- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted September 10, 2025 at 12:54 pm

Wall Street is rallying and stocks have hit fresh records as a much weaker-than-anticipated PPI depicted deflation rather than expected inflation. Animal spirits are soaring because the well-received print is bolstering probabilities that the Fed will deliver cuts during each of its last three meetings of 2025. Meanwhile, odds for a jumbo 50 reduction next week only increased marginally, although those chances could rise meaningfully if we get a miss on tomorrow’s more significant CPI release. Investors are also enthusiastic following Oracle providing a blockbuster outlook for future revenues associated with artificial intelligence, which is propelling confidence that the tech-fueled bull market has further to run. Equities are advancing amidst a majority of sectors gaining while Treasuries climb. The yield curve is descending in bull-steepening fashion led by the shorter-tenors, driven by monetary policy accommodation prospects. But duration could narrow the gap this afternoon if there’s a packed house bidding at a $39 billion government auction for 10-year notes. The commodity complex ex natural gas and lumber is additionally experiencing higher prices alongside strong interest for bitcoin and forecast contracts. Conversely, volatility protection instruments and the greenback are facing selling pressure on softer hedging demand and lighter domestic borrowing costs.

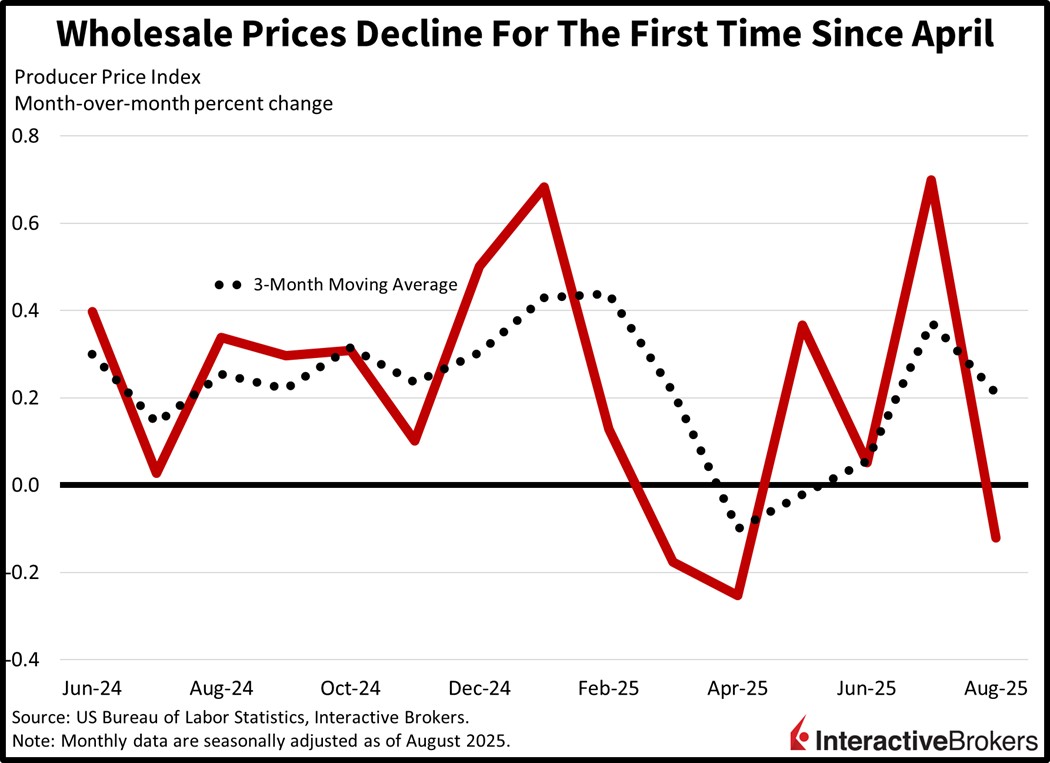

Wholesale prices retreated last month for the first time since April as deflation in services and energy drove the headline Producer Price Index (PPI) into negative territory. The 0.1% month over month (m/m) August decline missed the median estimate of a positive 0.3% by a wide margin and was well below the 0.7% increase in July. Similarly, the 2.6% year over year (y/y) gain arrived beneath the 3.3% expectation and the prior month’s 3.1%. Overall services saw a 0.2% m/m decrease, as the trade category dropped 1.7% which countered the 0.9% and 0.3% increases in the transportation/warehousing and other components. Goods as a whole experienced m/m inflation of 0.1%, with core products rising 0.3%, food up 0.1% and energy down 0.4%.

In a similar manner to my commentary yesterday that maintained expectations for today’s PPI were too high, I believe the outlook for tomorrow’s Consumer Price Index (CPI) print is excessively elevated. Indeed, subdued energy costs, sluggish housing valuations, low rents and a lack of tariff-fueled cost pressures are like to dampen the gauge’s increase.

My estimate for this week’s CPI is 2.8%, below the median of 2.9%; however, a significant 2.7% surprise would mark a flat annualized reading for the third consecutive month. A miss of that magnitude would spark chants calling for the Fed to slash by 50, rather than the traditional 25 next week. Odds of a super-sized half-point cut are currently at just 10%, but a 2.7% figure would raise those chances to a coin-flip, in my opinion. A downside shocker would create a trio of developments this week that contained a heavy payroll benchmark revision and the softer-than-projected PPI, which would justify a larger reduction by the Fed. This bullish hypothetical would drive stocks to another new record and plunge the yield curve south, with the 2 and 10 tenors dropping beneath the pivotal levels of 3.50% and 4%. On the contrary, a fresh burst of services inflation driven by corporate pricing power resulting from robust shopper demand would generate a bearish move in markets amidst unfavorable seasonals, featuring lower equities and loftier interest rates.

International Roundup

August retail prices in China were unchanged m/m but down more than expected relative to the same month of 2024 while wholesale prices fell nearly 3% during the same 12-month period. The results are expected to intensify pressure on the country’s government to provide additional economic stimulus. The Consumer Price Index was flat relative to July after climbing 0.4% in m/m in July and it missed the economist consensus estimate for a 0.1% increase. When compared to August 2024, the index was down 0.4%, which was worse than the economist consensus forecast for a 0.2% drop and July’s goose egg result. Meanwhile, wholesale prices, as measured by the PPI, descended 2.9% in August, matching the consensus estimate and easing from the 3.6% y/y drop in July. Beijing officials maintain that the August y/y CPI result reflect a high level in the year ago period. Additionally, food prices declined slightly. Regarding the PPI, the drop was driven, in large part, by the country cracking down on price competition.

Japan manufacturers’ confidence strengthened this month to its high level in more than three years as depicted by the Reuters Tankan survey climbing from +9 in August to +13. It was the third consecutive monthly increase and led by the auto and transport machinery sector hitting +33. In that category, firms reported weak domestic production but said they are experiencing steady orders from foreign customers. Other manufacturing segments, including oil refining, precision machinery and textiles, experienced declining sentiment, a result of tariffs causing a decline in orders from other countries. The non-manufacturing gauge was also strong, climbing from +24 in August to +27. While wholesalers and tech companies reported weakening conditions, sentiment within the real estate, retail and transport moving sectors strengthened.

South Korea’s unemployment rate climbed from 2.5% in July to 2.6% last month, according to Statistics Korea.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

Despite seasonal headwinds and weakening economic data, markets are holding up pretty well.