- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Lesson 9 of 11

New to Interactive Brokers?

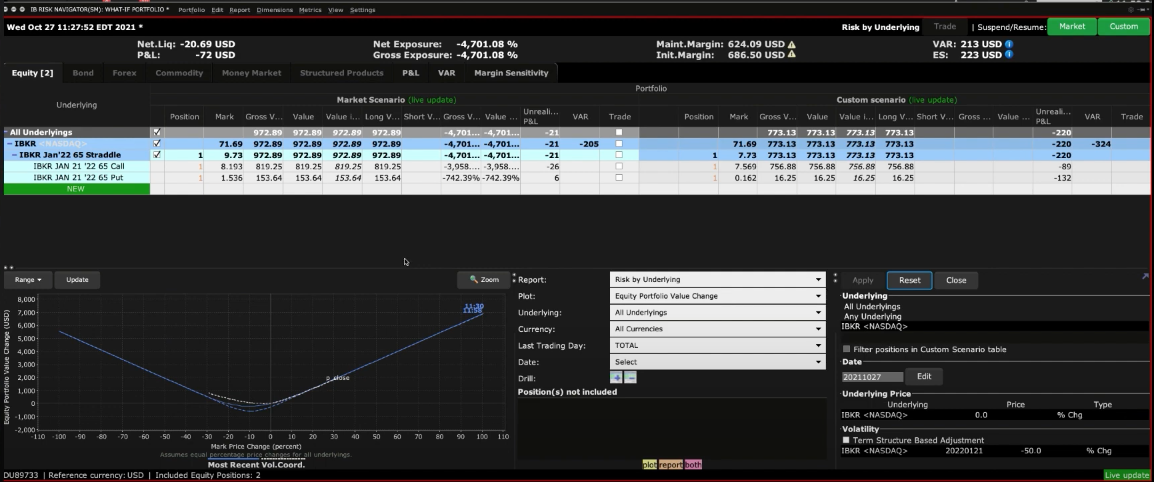

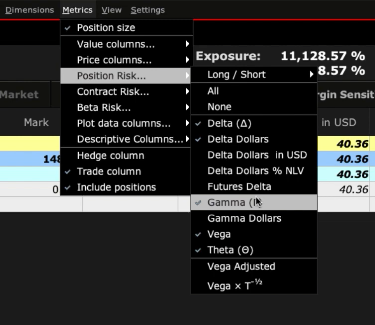

The TWS Risk Navigator is a powerful tool and can be used to calculate the likely forward price of single options and option combinations. In this video we will go through how to use the Risk Navigator what-if custom scenario feature to make assumptions on the forward price of an underlying and implied volatility to measure the potential price of an option and combination on various days leading up to expiration. Let us start by going to a Watchlist I previously created with options and combinations on it. To bring up a new Risk Navigator What If right-click on an option and scroll down to display What-if. A Risk Navigator What-if display will populate with just this single option. Notice that the border of the Risk Navigator is Red indicating it is in edit mode. To access available columns, go to the Metrics Menus. Scroll down to see available column areas. Choose the metrics you want, and the available columns will show. I recommend adding in the following position risk columns: Delta, Delta Dollars, Gamma, Vega, and Theta if they are not already selected. You are now displaying market prices and associated values.

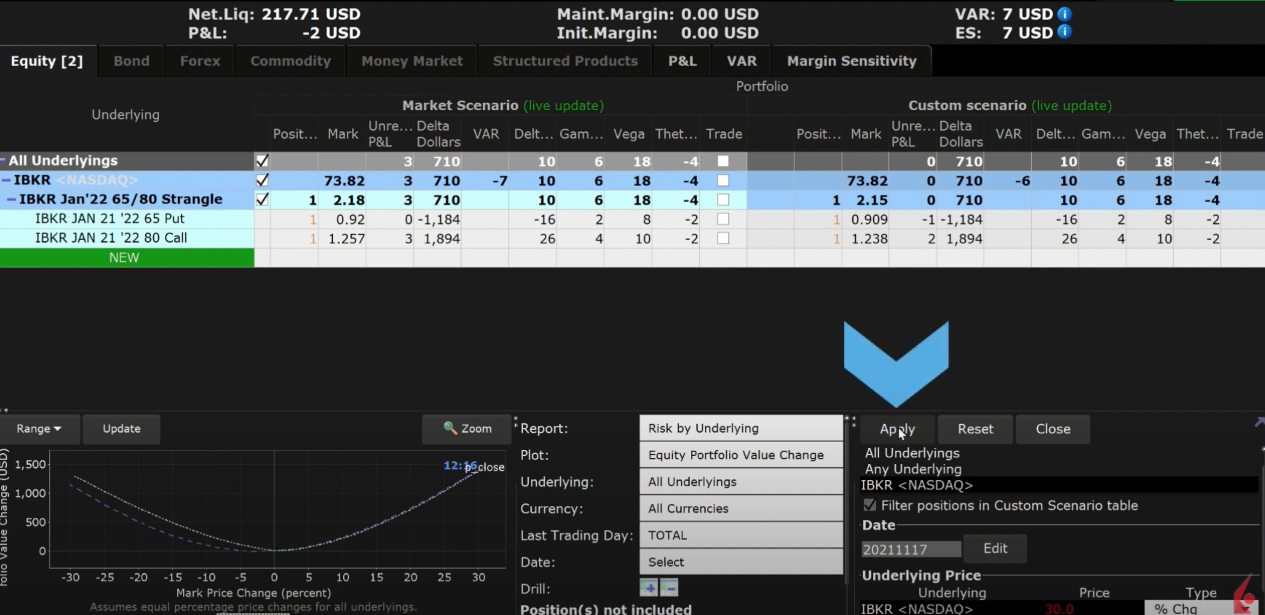

Let us start by going to a Watchlist I previously created with options and combinations on it. To bring up a new Risk Navigator What If right-click on an option and scroll down to display What-if. A Risk Navigator What-if display will populate with just this single option. Notice that the border of the Risk Navigator is Red indicating it is in edit mode. To access available columns, go to the Metrics Menus. Scroll down to see available column areas. Choose the metrics you want, and the available columns will show. I recommend adding in the following position risk columns: Delta, Delta Dollars, Gamma, Vega, and Theta if they are not already selected. You are now displaying market prices and associated values.  We will now bring up the custom scenario by going to the view menu at the top of the screen and scrolling down to custom scenario. This will replicate the market scenario with a custom scenario on the right of the screen.

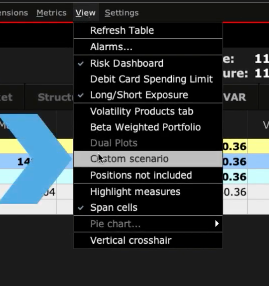

We will now bring up the custom scenario by going to the view menu at the top of the screen and scrolling down to custom scenario. This will replicate the market scenario with a custom scenario on the right of the screen.  You can adjust the underlying price, the option volatility for the expiration, and even set a final settlement price. Let’s walk through a few scenarios to see how they affect the price of the option. I have selected a long call option for our first example. The aim here is to learn the premium of the option by first increasing the price of the underlying by $15 and second, reducing the reading for implied volatility by 15%. Let’s first adjust the underlying price. There are 3 choices: Explicit Value, Change, or Percent Change. We will increase the underlying price by typing $15 into the box underneath price, changing the type to “chng”. Note that whenever you edit any inputs here, the font will remain red until you apply the change. Click “Apply”. The value of the option has increased reflecting the change in the underlying. This can be seen in both the data table and the plot. I’ll now reset the scenario editor and adjust the volatility by lowering it 15% to show the effect on the option pricing. You can now see how the premium of the option has declined for a reduction in implied volatility.

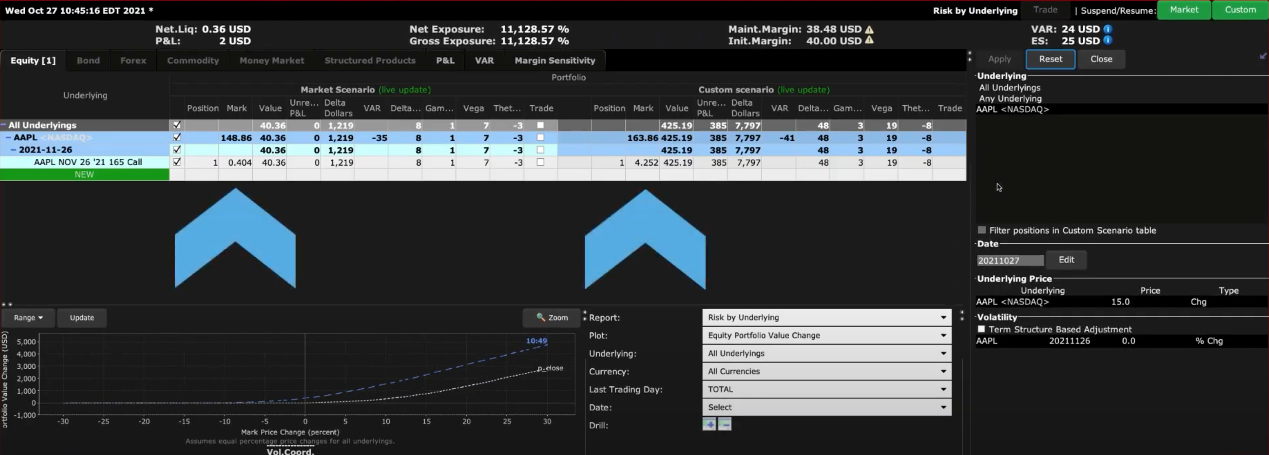

You can adjust the underlying price, the option volatility for the expiration, and even set a final settlement price. Let’s walk through a few scenarios to see how they affect the price of the option. I have selected a long call option for our first example. The aim here is to learn the premium of the option by first increasing the price of the underlying by $15 and second, reducing the reading for implied volatility by 15%. Let’s first adjust the underlying price. There are 3 choices: Explicit Value, Change, or Percent Change. We will increase the underlying price by typing $15 into the box underneath price, changing the type to “chng”. Note that whenever you edit any inputs here, the font will remain red until you apply the change. Click “Apply”. The value of the option has increased reflecting the change in the underlying. This can be seen in both the data table and the plot. I’ll now reset the scenario editor and adjust the volatility by lowering it 15% to show the effect on the option pricing. You can now see how the premium of the option has declined for a reduction in implied volatility.  We will now go through some examples using a strangle combination. From the Watchlist we created click on a strangle. We can choose to either add it to the existing What if that is open or open an entirely new one just for the combination. We will open a new one. I’ll make some exaggerated adjustments to emphasize the changes and point them out on both the plot and the table. Examples using Strangle Combination

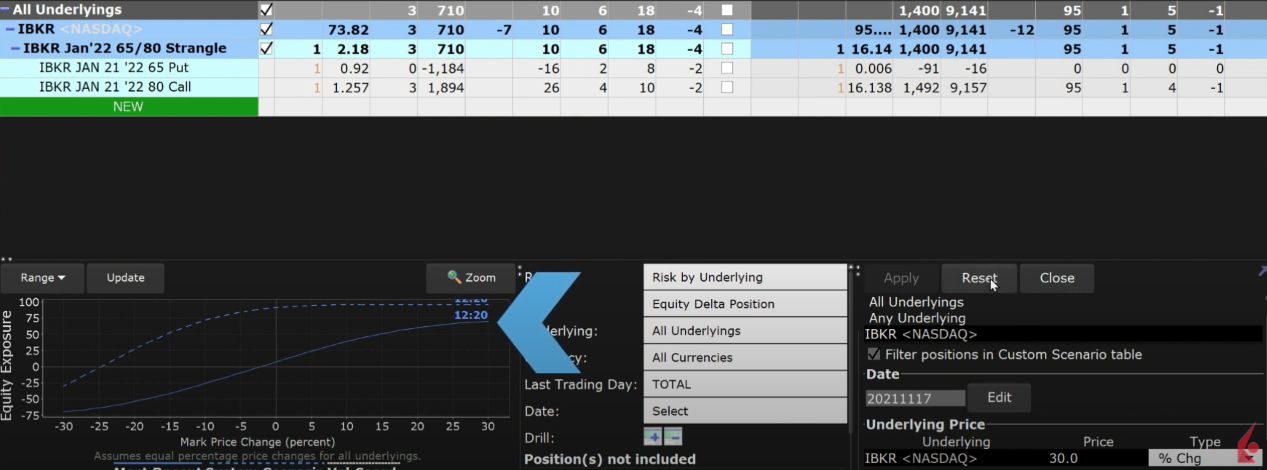

We will now go through some examples using a strangle combination. From the Watchlist we created click on a strangle. We can choose to either add it to the existing What if that is open or open an entirely new one just for the combination. We will open a new one. I’ll make some exaggerated adjustments to emphasize the changes and point them out on both the plot and the table. Examples using Strangle Combination  Looking at the plot I’ll change to Equity Portfolio Value and then equity delta position. Notice the dotted blue line which is the scenario versus the solid blue line, which is the solid blue line which is the most recent market scenario.

Looking at the plot I’ll change to Equity Portfolio Value and then equity delta position. Notice the dotted blue line which is the scenario versus the solid blue line, which is the solid blue line which is the most recent market scenario.  I’ll now reset the price change to zero and adjust the volatility by decreasing it by 50%. Notice now how the price of both the call and the put have decreased drastically from their original value.

I’ll now reset the price change to zero and adjust the volatility by decreasing it by 50%. Notice now how the price of both the call and the put have decreased drastically from their original value. As you can see the Risk Navigator is a powerful tool enabling you to test various scenarios for price, time and volatility to display their impact on the worth of an option. Use the custom scenario functionality to test your trading strategies and learn how to monitor risk through the lens of Greek variables.

As you can see the Risk Navigator is a powerful tool enabling you to test various scenarios for price, time and volatility to display their impact on the worth of an option. Use the custom scenario functionality to test your trading strategies and learn how to monitor risk through the lens of Greek variables.For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Options involve risk and are not suitable for all investors. For information on the uses and risks of options, you can obtain a copy of the Options Clearing Corporation risk disclosure document titled Characteristics and Risks of Standardized Options by going to the following link ibkr.com/occ. Multiple leg strategies, including spreads, will incur multiple transaction costs.

Trading on margin is only for experienced investors with high risk tolerance. You may lose more than your initial investment. For additional information regarding margin loan rates, see ibkr.com/interest

Can I roll options via Risk Navigator?

Thank you for asking. This is not possible. The Risk Navigator is a real-time market-risk management platform that provides a comprehensive measure of risk exposure across multiple asset classes around the globe.Its easy-to-read spreadsheet-like interface lets you quickly identify exposure to risk starting at the portfolio level, with drill-down access into successively deeper levels of detail within multiple report views. For more information on the Risk Navigator, please view this User Guide: https://www.ibkrguides.com/traderworkstation/risk-navigator.htm?Highlight=Risk%20Navigator

For instructions to roll options, please view this FAQ: https://www.interactivebrokers.com/faq?id=34483816

We hope this helps!

Can I see the margin requirements after adjusting an underlying price?

Hi Matyas, thank you for reaching out. Please view this FAQ to monitor your margin requirements in TWS: https://www.interactivebrokers.com/faq?id=27271532