but medium-sized firms sustaining between 50 and 499 laborers lost 7k. Compensation trends were relatively steady. The median year-over-year (y/y) changes across job stayers and leavers were 4.5% and 6.3%, respectively, unchanged on the former and lighter than the 6.4% previously reported for the latter.

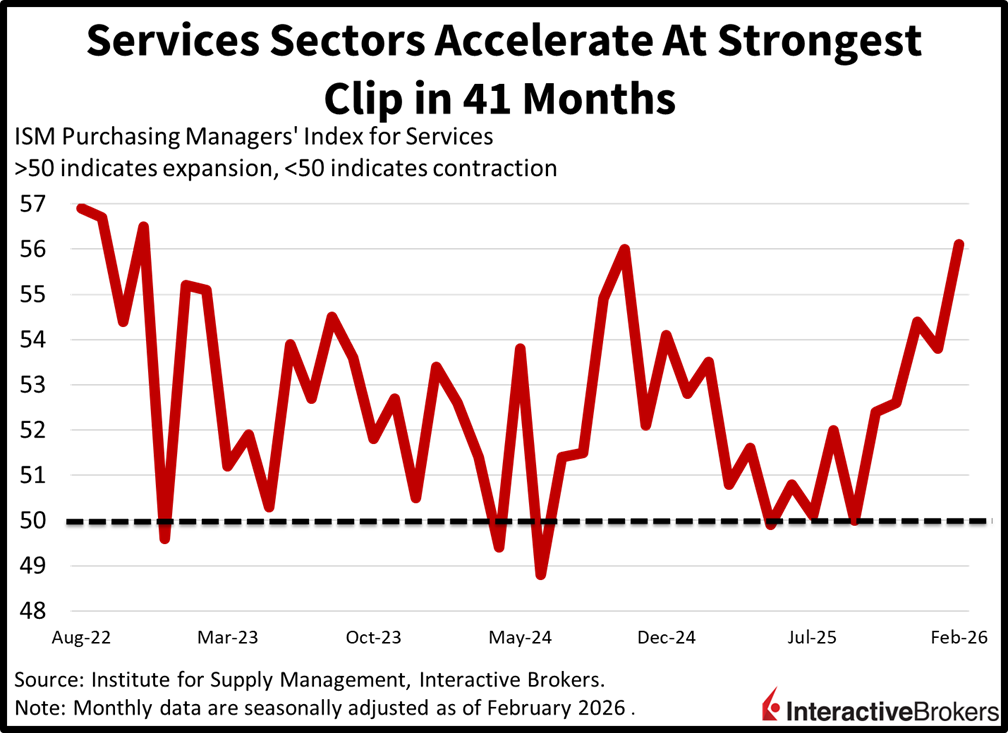

A separate report from the Institute for Supply Management (ISM) confirmed the acceleration in hiring, as roster expansions were supported by buoyant consumer demand. Indeed, the ISM’s Purchasing Managers’ Index for services rose to a 41-month high of 56.1, above the projected 53.5 and January’s 53.8. Business activity, new orders, exports, backlogs and employment all ramped up to scores of 59.9, 58.6, 57.2, 55.9 and 51.8. Price pressures decelerated, meanwhile, from 66.6 to 63.4, but nonetheless remained elevated.

With bouts of volatility followed by intense dip buying in equities this week, the S&P 500 is now flat for March despite the risk of an inflationary episode stemming from the Middle East conflict. President Trump and his cabinet have been active in the media seeking to quell fears regarding a potentially extended war and a shortage of energy supplies, which has driven sharp intrasession rebounds in stocks for three consecutive days. Meanwhile, the GOP is losing ground in the midterm elections, according to the Interactive Brokers prediction market, with odds rising that the Republicans may even give up their majority in the Senate, a potential outcome that had a much lower likelihood at the beginning of the year. The development, while negative for the party in control, is positive for bullish investors, as the Trump put lifts to a higher strike in an attempt to please Wall Street and voters with the dual goal of offsetting both declining approval ratings and weakening probabilities for Republican defeats at the ballots this November.

South Korea’s domestic equity benchmark, the Kospi Index, dropped roughly 12% this morning following Tuesday 7.2% free fall as margin calls intensified a selloff triggered by the Middle East war. The abrupt correction occurred after South Korea stocks climbed more than 50% in recent months with investors clamoring for semiconductor manufactures that are positioned to benefit from billions of dollars being allocated to artificial intelligence. The Middle East violence caused equities to fall worldwide because investors fear that a disruption in oil production and shipping will cause the commodity’s prices to climb and trigger higher inflation. South Korea’s heavy dependence on energy imports has made the Asian peninsula and its manufacturers particularly susceptible to these fears. Additionally, record levels of leverage have intensified the selloff. Investors are now assessing if the South Korean government will intervene.

South Korea’s industrial production in January declined relative to the preceding month, yet it was still substantially stronger than in the year-ago period, according to the Ministry of Data and Statistics. Output as measured by the Index of All Industry Production slipped 1.3% month over month (m/m) but was 4.1% higher than during the year-ago period. Construction was the most significant contributor to the m/m drop while services activity was roughly unchanged. The retail and wholesale sectors also contracted, offsetting encouraging results for software development and computer programming.

Consumers in South Korea dished out 2.3% more at cash registers in January compared to the previous month, according to the Retail Sales Index. In December, spending was up only 0.6% m/m. Despite the m/m ascent, the January volume of transactions was only 0.1% higher than during the first month of 2025.

The China Federation of Logistics & Purchasing and the country’s government this morning published separate reports depicting ongoing economic contraction last month, but a revised S&P report showed that activity in the world’s second-largest economy is expanding at a solid pace. The gauges often produce different results, in part due to variations in the weighting of trade activity.

The official Chinese Composite PMI from the National Bureau of Statistics of China pointed to the country’s economic contraction accelerating with a score of 49.5 after January’s 49.8. A score of 50 is the contraction-expansion threshold.

The Federation’s indices confirmed ongoing weakness with the Manufacturing PMI and Non-Manufacturing PMI at 49 and 49.5. Economists anticipated that the Manufacturing PMI would fall to 49.1 following January’s 49.3 print. For the non-manufacturing sector, the gauge climbed modestly from 49.4 to 49.5 but missed the economist forecast of 49.8.

S&P Global’s RatingDog China reports were more encouraging with the manufacturing version climbing from 50.3 in January to 52.1, the sharpest expansion in more than five years. New orders, including exports, improved considerably. The RatingDog general services PMI depicted a similar pattern with a score of 56.7, a considerable jump from 52.3. It was the fastest expansion in nearly three years.

Australia’s economy expanded across industry sectors resulting in quarter-over-quarter GPD growth of 0.8% during the final three months of 2025. The result exceeded the economist consensus estimate for a 0.7% expansion and it outpaced the 0.5% gain in the third quarter, according to the Australian Bureau of Statistics. On a y/y/ basis, the economy expanded 2.6% following the third quarter’s 2.1% advance. Economists anticipated that the country’s economy would be 2.2% larger relative to the year-ago period. Demand from both private and public sectors picked up with each category contributing 0.3 percentage points to the headline. Companies also rebuilt inventories, providing an additional economic tailwind. Net trade, however, detracted from results with imports increasing at a faster rate than exports.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Trading on margin is only for experienced investors with high risk tolerance. You may lose more than your initial investment. For additional information regarding margin loan rates, see ibkr.com/interest

Interactive Brokers LLC is a CFTC-registered Futures Commission Merchant and a clearing member and affiliate of ForecastEx LLC (“ForecastEx”). ForecastEx is a CFTC-registered Designated Contract Market and Derivatives Clearing Organization. Interactive Brokers LLC provides access to ForecastEx Forecast Contracts for eligible customers. Interactive Brokers LLC does not make recommendations with respect to any products available on its platform, including those offered by ForecastEx.

This is commentary on economic, political and/or market conditions within the meaning of CFTC Regulation 1.71, and is not meant provide sufficient information upon which to base a decision to enter into a derivatives transaction.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. Eligibility to trade in digital asset products may vary based on jurisdiction.

Related Articles

")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!