- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted August 4, 2025 at 12:58 pm

One could assert that Friday’s market could have been even worse, considering everything that was thrown its way. We had already written about the implementation of tariffs and the jobs report that featured a stunning revision which led to a reassessment of the economic situation and the likelihood for imminent rate cuts. Then in the afternoon, we learned of the President’s intention to fire the head of the Bureau of Labor Statistics (BLS), the resignation of a Fed Governor, and the $200+ million verdict against Tesla (TSLA). Put that all together, and a big decline seemed more than understandable.

Then, as if on cue, the dip buyers emerged in force this morning. We have frequently referred to momentum-driven markets as obeying Newton’s First Law of Motion:

A body remains at rest, or in motion at a constant speed in a straight line, unless it is acted upon by a force.

Friday’s market was emblematic of that effect. Stocks had been following very solid uptrends, with external factors seemingly providing insufficient forces to disrupt the upward motion. Sure, some stocks were battered recently by unpleasant reactions to their earnings reports, but even those downdrafts were not enough to darken the market’s mood entirely. Only after a confluence of factors was that path disrupted.

But today, like so many others, seems to be obeying a modified version of Newton’s Third Law of Motion:

To every action, there is always opposed an equal reaction; or, the mutual actions of two bodies upon each other are always equal, and directed to contrary parts

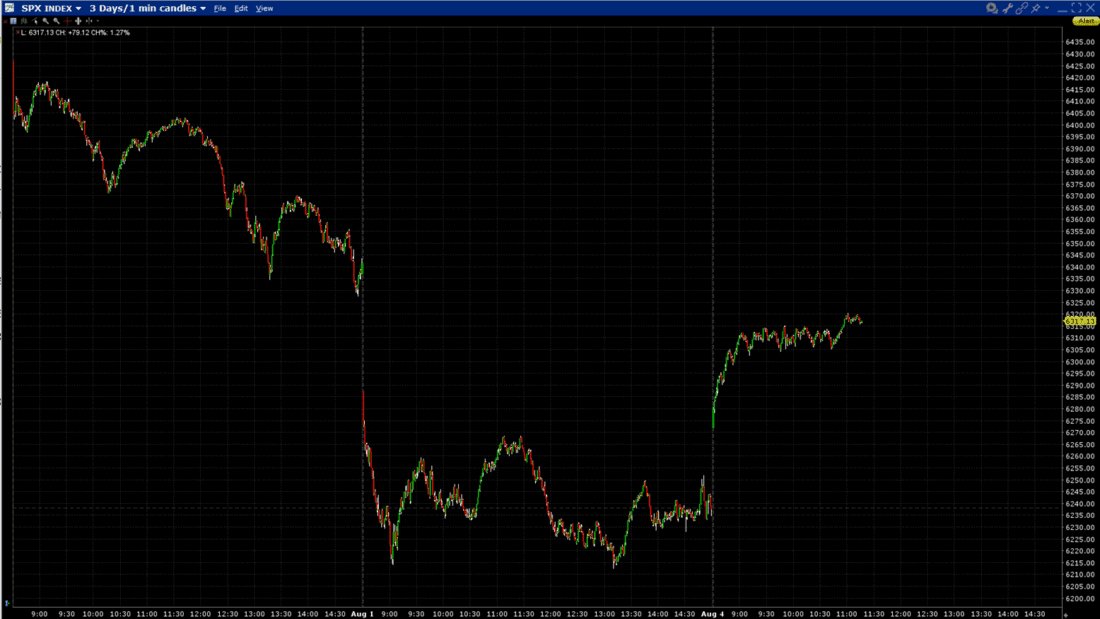

While the now-routine attempts to buy dips and then chase the bounces are not exactly equal and opposite reactions, they seem to come awfully close. As I type this around noon EDT, the S&P 500 (SPX) has recouped most of, but not quite all, Friday’s decline:

Source: Interactive Brokers

The gap from Thursday has so far been nearly filled, but not completely. Thursday’s low was 6327.64 (with a 6362.90 close), and today’s high as of now is 6320.35. A push to close the gap seems kind of inevitable, no?

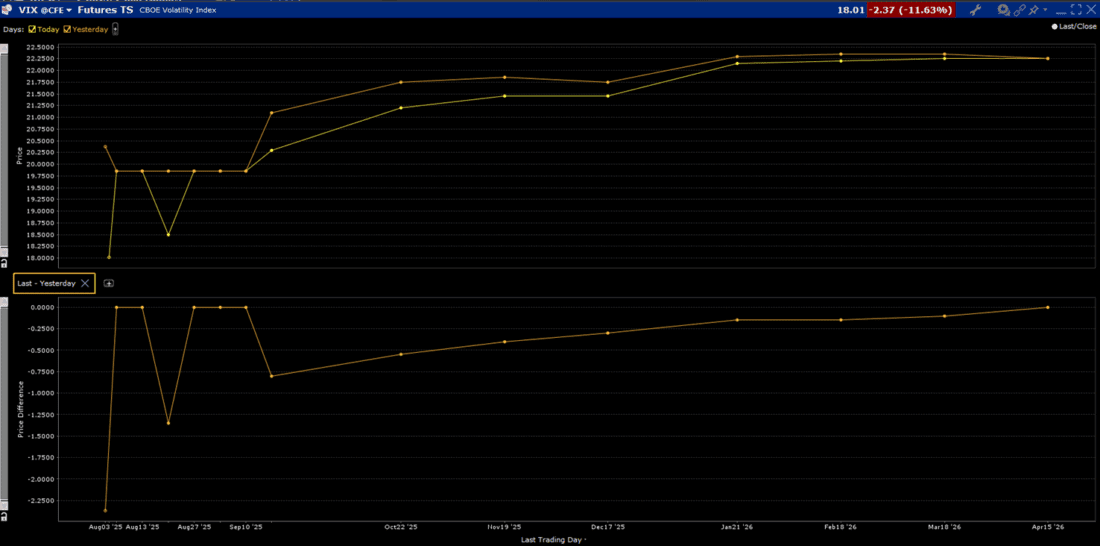

Unlike Friday’s decline, which was quite easily explained, the cause for today’s rally is a bit murkier. It could be that rate cut expectations have solidified, but the odds for a cut haven’t improved markedly since Friday, nor have we seen a significant move in 2-year rates today to reaffirm that. It could be a reaffirmation of the “Fed Put”, the thought that impending rate cuts will bolster stocks no matter what. That is basically a reiteration of the prior point, with the caveat that the “Fed Put” is not really about the stock market at all – it is the Federal Reserve stepping in to protect the broader economy or money market liquidity. Besides, if that was the case we would expect to see longer-term VIX futures decline – why buy protection if the Fed will give it to you for free? Despite the plunge in spot VIX and short-term futures, the long end is relatively firm:

Source: Interactive Brokers

In this case, I think the simplest explanation is the best. Buying dips has worked so spectacularly well for active traders recently that they are loath to abandon that strategy. Who can blame them when it has worked so spectacularly well? It’s not a question of whether traders will attempt to buy dips, but how aggressively will they step in during the decline and how aggressively will they chase the seemingly inevitable bounce. For today at least, it is very nearly an equal and opposite reaction, with very little news and positive sentiment almost balancing out a highly consequential flow from the prior session.

New to Interactive Brokers?

Open AccountAlready an Interactive Brokers Client?

Request Trading PermissionThe analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

")

I THINK THE TIME HAS COME FOR CHAIR POWELL TO HUDDLE WITH HIS TEAM AND THINK ABOUT CHANGING HIS/ITS PHILOSOPHY. HE CONSTANTLY DECLARES THAT HE HAS TWO MANDATES. BUT MAYBE THE TIME HAS COME FOR HIM/THEM TO RE- DEFINE THE ‘STABLE PRICES’ MANDATE. YES, HE WANTS TO KEEP PRICES LOW, BUT BY KEEPING RATES TO HIGH HE CHOKES-OFF THE ECONOMY. POSSIBLY THIS IS A NEW LOOK FOR THE ECONOMIC PICTURE WITH ALL THE NEW/STRANGE/UNUSUAL HAPENINGS? THOUGH THE TARIFFS WILL INCREASE PRICES TO THE CONSUMER, HIGH RATES WILL POSSIBLY HAVE A MORE SIGNIFICANT NEGATIVE EFFECT ON THAT CONSUMER. THE BIG PROBLEM FOR POWELL MIGHT JUST BE THAT HE REFUSES TO GIVE TRUMP HIS CAKE AND LET HIM EAT IT TOO. HE DOES THAT BY LOWERING THE RATES AS THE TARIFFS CONTINUE TO EXIST.