- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted June 6, 2024 at 11:00 am

Markets are struggling for direction today following yesterday’s stellar gains on the back of Ottawa kicking off a synchronized monetary policy easing cycle. Indeed, the EU followed suit this morning, dropping its key rate by 25 bps. Bullish trading action in recent days has been motivated by the expectation that the Fed will follow suit, as bond investors incrementally expand expectations for an accommodative central bank. Tomorrow’s jobs report may certainly move the needle ahead of the Fed meeting next week, which will feature the committee’s quarterly update to its Summary of Economic Projections alongside an estimate of year-end fed funds.

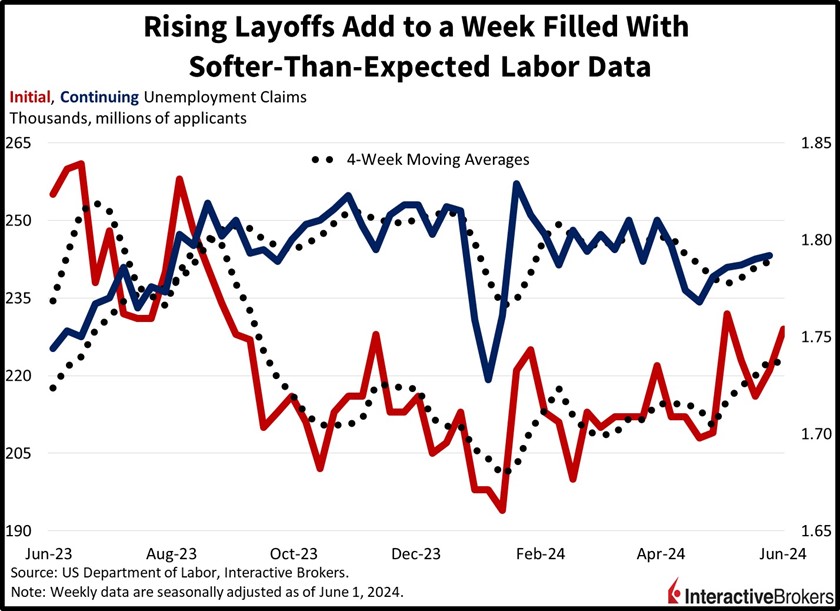

This morning’s unemployment claims data added modest evidence pointing to a slowing labor market, with layoffs picking up slightly. Initial unemployment claims rose to 229,000 during the week ended June 1, exceeding estimates of 220,000, which would’ve been closer to the former week’s 221,000. Continuing claims increased but more modestly to 1.792 million for the week ended May 25, near expectations of what would have been an unchanged 1.79 million. Four-week moving averages reflected mild changes, with initial and continuing claims shifting from 223,000 and 1.786 million to 222,250 and 1.789 million, respectively.

The European Central Bank (ECB) delivered its highly anticipated rate cut this morning with a 25-basis point (bp) reduction, bringing its key figure to 3.75% from a record high. According to an ECB Governing Council statement, the central bank brought out the scissors after determining that slower price pressures and an underperforming economy needed it. At the same time, the bank increased its inflation estimate for this year from 2.3% to 2.5%. It also raised its 2025 outlook from 2% to 2.2%. The ECB action follows yesterday’s decision by the Bank of Canada to lighten up, making it the first member of the Group of Seven to dust off its cutlery.

Recent earnings releases depict consumers cutting back on spending as inflation hurts households’ spending clout. This trend extends across athleisure, deep discounters, lingerie and alcohol companies. Consider the following earnings highlights:

Wall Street is quiet today as investors await tomorrow’s jobs report that may either greenlight the equity rally or create selling pressure. Against this backdrop, equity indices are generally tilting lower while bonds are paring some gains. The Dow Jones Industrials, up 0.1%, is the only gainer, while the Russell 2000, S&P 500 and Nasdaq Composite benchmarks are down 0.5%, 0.1% and 0.1%. Sectoral breadth is split and sporting a defensive tilt as 6 out of 11 sectors trade green. Leading the upside are consumer staples, communication services and healthcare with gains of 0.5%, 0.5% and 0.3%. Treasurys appear tired with investors potentially anticipating higher costs of capital. The 2- and 10-year maturities are yielding 4.73% and 4.29%, 1 and 2 bps loftier on the session. The dollar is near the flatline, meanwhile, as it gains versus the yuan and pound sterling but loses ground relative to the euro, franc, yen and Aussie and Canadian dollars. Commodities are recovering from their recent battering as monetary policy easing prospects calm demand concerns. Silver, lumber, crude oil, copper and gold are all higher by 3.1%, 2.7%, 1.1%, 1% and 0.7%.

This week’s employment data has featured softer-than-expected figures on JOLTS, ADP and unemployment claims, but tomorrow’s employment situation report will carry the most weight for investor sentiment and the Fed’s decisions. I’m expecting another miss tomorrow with the headline figure arriving at 165,000 alongside wage growth of 0.3% and the unemployment rate ticking up to 4%. The numbers are likely to bolster rate reduction projections further, but Fed officials will want more labor market moderation considering recent miscues. In conclusion, next week’s inflation data will finally offer the first month of price pressures rising at a pace consistent with the central bank’s 2% objective in the very short-term, a month over month rate of just 0.1%. Whether the market focuses on liquidity arrivals from the Fed or earnings prospects against the backdrop of rising joblessness is an answer we’ll have tomorrow morning.

Visit Traders’ Academy to Learn More About Unemployment Claims and Other Economic Indicators.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

for Daily Seasonal Data")

thank you for the brilliant article.

We hope that you continue to enjoy Traders’ Insight!