- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted August 26, 2025 at 12:55 pm

Yesterday, we taped and released a podcast. The main topic was about the markets’ reactions to Chair Powell’s Jackson Hole address, but I brought up a key element of stocks’ behavior over recent sessions. It’s something that I call the “ratchet effect”, and today I’ll explain what it is and why I believe it is critical to understanding the current market climate.

The podcast contains this snippet:

I think what we saw Friday was more of what I’ve been calling the “ratchet effect” in markets. We go down slowly when we go down. When we do have down days—as rare as they seem—they tend not to be of a huge magnitude. But when we go up, we go up big. So, we have this big up move, then ratchet lower, then up again. It’s akin to turning a ratchet.

Allowing for the fact that I repetitively ramble more when I speak extemporaneously than when I write, I’d like to think that the ratchet analogy is clear to anyone who uses hand tools, but for those who don’t:

A ratchet (occasionally spelled rachet) is a mechanical device that allows continuous linear or rotary motion in only one direction while preventing motion in the opposite direction.

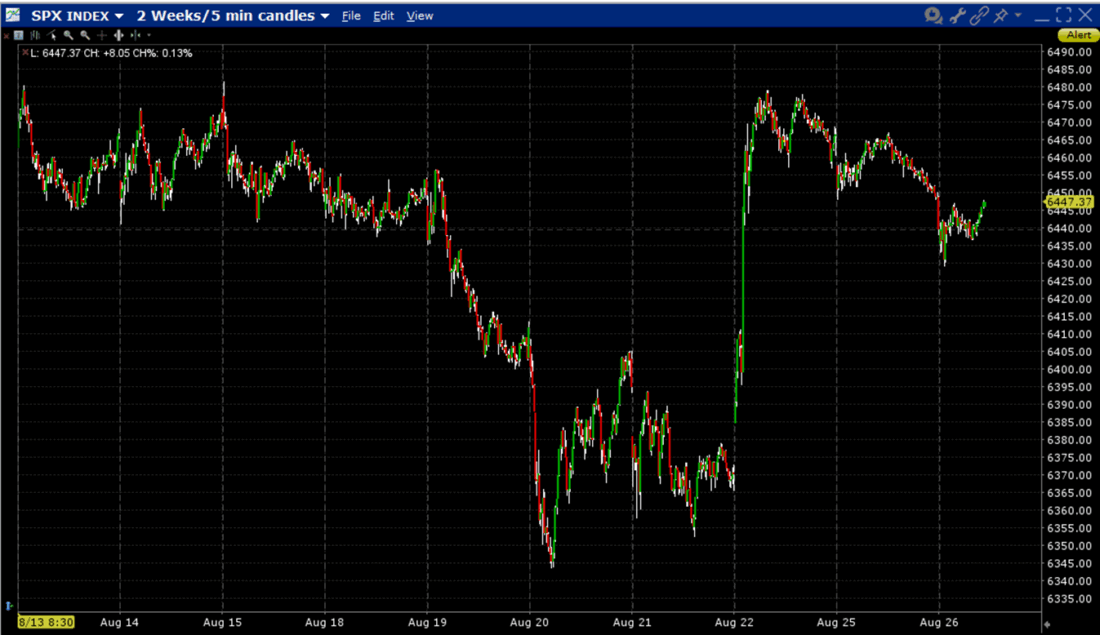

That seems to describe the direction of most broad indices recently. Occasionally when using a ratchet, we can get some minor backwards slippage, and that seems to be an apt way of describing the minor dips that have punctuated the explosive rally that has been in place since the April lows. We don’t go up every day, but the declines have been relatively rare and modest, while the upward moves have often been significant.

Think about the market activity over the past two weeks. The S&P 500 (SPX) had been moving roughly sideways about two weeks ago, then had a relatively sizable dip – at least by recent standards – about a week ago. That dip was erased within about a 10-minute period on Friday when Powell’s speech was released, yet the powerful rally only pushed SPX to a 0.3% gain for the week, though.

Source: Interactive Brokers

I firmly believe that the magnitude of the post-Jackson Hole move was abetted by the fact that it occurred on a Friday. As we noted yesterday:

Fridays are the ultimate ratchet days because not only do you have the usual daily expirations in major indices and ETFs, you also have weekly options expiring for over 600 big companies and other decent-sized ETFs. So it’s much easier to get these things running on a Friday. I don’t think it was a coincidence.

We noted the Friday effect as early as 2021. There was a propensity for markets to have outsized upward moves on Fridays during the post-Covid run-up. The reason was that options traders learned that if enough of them piled into expiring calls, their activity could push markets higher. Since then, the industry has of course added daily expirations, so called “0DTE” options, but Fridays still matter. The daily expirations of key indices and related ETFs, especially SPX, can indeed propel markets higher on any day of the week, but on Friday we have another 600+ stocks and ETFs with expiring options. If a broad rally is in the cards, it is easier to achieve on Fridays.

Note here that I’ve focused solely on the upside. Quite frankly, we don’t see the same enthusiasm for selling as we do for buying — even during market declines. Speculators prefer to trade from the long side than the short side. Also, the tendency for active traders to buy dips means that many are more poised to seek buying opportunities than to exacerbate market declines. This plays into the ratchet effect.

It will be important to see if this recent effect stays in place. We saw some late profit-taking yesterday, but that activity and this morning’s sideways movement doesn’t negate the theory. We’ll get a stern test on Thursday when the market reacts to the Nvidia (NVDA) earnings that are released after the close. A well-received result could lead to another ratchet up. Would a poorly received result be insulated by that ratchet effect? We’ll know at least one answer soon enough.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Options involve risk and are not suitable for all investors. For information on the uses and risks of options, you can obtain a copy of the Options Clearing Corporation risk disclosure document titled Characteristics and Risks of Standardized Options by going to the following link ibkr.com/occ. Multiple leg strategies, including spreads, will incur multiple transaction costs.

Any discussion or mention of an ETF is not to be construed as recommendation, promotion or solicitation. All investors should review and consider associated investment risks, charges and expenses of the investment company or fund prior to investing. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

I like thinking of price range, for the market or even for a wild child stock like TSLA, as slide rule. The range slides up and down and sometimes ratchets higher, and sometimes lower. Nurse Rached (also known as “Big Nurse”), as played by Louise Fletcher alongside Jack Nicholson, the main antagonist of One Flew Over the Cuckoo’s Nest, who was first featured in Ken Kesey’s 1962 novel, is likely the ultimate authority on this effect. => ok’8); ? It would be a moral hazard to guess who the functional equivalent of her, and the role she played in that drama might be in the drama that is today’s markets.

The biggest ratchet effect that I can recall was from the mid thru the late ‘90”s. Something that a previous Fed head referred to as “irrational exuberance”. Many thought for the first few years that it was a party that would end badly, but finally almost all piled in and caused a major blowout after the turn of the century. The big difference is P/E‘s. have not grown to the extremes of then, but this party has been of a much shorter duration. .

Isn’t this called a bullish flag??

No, it’s a white flag of the bulls finally surrendering to the bears!! We’ll be as kind to them as the RABID bulls have been to us. EPIC valuations, RABID bullishness, recession on the horizon…what could go wrong…especially with a TYRANT pulling the strings…hang on to your tail pipe, this one is for the history books!