- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted September 9, 2025 at 12:55 pm

Treasuries are taking a break from their relentless rally after this morning’s benchmark revision to nonfarm payrolls failed to subtract a million workers or more from total rosters. The record reduction of 911,000 employees was significant, but not enough to bolster the single-digit odds of a 50 basis-point cut from the Fed next week, which is driving rates north. Stock indices are mostly near their flatlines though, as Wall Street awaits pivotal PPI and CPI inflation reports in the next two days that are certainly going to increase visibility related to the pace and rhythm of the central bank’s walk down the monetary policy stairs. A quiet economic calendar did feature NFIB small business optimism rising for the second consecutive month in August, but that couldn’t move the needle from a capital markets perspective. It definitely didn’t contain the retreat in the Russell 2000, however, as small caps are suffering the heaviest losses across benchmarks, as those investors would’ve benefited the most from a faster stride south to cheaper borrowing costs. Indeed, yields are climbing in bear-flattening fashion led by the short-end on incrementally disappointing accommodation prospects, while the commodity complex ex crude oil and bitcoin are also in the red. Conversely, the greenback is gaining and volatility protection instruments are experiencing demand alongside forecast contracts.

This morning’s benchmark revision to nonfarm payrolls removed half of the employment gains that were believed to have existed during the 12 months through March, signaling that the labor market was much weaker than initially perceived at the beginning of the year when the Trump administration took office. The 911,000 workers dropped from the number of employed individuals represents 0.6% of the total roster and is largely attributed to the Bureau of Labor Statistics’ annual update not benefiting from immigration tailwinds. Many undocumented migrants work more than one job and have been double- or triple-counted in previous prints; however, the yearly modification takes state unemployment claims into account and effectively omits many of those foreigners since they don’t qualify for the insurance program. Other justifications for the huge miss include ancient data collection techniques used by the government as well as declining response rates; yes, submitting numbers is voluntary. The alteration was the greatest on record.

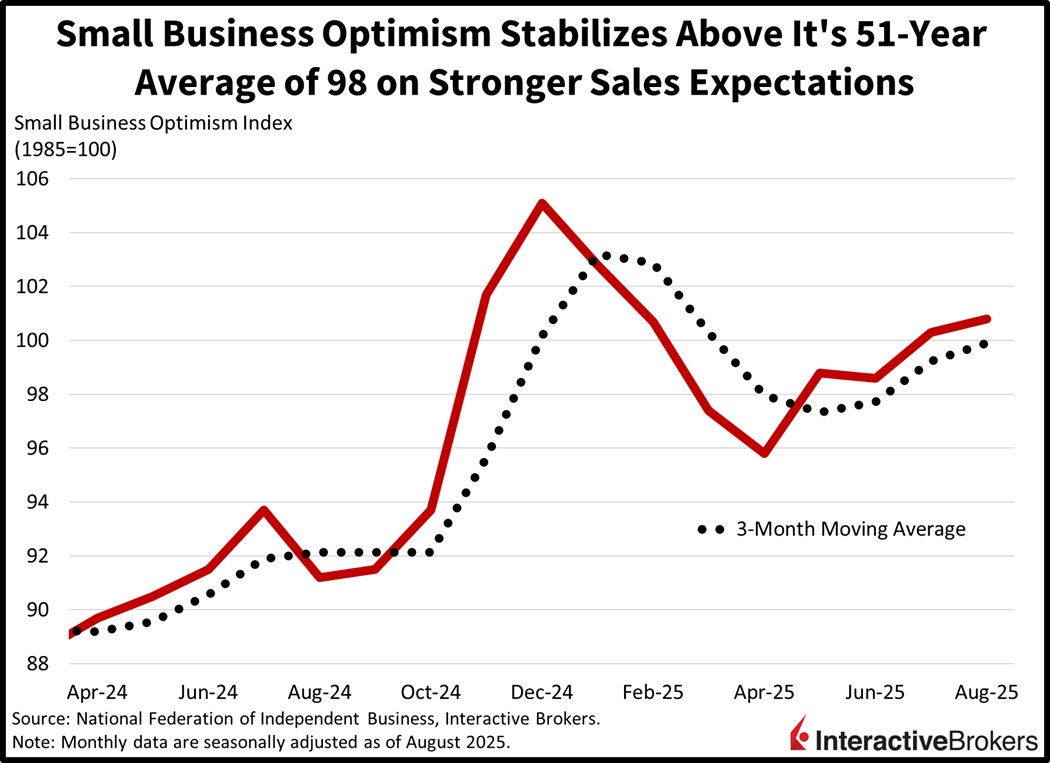

Small company optimism in August rose for the second consecutive month as stronger revenue expectations coincided with reduced uncertainty. The National Federation of Independent Business’s (NFIB) top-line result of 100.8 was slightly below the projected 101 but better than July’s 100.3. An advancing outlook for sales, favorable earnings trends, plans to increase headcounts and subdued inventory all contributed to the month-over-month gain in the overall print. However, capital expenditure prospects, confidence concerning economic conditions, current job openings and corporate expansion sentiment contained progress. Meanwhile, 21% of firms identified quality of labor as the single most-important problem while, 17%, 11% and 10% cited taxes, inflation and weak transaction activity.

While today’s payroll benchmark revision was unfriendly to investors because it sent interest rate rates north instead of south, this week’s inflation reports will provide additional opportunities for Treasury bulls. I think the bar is elevated with the consensus expectation for the Producer and Consumer Price Indices (PPI & CPI) hovering at 3.3% and 2.9%. Indeed, my estimates are lighter at 3.1% and 2.8%, but even those weaker-than-expected figures won’t motivate a 50-basis point reduction from the Fed next Wednesday. Still, those numbers alongside strong showings at government debt auctions totaling $58 billion, $39 billion and $22 billion across the 3-, 10- and 30-year maturities to start this afternoon and continue through Thursday could drive yields much lower, especially at the long-end. Finally, levels below 4% on 10s and eventually beneath 4.50% on 30s amidst an expanding economy bode well for corporate earnings, equity valuations and a year-end stock market rally as a result.

The Bank of England’s monetary easing combined with an assist from favorable weather appears to have increased domestic consumption with the British Retail Consortium (BRC) reporting that August consumer spending climbed 3.1% year over year (y/y) an acceleration from the 1% y/y increase in the year-ago period. The pace also exceeded the 12-month average of 2%.

The central bank last month slashed its key rate from 4.25% to 4%, its fifth reduction of the easing cycle. The bank also revised its forecast for this month’s inflation to 4%. The BRC believes that monetary easing shored up spending despite a decline in consumer confidence. Additionally, sunny weather and a surge in home purchases sparked by real estate buyers seeking to avoid the implementation of Stamp Duty changes in April helped boost sales. Cash register activity for food climbed 4.7% y/y compared to the 3.9% gain in the year-ago period but the improvement is attributed primarily to higher prices. Encouragingly, non-food transactions increased 1.8% compared to the 1.4% drop in August 2024 and the 12-month average of 1%. While back-to-school shopping for clothing was weak, demand for home appliances, garden goods and do-it-yourself products and accessories were strong. Meanwhile, food inflation, higher energy bills, potential tax increases and a weakening job market caused consumer sentiment to fall for the third consecutive month. On the flip side, the BOE’s rate cut and less burdensome mortgage rates are a tailwind for retailers.

Business conditions in Australia improved last month but sentiment among companies weakened, according to the National Australia Bank (NAB). The NAB Business Survey climbed from 5 in July to 7 in August, but the organization’s Business Confidence gauge dropped from 8 to four. Regarding overall conditions, businesses reported better profits and improved employment conditions. Other gains included cash flow, orders, capacity utilization and capital expenditures. Global trade conditions remained unchanged. NAB notes that the drop in confidence follows four months of higher readings and the metric is still close to its long-term average.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!