- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted July 16, 2024 at 11:15 am

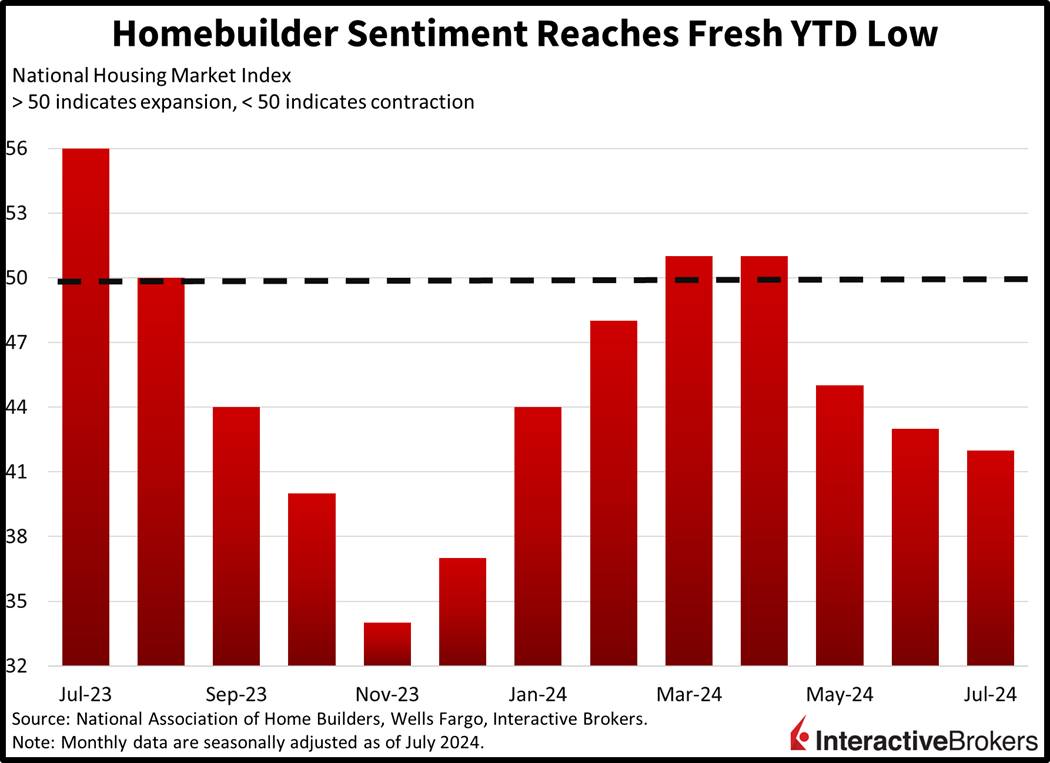

This morning’s solid retail sales report is emboldening the Trump trade as the Dow Jones and Russell 2000 benchmarks soar at the expense of popular technology names. American consumers are certainly flaunting their shopping bags, fresh kicks and Amazon gift cards, but domestic homebuilders have extended their leases at nearby storage units where they’re parking their hammers, screwdrivers, tape measures and circular saws as they await better conditions in the real estate sector. Indeed, this morning’s sentiment data was the worst of the year, as an unfavorable price/rate mix continues to dent affordability.

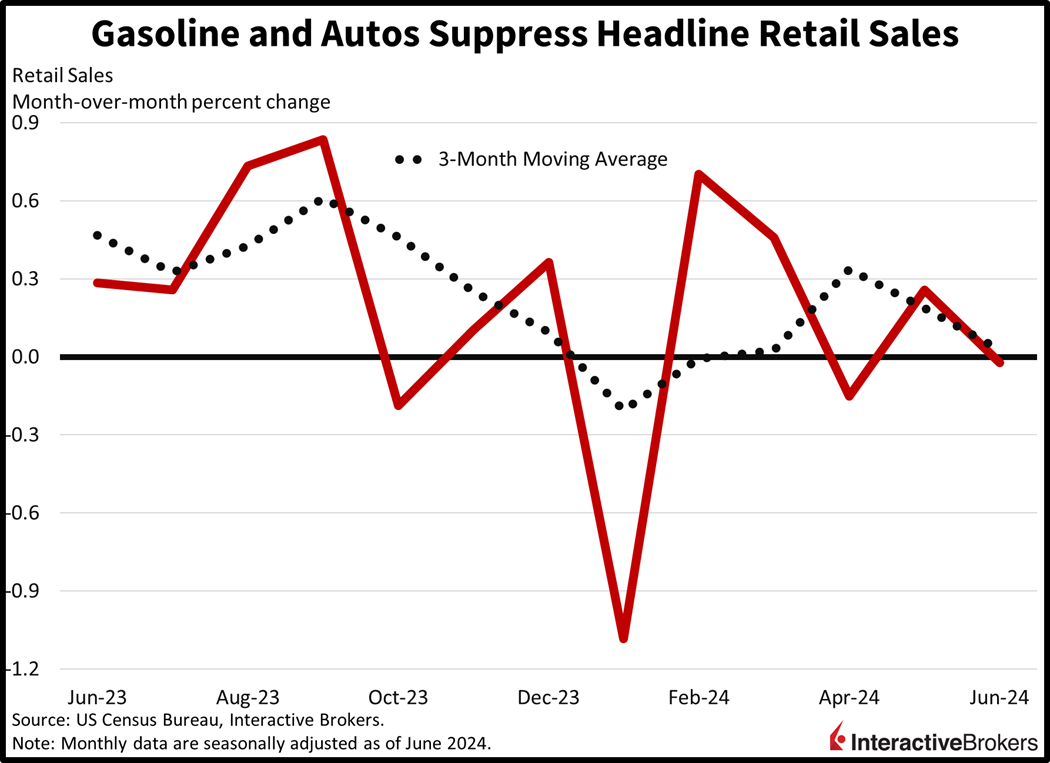

Consumers picked up their spending pace on core categories last month, with transactions reflecting broad-based strength despite acute weakness isolated to automobiles and gasoline. Dealership cyberattacks are to blame for the former category. Indeed, declines in those two areas contributed to a flat month over month (m/m) reading, in-line with projections and slower than May’s 0.3% increase. June’s transactions excluding automobiles rose 0.4% m/m, meanwhile, and increased 0.8% m/m when omitting automobiles and gasoline. Both figures accelerated from May’s 0.1% and 0.3% while surpassing expectations for 0.1% and 0.2% growth.

Despite the stagnant headline figure, ten of thirteen major components sported gains. The leading growth categories and their m/m increases included the following:

Electronics shops, general merchandise retailers, miscellaneous stores, dining establishments and food markets experienced smaller upticks of 0.4%, 0.4%, 0.3%, 0.3% and 0.1%. Weighing on overall results were gasoline stations, automobile dealerships and sporting goods boutiques with declines of 3%, 2% and 0.1% m/m.

Homebuilder sentiment tanked this month as the gap between sellers’ asking prices and buyers’ spending limits remained historically wide. The NAHB/Wells Fargo National Housing Market Index fell to 42, beneath the median projection of 44 and June’s 43. The pace of single-family sales and traffic of prospective buyers weighed on the headline figure, with this month’s numbers arriving at 47 and 27, each a point lower than June’s level. Encouragingly, the outlook for single-family sales over the next six months improved marginally from 47 to 48 during the period. From a regional perspective, top-line results for the Northeast, Midwest and West declined from 62, 40 and 38 to 47, 39 and 37. The South remained steady at 43.

Investment banking continues to be a sweet spot for second-quarter earnings while other forms of non-interest income are also helping to boost financial firms’ results. In the medical industry, however, UnitedHealth Group reported growing expenses. Consider the following earnings highlights:

Markets are tilted bullish today as investors scoop up value and small cap stocks, which tend to be domestically oriented and perceived to benefit disproportionately from a Trump victory in November. The dollar is higher, though, despite steady yields, a result of stronger consumption data and brighter economic prospects relative to global counterparts. All major US equity indices are pointing north with the Russell 2000, Dow Jones Industrial, S&P 500 and Nasdaq Composite baskets higher by 2.5%, 1.6%, 0.5% and 0.1%. All eleven sectors are loftier except for technology, which is down 0.4%. Leading the bulls are industrials, materials and healthcare, which are up 2%, 1.4% and 1.3%. The Dollar Index is higher by 15 basis points to 104.41 as the greenback appreciates versus all of its major peers, including the euro, pound sterling, franc, yen, yuan and Aussie and Canadian dollars. Treasurys are rather steady, with the 2- and 10-year maturities changing hands at 4.46% and 4.20%. Commodities are mixed, as silver and gold gain 2% and 1.5% while lumber, copper and crude oil lose 1.8%, 1.1% and 1%. Domestic real estate sluggishness is weighing on lumber, and Beijing’s lighter-than-anticipated GDP print of 4.7% is concerning oil watchers of possible demand weakness from the world’s largest importer. WTI crude is being offered at $81.06 per barrel against this backdrop.

With former President Trump’s odds of recapturing the White House roaming north of 70% in most surveys, market participants are certainly rushing to stocks that could benefit the most from his proposed policies. Investors are perceiving that industrials, materials, financials, healthcare and energy will thrive from Trump tax cuts 2.0, increased tariffs and a deregulatory agenda. Technology, however, is lacking momentum because the category has a disproportionate reliance on China, and segregated manufacturing hubs may hurt the sectors’ performance if US protectionism strengthens. Furthermore, Trump’s selection of J.D. Vance as his running mate is also concerning investors because the senator is a strong supporter of increasing regulation of the industry, including imposing antitrust measures. Finally, the success of Trump’s plans will be heavily dependent on Congressional election results, as odds of a red wave, unlike the general election, are closer to a coin-flip.

Visit Traders’ Academy to Learn More About Retail Sales and Other Economic Indicators

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!