- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted December 16, 2025 at 1:08 pm

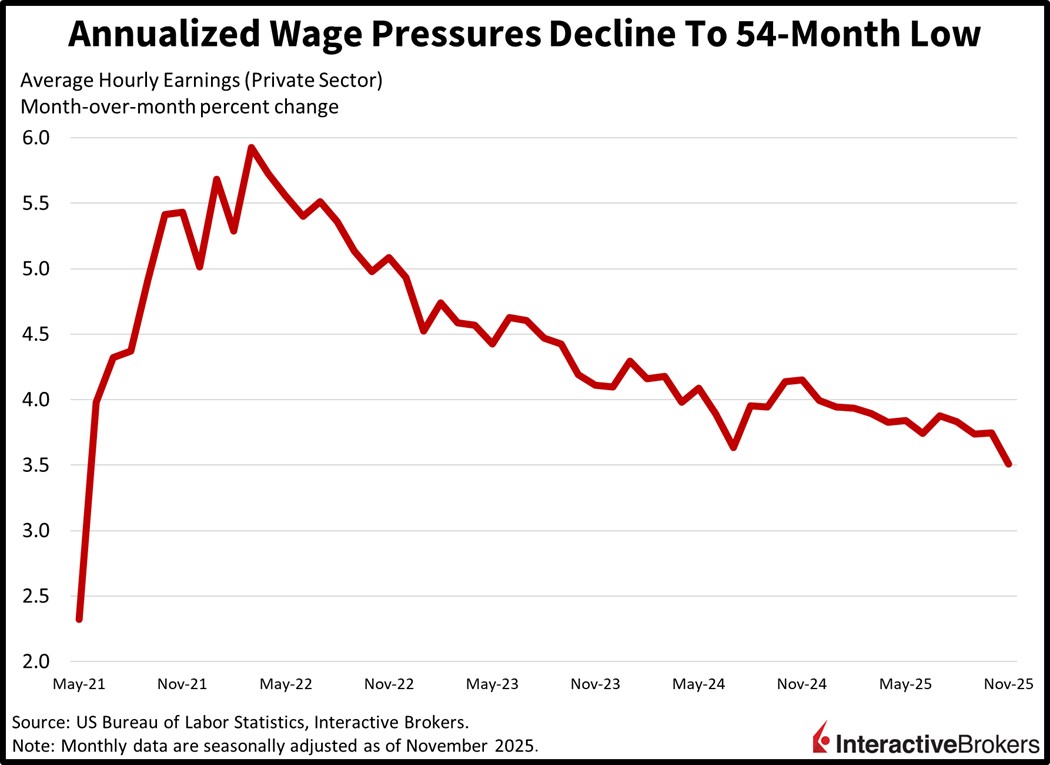

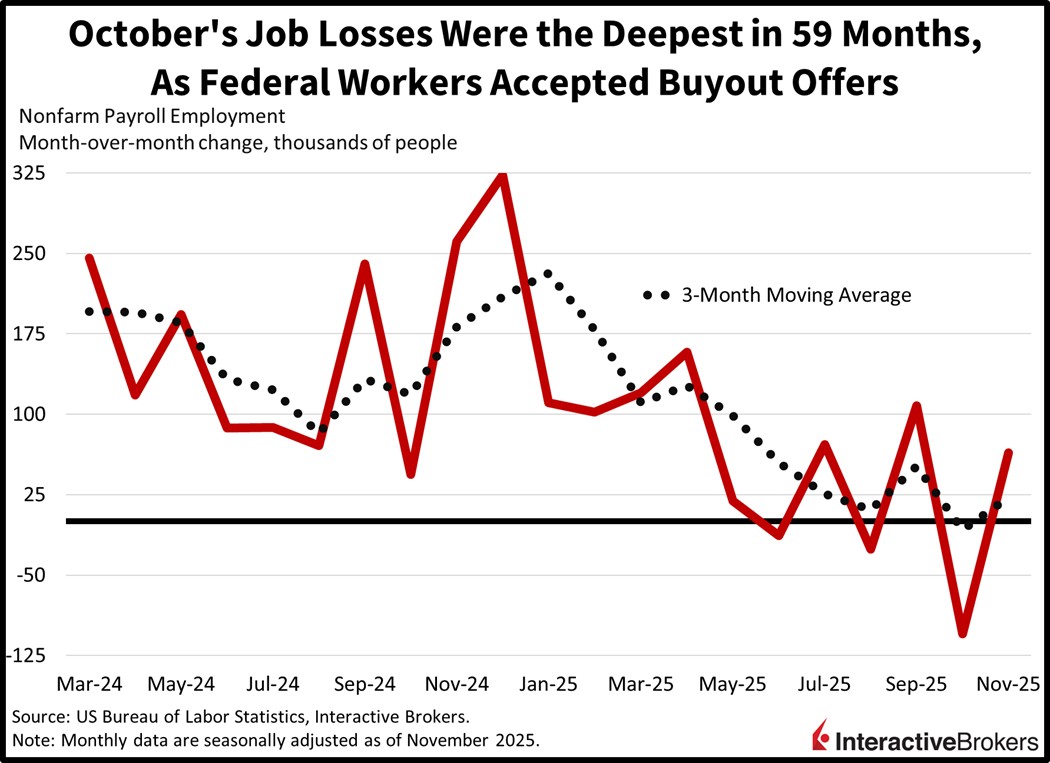

An unexpected jump in the unemployment rate to levels not seen since 2021 is generating slowdown angst across Wall Street, as investors dial down equity exposures and scoop up Treasuries with a short-end bias. The 50-month high in joblessness dampened the pre-market enthusiasm that existed prior to the nonfarm payrolls release. Meanwhile, optimism about a modest 64k November job beat was offset by a sharp 105k decline in October, which was detailed in the same print due to adjustments made as a result of the longest government shutdown in history. Federal employees who accepted the White House’s buyout offer deepened the roster reductions in the former month, which was the weakest in 59. More evidence of a deceleration came from paycheck growth, which slowed to the softest pace in 54 months and is compressing its spread versus the 3% inflation rate, adding risks to the outlook for consumer spending, as shoppers have enjoyed meaningful real wage expansions for an extended period. Thankfully, retail sales ex autos and gasoline were firm, as were flash PMIs and ADP’s weekly hiring indicator. These reports signaled strength amongst household outlays, corporate revenues and appetites for additional workers, serving to counter the sluggish BLS publication while tempering Fed easing expectations. The mix of developments sent the yield curve and the greenback modestly lower, because a sole focus on the main employment situation report would have likely generated a plunge in borrowing costs and the US dollar. Equities are attempting a comeback, however, with the Nasdaq 100 benchmark now at its flatline after all 11 major sectors were retreating on the session; only 9 are at the moment. Bitcoin and forecast contracts have been catching bids all morning but commodities ex-gold are descending.

ADP reported that in the previous 28 days, the average amount of workers added to private sector rosters totaled 16.25k per week, well above the 2.75k published during the prior interval last Tuesday.

Retail sales were flat in October with declines in energy prices and automobile transactions hampering results. But when excluding those items, building materials and food services, the resulting control group, which is a significant input to the gross domestic product calculation, rose a sharp 0.8% month over month (m/m), well above the 0.4% median forecast and the 0.1% decrease from September. Among the 13 categories, the following eight experienced strong progress:

Those gains were countered by slipping cash register activity among businesses tied to car dealerships, building materials, gasoline stations, health/personal retailers and restaurants/bars.

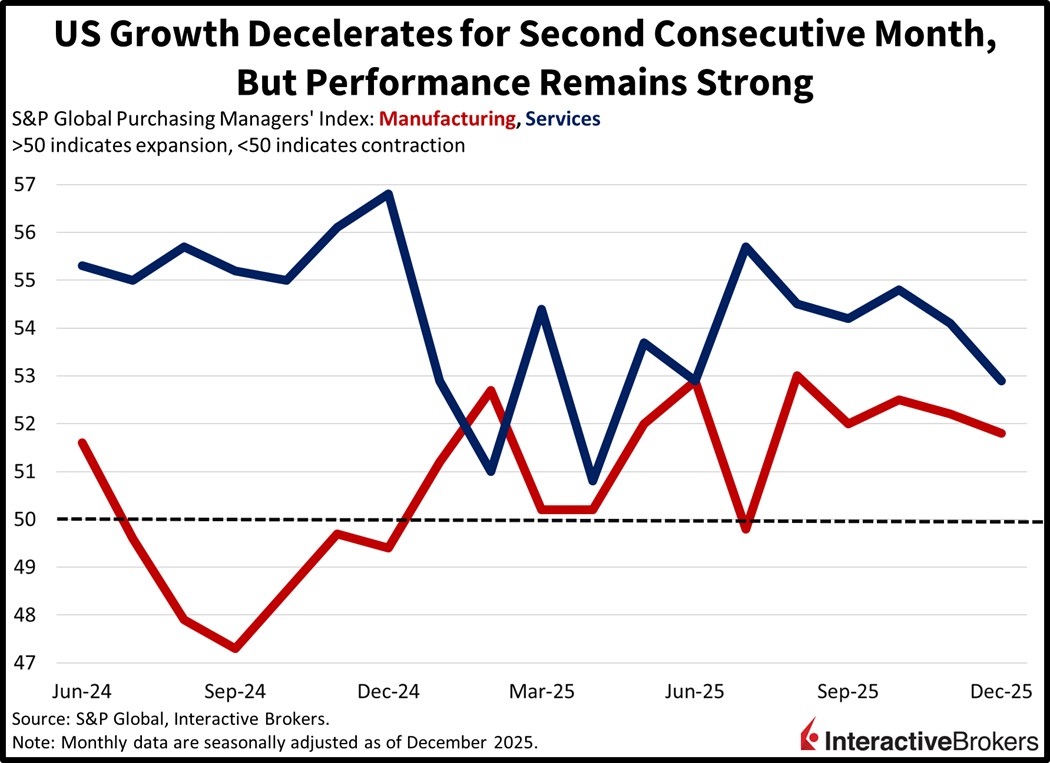

December’s S&P Global Flash Purchasing Managers’ Indices (PMI) depicted marginally slower growth this month relative to November and October. The services and manufacturing headlines of 52.9 and 51.8 missed projections of 54 and 52 and were beneath November’s 54.1 and 52.2. The declines were driven by softening demand and weaker confidence amongst survey respondents, which were influenced by a sharp increase in tariff-related costs. Still, the numbers were relatively strong across the board, but the second-consecutive period of deceleration is certainly something to watch.

Restrictive immigration policies paired with AI adoption are curbing the upside potential for nonfarm payrolls and clouding the traditional relationship between job losses and economic expectations. On the one hand, aggregate worker supply is inadequate for significant roster additions, while on the other, modern technologies are motivating companies to raise productivity levels with reduced headcounts. Meanwhile, the conventional trend of higher unemployment generating cyclical turbulence is significantly different these days in light of aging demographics, and an economy that’s less labor intensive but increasingly dependent on stock market values. Wall Street is waking up to the fact that lackluster employment gains aren’t terrible against this backdrop since they haven’t’ resulted in consumer spending weakness and growth has held up despite softening headline results.

Japan’s business activity is continuing to expand but at a slightly slower pace than in November with this month’s S&P Global Flash Composite PMI Index falling from 52 to 51.5 but remaining above the contraction-expansion threshold of 50. The services version of the PMI weakened from 53.2 to 52.5, while the manufacturing gauge strengthened from 48.7 to 49.7 and exceeded the economist consensus estimate of 49.

Within the composite gauge, new orders for good declined due to waning foreign demand, but services orders from overseas improved marginally. In other areas, overall employment increased across both sectors at the fastest pace since May 2024. Input costs also increased, but businesses were able to raise what they charge customers. Services companies, furthermore, experienced growing order backlogs and unfinished work for manufacturers sank at the slowest pace in 18 months. Firms were optimistic about growing output due to client demand, new product releases and expansions into new markets but they remained concerned about global trade uncertainty and an aging population.

Payrolls in the UK shrank by 38k and 171k positions m/m and year over year (y/y) in November, according to an early estimate from the Office for National Statistics. Also last month, 20.1k individuals claimed unemployment benefits, slightly below the 21.6k economist consensus estimate but a significant reversal from October’s 3.9k decline. October data also pointed to weakening labor conditions. As expected, the unemployment rate climbed from 5% in September to 5.1%. Additionally, average y/y earnings increases ex bonus and with bonus slowed from 4.7% and 4.9% to 4.6% and 4.7%. The results outpaced the estimates for compensation to ascend 4.5% and 4.4%.

Business activity expanded at a faster pace this month than during November with the S&P Global Flash UK PMI Composite Output Index climbing from 51.2 to 52.1 Both services and manufacturing picked up with the former category improving from 51.3 to 52.1 while the latter sector went from 50.2 to 51.2. The growth of goods production, furthermore, sped up with the metric improving from 50.2 to 51.2. Broadly speaking, the strongest jump in new orders in 14 months helped push the PMI prints higher. The gain included loftier order volumes from foreign customers. Demand contributed to order backlogs growing for time since February 2023. Conversely, input costs and charges to customers moved north at the most aggressive rates since May and August, respectively. Survey respondents attributed the cost pressures to wage inflation, higher fuel bills and rising technology expenditures. The data implies that labor market weakness is continuing with firms reporting declines in staffing, a reaction to intense cost pressures and elevated business uncertainty.

The eurozone continued to experience business activity growth this month but at a slower pace. The S&P Global Flash Composite Index fell from 52.8 to 51.9, a three-month low and below the economist consensus estimate of 52.7. Manufacturing output was the most concerning with its gauge slipping from 50.4 to 49.7, a 10-month low. Economists anticipated a 49.9 result. The broader manufacturing PMI, meanwhile, remained in contraction with its score falling from 49.6 to 49.2. The services component also contributed to the slowdown with its index weakening from 53.6 to 52.6.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. Eligibility to trade in digital asset products may vary based on jurisdiction.

Forecast Contracts are only available to eligible clients of Interactive Brokers LLC, Interactive Brokers Canada Inc., Interactive Brokers Hong Kong Limited, Interactive Brokers Ireland Limited and Interactive Brokers Singapore Pte. Ltd. Forecast Contracts on US election results are only available to eligible US residents.

Futures, event contracts and forecast contracts are not suitable for all investors. Before trading these products, please read the CFTC Risk Disclosure. For a copy visit our Warnings and Disclosures Page.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!