- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted October 13, 2025 at 10:30 am

Earnings season kicks into high gear this week, with the big banks unofficially firing the starting gun on Tuesday. As the season begins, major U.S. indices are at record levels, even amidst a government shutdown, creating a dynamic environment with no shortage of significant events.

Sell-side analysts and investors alike are optimistic heading into the reports. For the first time since late 2021, Wall Street analysts have actually raised their earnings estimates heading into the reporting period, a rare vote of confidence in corporate America. The consensus is for an impressive 8% year-over-year earnings growth for the S&P 500®, a figure that would mark the ninth straight quarter of expansion. Revenue growth is expected at 6.3%.1

But don’t let the headline number fool you. Under the surface, a “have and have-not” economy is becoming more entrenched. While the AI darlings and financial giants are poised for a strong showing, other sectors are starting to feel the pinch of a more discerning consumer and persistent inflation.

Big Banks Poised for Another Strong Showing

Financials are expected to be one of the leading sectors this season, as the environment for banks has gotten better, but there are still headwinds. JPMorgan Chase, Citigroup and Wells Fargo get the party started on Tuesday and here’s what we’re looking for updates in three key areas:

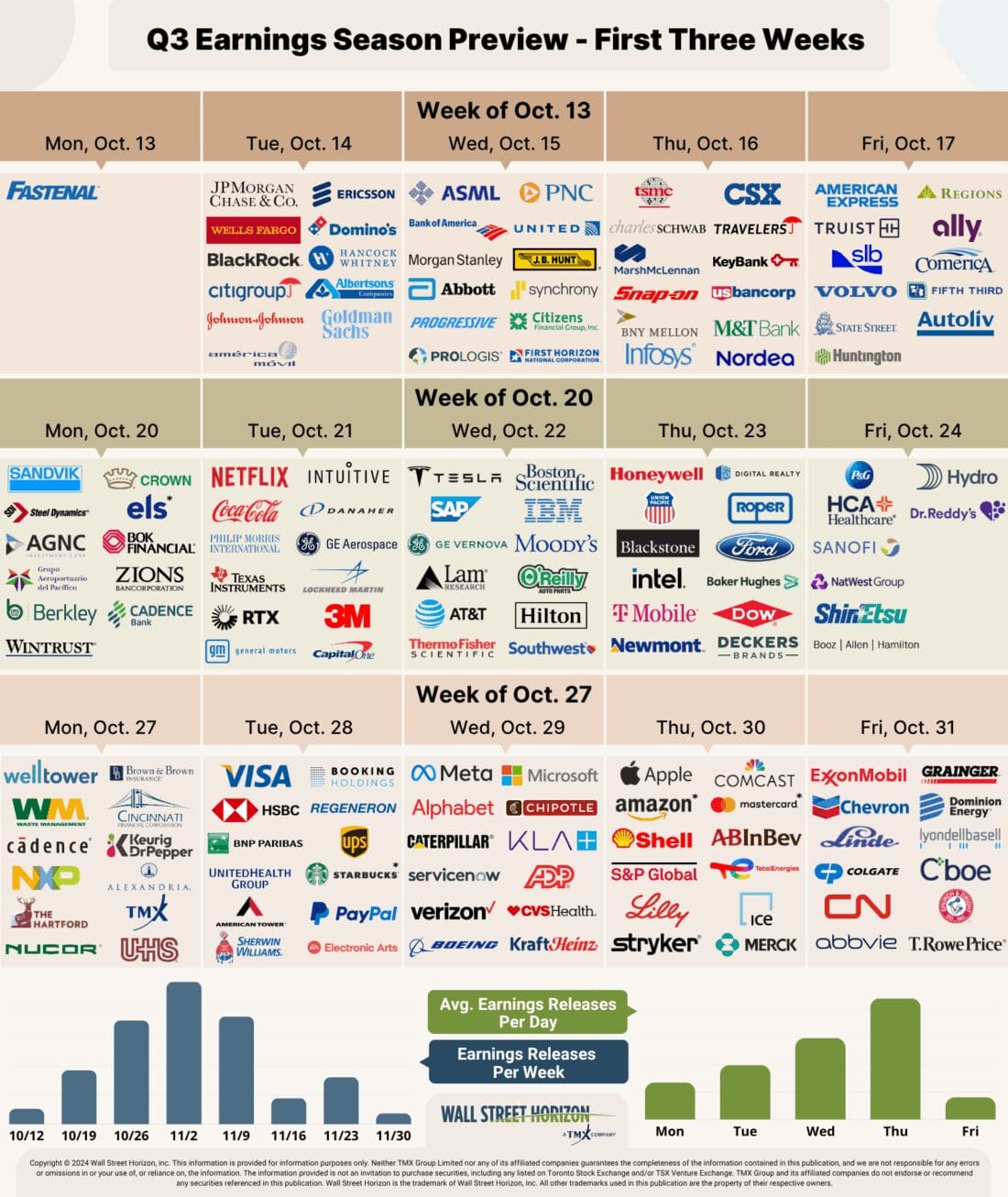

Source: Wall Street Horizon. Companies market with an * are unconfirmed. Data as of October 9, 2025.

The AI Arms Race Continues

The tech sector, and particularly the Mag7, is once again expected to do the heavy lifting this quarter. If you need any evidence of that just look at the number of multi-billion dollar AI partnerships and deals announced in only the last few weeks.4

Companies that provide the picks and shovels for the AI gold rush are set to report another round of stellar numbers. According to FactSet, earnings growth for S&P 500 tech names is expected to top 20.9%.5 Look for companies like Nvidia (NVDA) and other semiconductor players to continue their impressive growth trajectory. The enterprise software space is also one to watch, as companies are pouring money into AI-powered solutions to boost efficiency. To put it bluntly, if you don’t have an AI story to tell this quarter, you’d better have a reason. AI is so important to the US economy right now, that AI corporate spending makes up around 40% of US GDP growth this year.6

A Bifurcated Consumer

While the tech boom has been a boon for some, there are growing concerns about the lower-end consumer. We’ll be keeping a close eye on reports from big-box retailers and consumer staples companies for clues on the health of Main Street, most of which report in a month’s time. Expect to hear a lot about “value-conscious” shoppers and the ongoing battle for market share between legacy brands and private-label alternatives. The consumer staples (expected EPS decline of -3.1%) and consumer discretionary (expected EPS decline of -1.7%) sectors are expected to be laggards this quarter, a sign that the post-pandemic spending splurge may be running out of steam.7

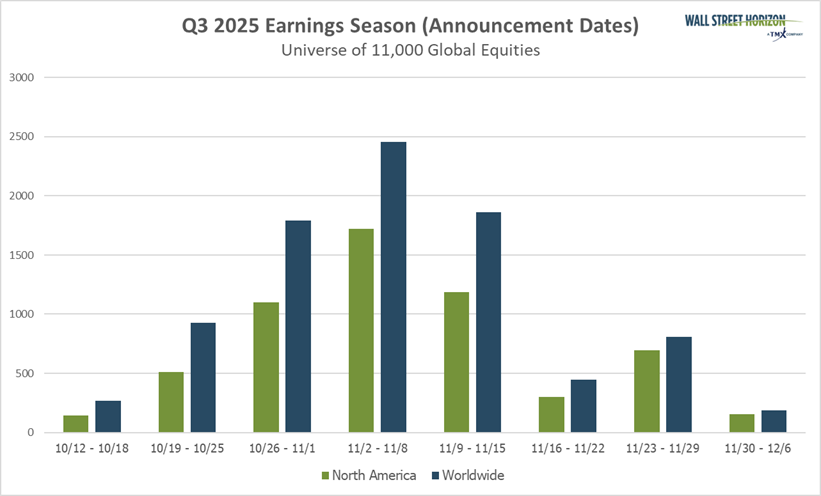

The peak weeks of the Q3 earnings season are expected to fall between October 27 – November 14, with each week expected to see over 2,000 reports. Currently, November 7 is predicted to be the most active day with 1,238 companies anticipated to report. Thus far, only 48% of companies have confirmed their earnings date (out of our universe of 11,000+ global names), so this is subject to change. The remaining dates are estimated based on historical reporting data.

Source: Wall Street Horizon

This earnings season is shaping up to be a tale of two markets. While the tech sector is likely to continue its impressive run, the real test will be whether the rest of the market can keep pace. The unusual optimism from Wall Street analysts is a good sign, but it also sets a high bar for companies to clear. Any disappointments could be met with a swift and punishing response from investors.

—

Originally Posted October 13, 2025 – Q3 2025 Earnings Preview: Earnings Season Begins with High Hopes and Key Tests for Banks

1 FactSet Earnings Insight, John Butters, October 10, 2025, https://advantage.factset.com

2 “For global M&A, third quarter was one of the best – and worst – in recent history,” Reuters, Dawn Kopecki, Charlie Conchie and Kane Wu, October 1, 2025, https://www.reuters.com

3 “Aggregate loan growth at US banks shoots to a 3-year high in Q2 2025,” S&P Global, Robert Clark, August 18, 2025, https://www.spglobal.com

4 “From OpenAI to Meta, firms channel billions into AI infrastructure as demand booms,” Reuters, October 6, 2025, https://www.reuters.com

5 FactSet Earnings Insight, John Butters, October 10, 2025, https://advantage.factset.com

6 “How AI became our personal assistant,” Financial Times, Dan Clark and Caroline Nevitt, October 7, 2025, https://ig.ft.com

7 FactSet Earnings Insight, John Butters, October 10, 2025, https://advantage.factset.com

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Wall Street Horizon and is being posted with its permission. The views expressed in this material are solely those of the author and/or Wall Street Horizon and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

Any discussion or mention of an ETF is not to be construed as recommendation, promotion or solicitation. All investors should review and consider associated investment risks, charges and expenses of the investment company or fund prior to investing. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

There is a substantial risk of loss in foreign exchange trading. The settlement date of foreign exchange trades can vary due to time zone differences and bank holidays. When trading across foreign exchange markets, this may necessitate borrowing funds to settle foreign exchange trades. The interest rate on borrowed funds must be considered when computing the cost of trades across multiple markets.

Security futures involve a high degree of risk and are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading security futures, please read the Security Futures Risk Disclosure Statement. For a copy visit ibkr.com

Spot currencies are not available at IBKR Singapore.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!