- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted April 6, 2026 at 1:15 pm

Stocks are on track to extend their winning streak to 4 consecutive sessions on hopes that Washington and Tehran may secure a 45-day ceasefire. President Trump threatened Iran with harder attacks if the Strait of Hormuz isn’t reopened by tomorrow night’s deadline, but equity participants seem unfazed against the backdrop, as they bought the overnight dip just in time for the commander in chief to potentially quell geopolitical angst during a scheduled afternoon address on this Monday. Furthermore, the word on Wall Street is that the S&P 500 may have bottomed on March 30 at 6317, helping to drive a broad rally to start the week. Conversely, fixed-income investors are increasingly cautious and are pricing out rate cuts, with the yield curve ascending in bear-flattening motion led north by the monetary policy sensitive shorter tenors. Economic data amplified Treasury losses, as ISM-services signaled significant inflationary pressures while slightly missing expectations. Elsewhere, commodities and the greenback are selling off in light of risk-on spirits in markets, which are benefiting cryptocurrency and prediction market activity. Volatility protection instruments are near their flatlines though, as hedges sustain their value ahead of the White House communication.

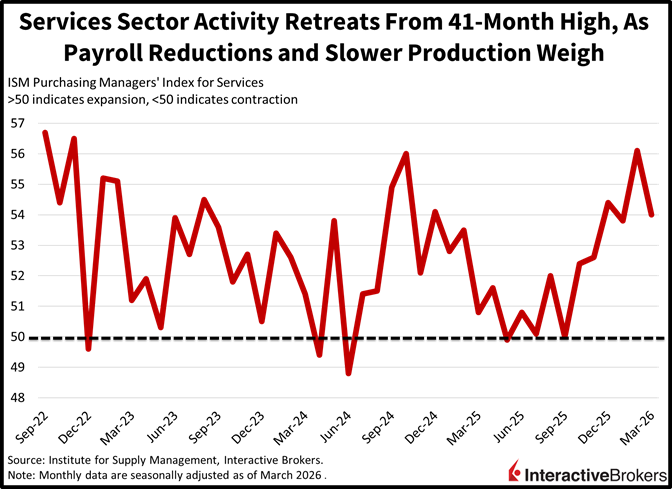

ISM Slows From 41-Month High

Economic activity slowed down in March from a 41-month high according to the services Purchasing Manager’s Index (PMI) from the Institute for Supply Management (ISM). The headline reading of 54 came in below the median estimate of 55 and February’s 56.1, nonetheless, it remained well above the contraction-expansion threshold of 50. Despite the modest miss, customer demand accelerated strongly from 58.6 to 60.6, although robust transaction flows and heavier cost pressures drove the prices segment from 63 to 70.7. Production, backlogs and exports decelerated from 59.9, 55.9 and 57.2 to 53.9, 53.6 and 50.7. The strongest disappointment was the inflationary impulse depicted in the print, however, workforce reduction actions was also a headwind, as the employment category dropped from 51.8 to 45.2.

Wall Street Sniffs Out Potential Deal

With a few hours to go until President Trump’s deadline tomorrow night, Washington and Tehran remain far apart on an agreement. However, Wall Street is sniffing out a potential ceasefire deal that drives a significant rally in stocks, as there’s mounting political pressure domestically for gasoline costs to normalize and asset price volatility to subside in this midterm election year. But the Iranians don’t appear positioned to acquiesce to White House demands just yet and have been instead looking for a definitive end to the war, a lifting of sanctions and funds to support the rebuilding of damaged infrastructure. Against this tense backdrop, market moves are poised to be increasingly binary, with gains from here likely stemming from peace in the Middle East, while continued violence and heightened uncertainty is conducive to ongoing bumpiness in equity and fixed-income portfolios alike.

International Roundup

Singapore Reports Mixed Consumption

Singapore retail sales contracted 4.1% on a month over month (m/m) basis but expanded 8.3% year over year (y/y) in February, after reporting figures of 6% m/m and -0.5% y/y in January. Monthly results featured increases in just 5 of 13 categories, as the other, recreational goods, computer/telecommunications, furniture and cosmetics segments rose 24.5%, 6.7%, 5.5%, 3.5% and 0.5%. Clothing, jewelry, and mini-market/convenience stores served as the strongest headwinds, retreating 14.4%, 13.9% and 13.8% m/m during the period.

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. Eligibility to trade in digital asset products may vary based on jurisdiction.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!