- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted December 18, 2025 at 12:45 pm

A significant miss in this morning’s CPI featuring the slowest pace of annualized core inflation in almost 6 years is restoring bullish sentiment on Wall Street and raising the chances of the Fed delivering another cut in the first quarter of 2026. A repricing along the curve is occurring as headline and core results arrived in the mid 2s, at 2.7% and 2.6%, figures that are much more conducive to monetary policy easing versus the 3.1% and 3% that were projected. Meanwhile, unemployment claims additionally came in beneath projections, and that’s aiding to curb concerns related to decelerating labor conditions. Stocks and Treasuries are rallying in broad-based fashion in response, with every sector ex energy advancing in equities while yields descend in bull-flattening motion, led south by duration. The balance of softening cost pressures alongside evidence of modest hiring in today’s economic calendar is supporting the greenback, which is gaining despite sinking domestic interest rates. Bitcoin and forecast contracts are also benefiting from risk-on postures following the long-awaited CPI print. The commodity complex is mixed as the cyclical majors gain minus crude oil but a lack of safe-haven demand drive retreats for gold and silver. Similarly, volatility protection instruments are experiencing lessening premiums due to reduced bids for hedges amidst offensive attitudes in markets.

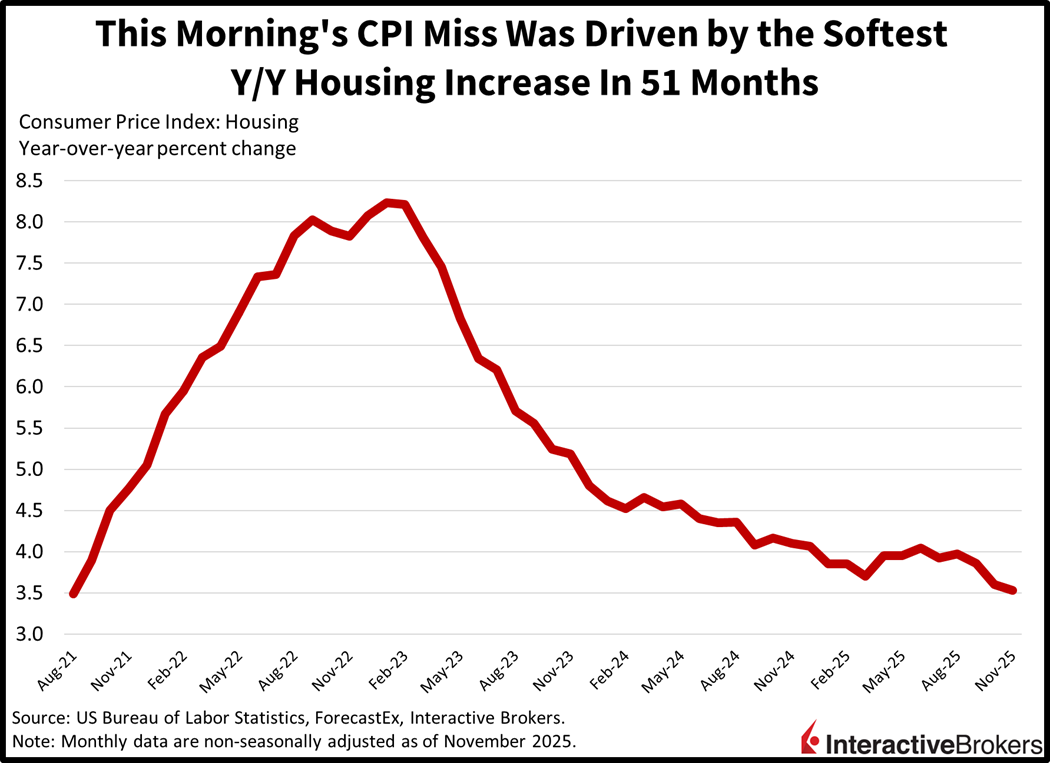

What drove the significant miss in this morning’s inflation report was a sharp deceleration in housing costs, which comprise nearly 45% of the Consumer Price Index (CPI). The pivotal segment retreated to 3.5% year over year (y/y) from 3.9% in September, marking its slowest pace of increase in 51 months, since August 2021. Similarly, transportation services, rose 1.7% y/y, its weakest speed going back to March of 2021, 56 months ago. Meanwhile, food decelerated, with figures for meals at home and at dining establishments shifting to 1.94% and 3.66% from 2.69% and 3.73% y/y. Energy served as a tailwind in the print, but tariff- sensitive areas cushioned that blow. Indeed, durable goods slowed to a hike of 1.5% y/y from 1.8% in September, while non-durables were generally unchanged as a whole.

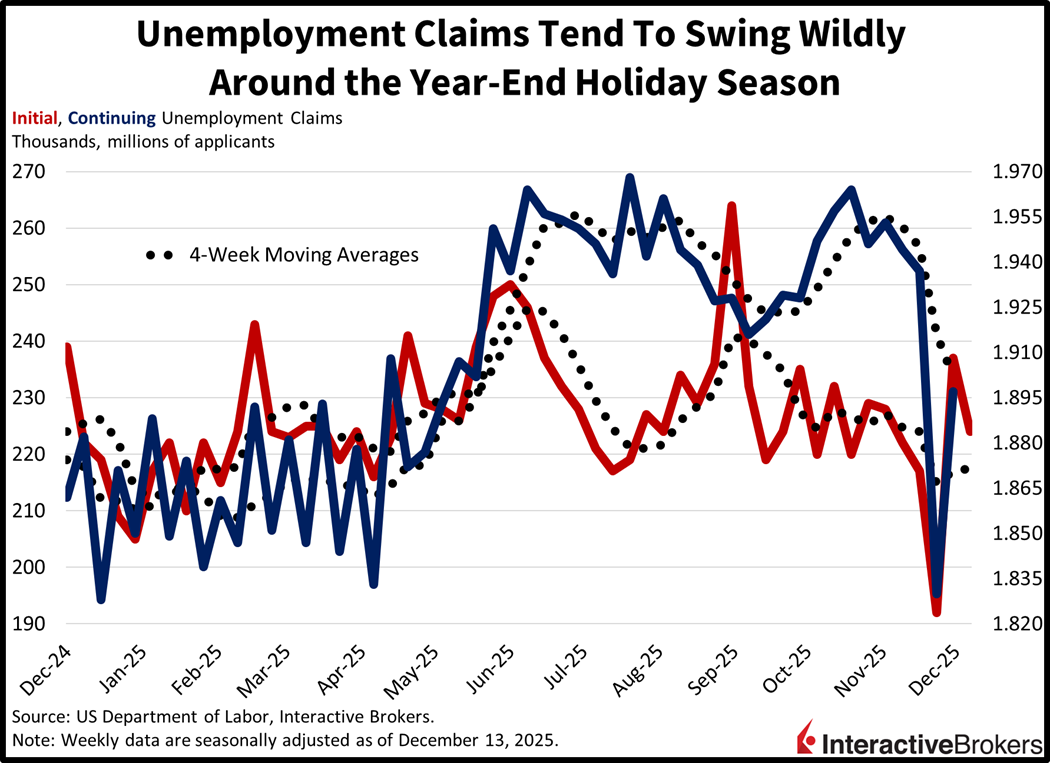

Unemployment claims remained in the safe zone in the past two weeks and are helping to raise confidence as it relates to the strength of the economic cycle. Initial filings dropped to 224k for the week ended December 13, beneath the median estimate of 225k and the 237k released prior. Continuing applications for the 7-day interval culminating on December 6, rose to 1.897 million, below the 1.930 million expected but above the 1.830 million from the previous print. Four-week moving averages went from 217k and1.916 million to 217.5k and 1.902 million.

With the S&P 500 within 1.5% of its record high following this morning’s terrific CPI report, there’s mounting hope of a Santa Claus rally to finish the year above 7,000. Reasons to raise exposures in the final days of 2025 include rising expectations of stimulative assists from the Fed and Congress. Today’s data provide the central bank with a wider path for another series of rate cuts, which alongside the augmentation of its balance sheet and anticipations of an increasingly dovish new Chair in May, serve as significant liquidity and credit tailwinds for risk assets. Meanwhile, President Trump’s signature legislation passed this year is poised to meaningfully boost growth as we turn the calendar. But the Commander in Chief is likely to support markets further via additional bills, in an effort to win over parts of the constituency ahead of the midterm elections, in which the Democrats are expected to flip the House. Finally, robust consumer spending, still healthy labor conditions and buoyant productivity lay the foundation for continued earnings expansion across Corporate America and offers a justification for getting long or staying invested.

Yesterday’s CPI miss of 3.2% y/y in the UK may have been the primary influencer that tilted the votes towards a Bank of England (BoE) cut this morning. Indeed, it was a hawkish reduction amidst a slim majority, with just 5 out of 9 voting members opining in favor of a 25-basis point trim against the backdrop of recession risk and mounting job losses. But the European Central Bank (ECB) decided to pause about an hour later, in light of stable growth, subdued unemployment and inflation that is at 2.1%, right around target.

And in evidence of additional bifurcation across central banks, later today, the Bank of Japan is expected to hike with an elevated degree of certainty in light of persistent cost increases and wage inflation. Conversely, however, the Bank of Mexico (Banxico) is widely projected to trim by a quarter this afternoon due to mounting economic growth worries.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!