- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted April 18, 2024 at 11:15 am

Investors’ optimism that the worst of the Middle East crisis is behind us alongside strong corporate earnings and a diverse mix of economic data is pushing stocks higher. Today’s data include a continued rebound in manufacturing, persistently tight labor conditions, and a decline in both existing home sales and the Conference Board’s Leading Economic Index. Equities are indeed looking to break their four-day losing streak as they’ve snapped back from morning losses despite multiple Federal Reserve speakers recalling their recent frowns following employment and inflation data that have been too hot for the central bank’s liking.

Elevated mortgage rates took a bite out of existing home sales last month as prospective buyers shook their heads at the sight of a 7 handle. Transactions fell 4.3% month over month (m/m) and 3.7% year over year (y/y) to 4.19 million seasonally adjusted annualized units (SAAU). March’s figure was narrowly below projections of 4.2 million SAAU, and it slipped from February’s 4.38 million SAAU. Both the single-family and condominium/cooperative segments contributed to the decline, with the components dropping 4.3% and 4.9%, respectively, m/m. Across regions, the West, South and Midwest weighed on results, with m/m sales down 8.2%, 5.9% and 1.9%. The Northeast offered some strength, however, with an increase of 4.2%. Prospective sellers may be growing impatient with the sluggish pace of sales since 2022, though, with inventory climbing 4.7% m/m and 14.4% y/y. Rising listings pushed up the ratio of unsold inventory at the current sales pace to 3.2 months, up from 2.9 in the previous month and 2.7 during the same period last year. Similar to what’s been happening in the new home market, sellers are likely to begin discounting to achieve closings, as the long-awaited move to lower mortgage rates hasn’t materialized.

The Conference Board’s Leading Economic Index returned to contraction territory last month following February’s positive result. The benchmark dropped 0.3% m/m, missing estimates of a 0.1% fall while slipping from February’s 0.2% rate of expansion. Driving the measure lower were the bear-steepening yield curve, declining plans for residential construction, consumer expectations of future business conditions and demand for goods and services. Meanwhile, rising stock prices, tight credit spreads and a longer hourly work week in the manufacturing sector were some of the positive contributors within the report.

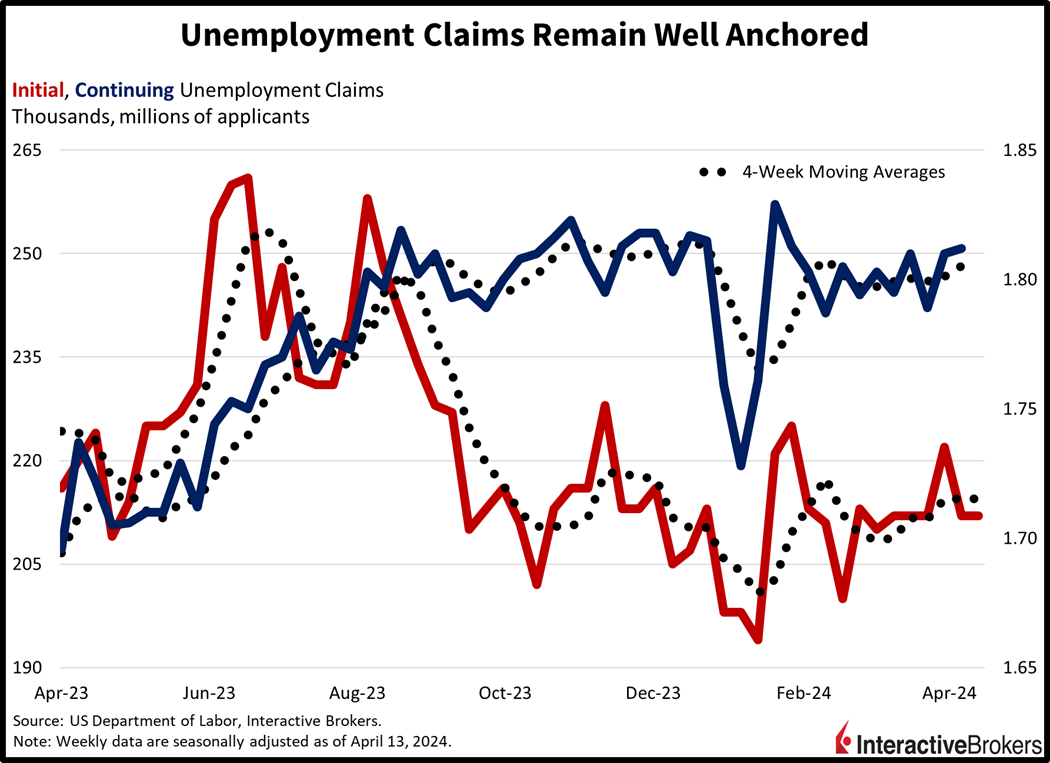

The labor market remains well anchored, with corporates showing little appetite to lay off employees. This morning’s Unemployment Claims report from the US Department of Labor was little changed from the prior week. Initial unemployment claims remained at 212,000 for the week ended April 13, while missing projections of 215,000. Continuing unemployment claims for the week ended April 6 came in at 1.812 million, near the 1.810 million from the previous week and the consensus anticipation of 1.818 million. The longer-term trend didn’t shift much, with the four-week moving average on both initial and continuing components coming in at 214,500 and 1.805 million, unchanged from the previous week for the former and close to the last reading of 1.801 million for the latter.

Realtors’ sale pending signs may be gathering dust, but factories are revving up production with the Philadelphia Fed’s Manufacturing Index climbing sharply this month, a result of activity, demand, shipments and pricing power all strengthening. April’s figure of 15.5 trounced expectations of 1.5 and rose from March’s 3.2 level. However, employment declined as manufacturers attempted to sustain margins amidst loftier wages. Firms remained optimistic about conditions over the next few months, with the future activity sub-index slipping slightly but remaining at elevated levels relative to post-pandemic readings.

Chinese tourism is still benefiting from pent-up demand resulting from Covid-19 pandemic restrictions while in the US, railroad freight volume, broadly speaking, is steady. Elsewhere, artificial intelligence is supporting demand for computer chips. Those are a few points from the following earnings highlights:

Stocks are recovering from their recent battering while taking their cues from better-than-feared developments from the Middle East. Stock bulls are also benefitting from a trading community that got too hedged up, considering oversold technical levels, elevated fears and towering volatility gauges. Bond traders are less optimistic, however, with the fixed-income community gathering their evidence from the hot Philly Fed, low unemployment claims and hawkish Federal Reserve rhetoric. Rate analysts are also looking at a bifurcated commodity market, with oil prices lower on simmering Middle East tensions but copper higher on firmer manufacturing data and undersupplied conditions. For stocks, all major US equity indices are higher while sporting a cyclical tilt, as the Russell 2000, Dow Jones Industrial, S&P 500 and Nasdaq Composite baskets are higher by 1%, 0.6%, 0.5% and 0.3%. Sectoral breadth is positive with all segments higher led by financials, communication services, industrials and materials; they’re up 1%, 1%, 0.6% and 0.6%. In fixed-income land, the 2- and 10-year Treasury maturities are trading at 4.64% and 4.99%, 5 basis points (bps) higher on the session for both durations. The dollar is benefiting from higher rates, strong economic data and a severely weakened Japanese yen that may require central bank stabilization in short order. The greenback’s index is up 15 bps to 106.01 as the US currency gains relative to the euro, pound sterling, franc yen and Aussie dollar. It is dropping versus the Canadian dollar and the yuan, however. WTI crude oil is down 0.2%, or $0.20, to $82.06 per barrel with traders dialing down their geopolitical war premium as it seems likely that another direct confrontation between Tehran and Tel-Aviv won’t occur in the short term.

While lower oil prices could support disinflation in coming months, that effect may be countered by copper, to some extent. Copper prices are up to their highest levels since June 2022, as the global economy’s manufacturing sector poses a sharp recovery. Helping drive the upside are lower interest rates around the world and a demand comeback. Consumers splurged on goods during the pandemic since many services weren’t available, frontloading a lot of the demand that would’ve otherwise been allocated to 2022 and 2023. Today, however, it’s time for many consumers and corporates alike to replace their older products bought during the lockdowns. This effect is especially inflationary since many supply chains have been rerouted and some production stages onshored, as globalization continues to shift towards regionalization. A sharp decline in oil prices may or may not offset the inflationary implications of the manufacturing sector’s powerful comeback.

Visit Traders’ Academy to Learn More About Existing Home Sales and Other Economic Indicators.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!