- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted November 25, 2025 at 10:30 am

NVIDIA has just delivered another blockbuster earnings report: revenue at record highs, margins still exceptional, and cash generation that would make most Fortune 500 companies jealous. And yet, despite beating expectations, the stock dropped sharply.

Why?

In this article, we dive into the underlying risks hidden behind the headline numbers — risks that many investors are comparing to the late-1990s Cisco playbook.

This is the natural continuation of my earlier analysis, “Investing Through the AI Bubble: Lessons From Jeff Bezos’ Prophecy”, published here on Interactive Brokers.

Markets initially celebrated the earnings release: NVIDIA proved once again that it is the undisputed leader of the AI-infrastructure boom. But by mid-day trading, the stock reversed violently, erasing more than $400 billion in market cap — one of the largest intraday swings in history.

Why such a dramatic reaction?

Because investors began to dig into the details behind the numbers, discovering signs of stress that echo the late stages of previous tech supercycles: heavy customer concentration, rising working-capital risks, and cracks in the demand narrative.

To understand today’s fears, we must revisit the past.

During the dot-com boom, Cisco sold the “shovels” of the Internet gold rush — routers, switches, and the infrastructure powering the new online economy. At its peak, Cisco was the most valuable company on Earth.

But just before the bubble burst, two metrics quietly began flashing red:

Both suggested that customers were ordering aggressively… but not paying quickly. And that Cisco was shipping more equipment than the market could truly absorb.

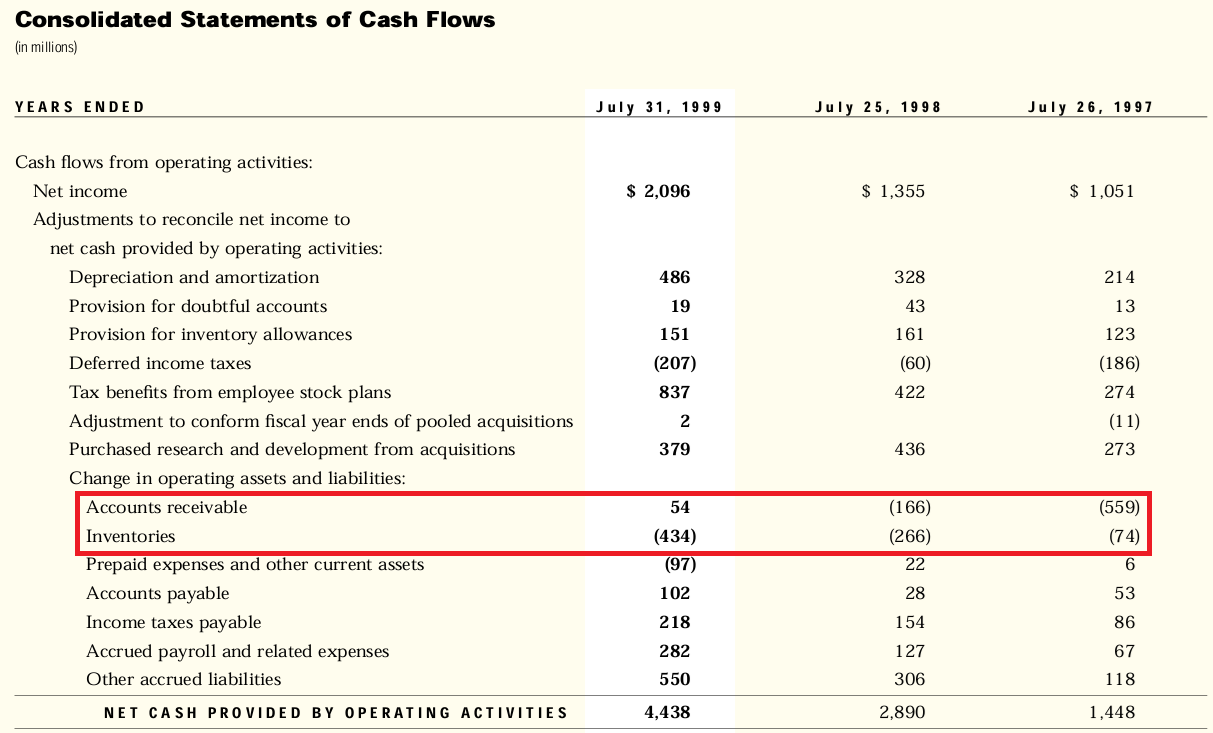

Cisco’s 1999 cash-flow statement showing a sharp rise in accounts receivable and inventories—two early warning signs that demand was softening beneath the surface. These same balance-sheet red flags are now appearing in NVIDIA’s latest results, raising investor concerns about the sustainability of the current AI-infrastructure boom. Source: Cisco System Investor Realtions

When the Internet bubble deflated, those early warning signs transformed into a collapse in demand — and Cisco’s stock never revisited its all-time highs for more than two decades.

In my previous IBKR analysis, I explored how Jeff Bezos himself compared today’s AI boom to the dot-com buildout. NVIDIA, like Cisco once, is selling the essential picks and shovels of a new technological wave.

This does not mean the bubble will burst — but it explains why the market is hypersensitive to Cisco-like signals.

The Two Red Flags: Inventories and Accounts Receivable

Now let’s bring the lens back to NVIDIA.

In the latest earnings report, despite its exceptional revenue, two working-capital metrics raised eyebrows:

Accounts receivable represent chips sold but not yet paid for.

And they have increased dramatically quarter after quarter.

This can have many explanations — long installation times, cloud providers staging multi-quarter buildouts, or simply standard enterprise payment cycles.

But historically, rapid increases in A/R often precede cooling demand.

Inventories are also rising, suggesting either:

No one is accusing NVIDIA of wrongdoing — but investors cannot ignore how similar this pattern looks to Cisco in 1999.

NVIDIA’s latest cash-flow data shows a sharp rise in accounts receivable and a notable build-up in inventories — the same two warning indicators that preceded Cisco’s slowdown in 1999. Despite record revenue, these working-capital pressures suggest that AI-infrastructure demand may be stretching customers’ ability to absorb and pay for new GPUs. Source: Forecaster Terminal Nvidia Fundamentals page

In both cases, Cisco then, NVIDIA now, top-line growth masked subtle balance-sheet pressure.

Customer Concentration: 61% of Revenue From Just Four Buyers

Another datapoint amplified market fears:

61% of NVIDIA’s total revenue now comes from only four customers.

The company does not disclose their names, but industry observers widely believe they are the hyperscalers:

(or possibly Oracle replacing one of the above)

This concentration adds systemic risk.

If even one of these giants slows its AI spending cycle, NVIDIA’s growth curve could flatten abruptly.

And in a recent public appearance, Elon Musk casually threw around datacenter capex figures in the hundreds of billions — numbers so extreme that Jensen Huang himself seemed uncomfortable.

Investors took note. When numbers get too big, too fast, skepticism enters the room.

The Hyperscaler Shift: From Cash Purchases to Debt-Financed GPU Buying

One of the most overlooked datapoints in the entire earnings discussion:

The major AI infrastructure buyers (Alphabet, Amazon, Meta, Microsoft, Oracle) have stopped using free cash flow to fund GPU purchases.

They are now issuing debt to finance their AI infrastructure buildouts.

This adds leverage — and therefore risk — to the entire ecosystem.

If rates stay higher for longer…

If monetization of AI lags expectations…

If political or regulatory pressure increases…

…a pullback in capex could arrive quickly.

And with 61% of revenue tied to only a handful of companies, NVIDIA becomes vulnerable to a synchronized slowdown.

The Growing Competitive Threat: Google’s TPU Breakthrough

Another catalyst spooking investors came from outside NVIDIA:

Google’s newly announced Gemini 3 Pro was trained entirely on Google’s in-house TPUs, not on NVIDIA GPUs.

The implication?

Even NVIDIA’s largest customers are actively building pathways to reduce their future dependence on NVIDIA’s high-margin chips.

This doesn’t kill demand today.

But it reduces confidence in the duration of the current supercycle.

Final Thoughts: Great Company, Fragile Ecosystem

NVIDIA remains one of the most profitable companies in history. Nothing in the data suggests a collapse in the near term. The AI build-out is real, necessary, and global.

But the balance sheet tells us that the easy phase of the AI boom is behind us.

The next phase will require:

Until that happens, NVIDIA will continue to trade like the center of a high-beta ecosystem — brilliant, dominant, but vulnerable to every tremor around it.

—

Originally Posted November 24, 2025

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Forecaster.biz and is being posted with its permission. The views expressed in this material are solely those of the author and/or Forecaster.biz and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

You don’t seem to understand this space, technology or Nvidia. This is nothing like Cisco. Take a better look at Nvidias solutions. Their eco system is more than plumbing. Consider GPU, CPU, ASIC and NV Link capabilities. To start with.