- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Lesson 3 of 4

Already an Interactive Brokers Client?

New to Interactive Brokers?

Portfolios are often designed to balance capital appreciation from equities with income generation from fixed income products. There have been debates over the years about the balance between the two asset classes. One line of thought states that 60 percent of a portfolio should be allocated to equities and the other 40 percent to fixed income. The so-called 60/40 rule should be loosely interpreted and applied to investors depending upon a series of factors including, but not limited to, risk appetite, age as well as the economic and monetary policy outlook.

Based upon the view of the investor, investing in fixed income is a function of willingness to take on risk, liquidity preference and a view on the developments of monetary policy. For example, the investor may only be willing to only buy bonds of investment grade quality. And for the time being they may be willing to invest for no longer than two years. This might be because of a view on monetary policy or the economic cycle, or it may be due to the need to pay for a known event coinciding with the maturity of the bond.

Whether the investor invests in government debt, investment grade or so-called “junk” bonds, whether they invest for 30-days, or 30-years is an individual preference. As is the allocation they choose between stocks and bonds.

While individuals may choose how to allocate their portfolios, the fact is that either asset class exposes them to market risk. For equity investors, market risk means that stocks as an asset class may be vulnerable to a correction or price decline for an extended period of time. Likewise, for fixed income investors, asset prices are equally exposed to market risk associated with falling bond prices or rising yields. In either case investors have access to hedging instruments. Typically, for equities, investors turn to protective put options to hedge their risk. And while fixed income investors can use options in some cases too, the illiquid nature of specific bond issues makes this more challenging.

However, the fixed income market is extremely developed with multiple hedging opportunities available across an array of exchange traded instruments. These are equally utilized by both hedgers and speculators. Hedging involves the offsetting of risk. Speculation involves taking on risk despite the uncertainty of outcomes.

Earlier, we defined two critical factors at the heart of fixed income investing. Those factors are quality and maturity tenure of bonds. Investors are exposed to a change in the structure of the yield curve as well as to shocks to economic growth.

The remainder of this lesson will look at speculation within the futures fixed income world to explain how investors aim to anticipate government or central bank policies that might lead to changing yields.

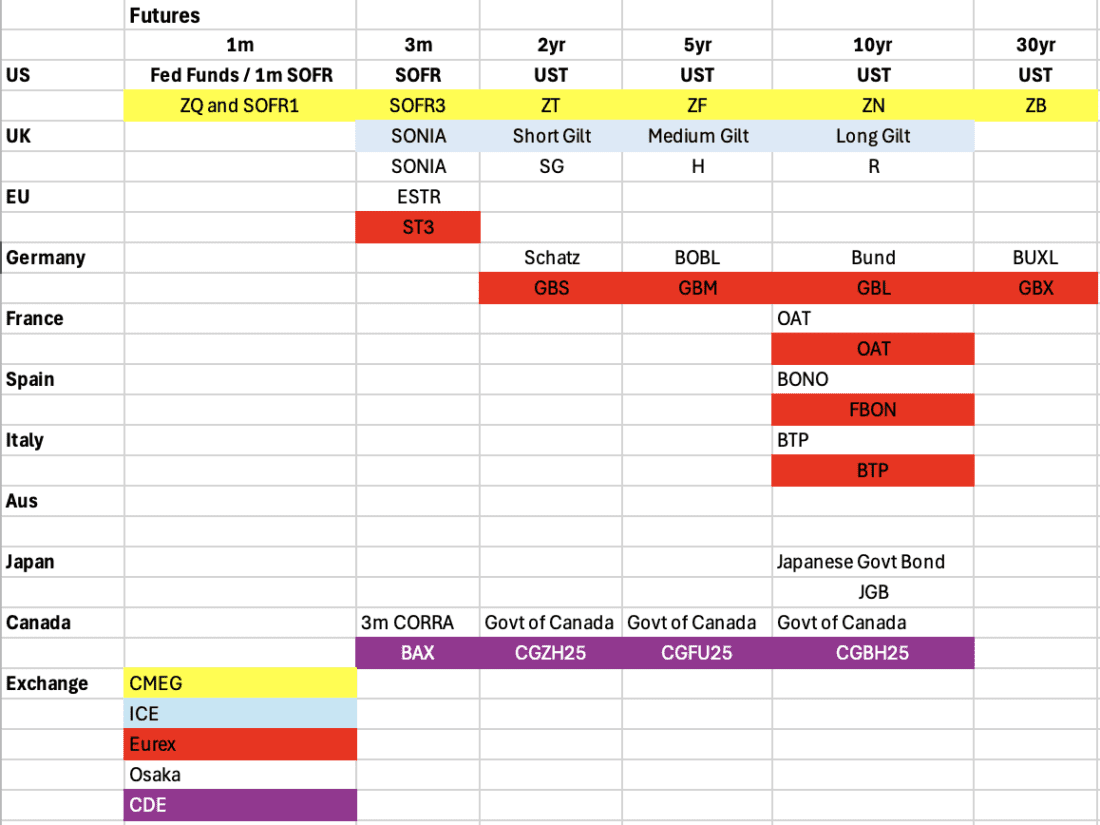

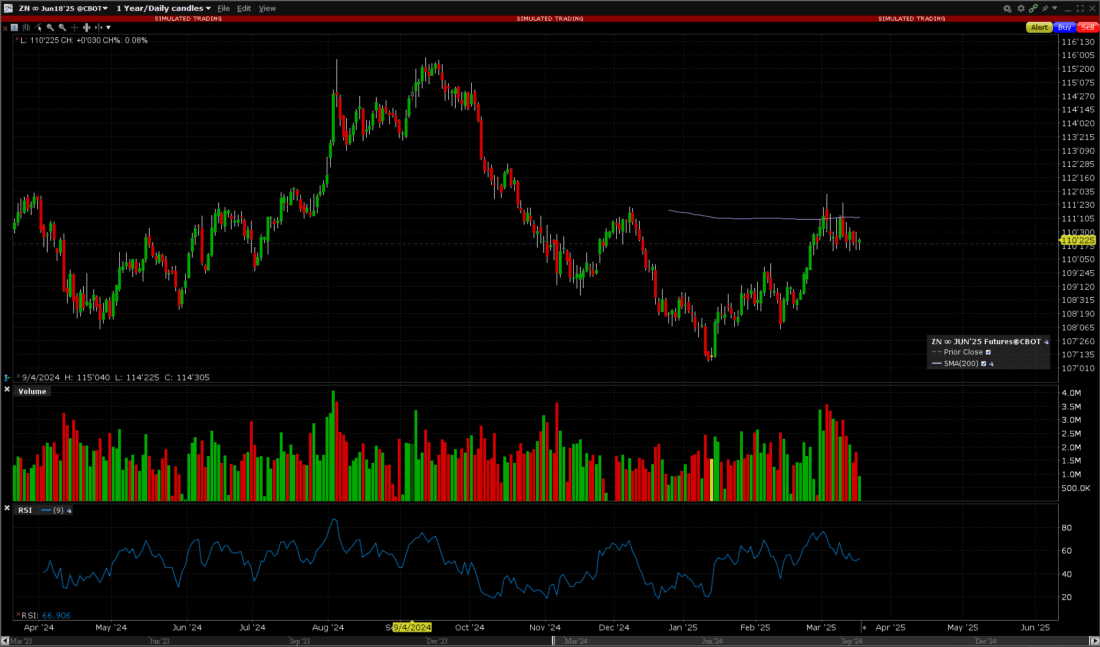

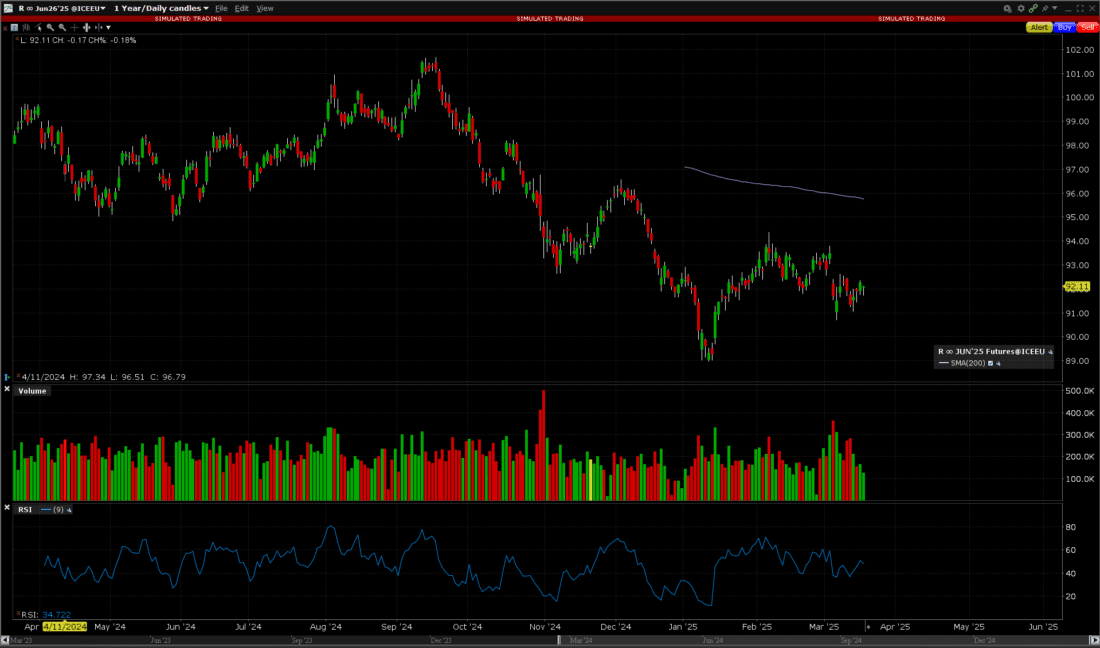

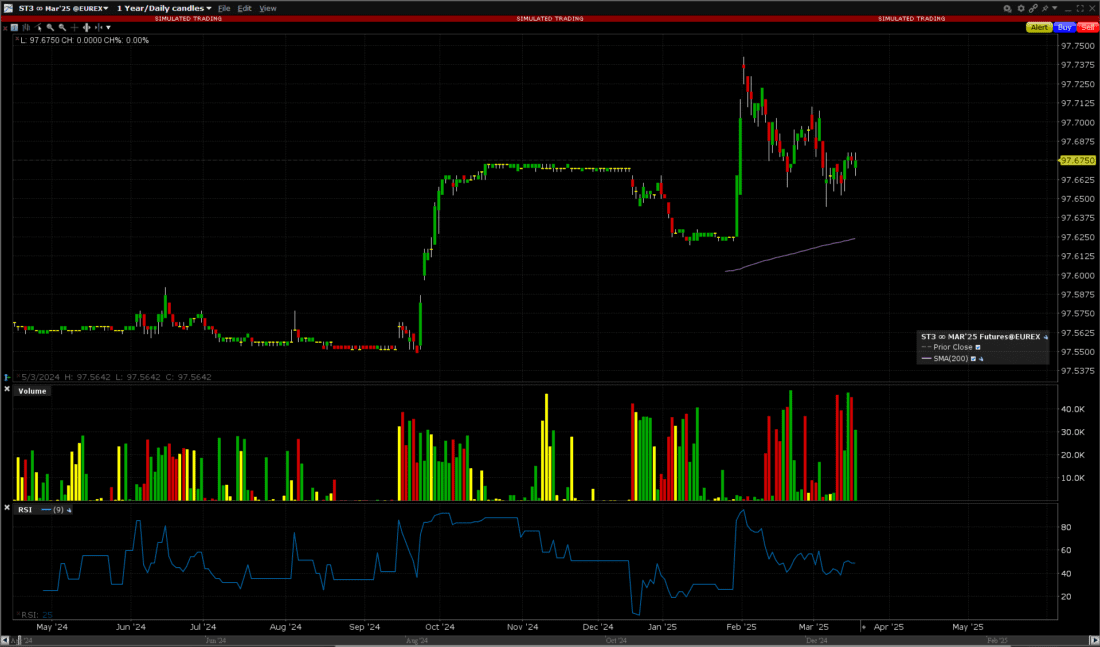

Futures traders are often characterized by their ability to trade on both sides of the market. That is, they are equally likely to buy or sell a futures contract. On the other hand, equity investors typically buy and hold and expect the stock market to rise over time. A yield curve trader tries to anticipate the developments within an economy and tries to predict the appropriate policy response. There are two types of products that offer futures traders access to economic and monetary policy. Those are Government Bond Futures and Short-Term Interest Rate Futures. These products can be used as a proxy for bonds of varying characteristics, such as quality, and maturity. They allow trading on future interest rate movements and may be used for both speculation and hedging. Fixed income futures provide an efficient way to manage interest rate exposure.

Interest rate futures deal with the short-end of a nation’s yield curve and typically have a 90-day duration. However, some contracts cover 30-day maturities. The three-month or 90-day contract is considered a benchmark across major G7 economies, since short-term lending is regularly refinanced at three-month intervals. And while these contracts have a short fixed-term duration, because they are futures contracts, they have maturity and expiration dates far off into the future. Such futures contracts enable investors to take a directional view on changes to the path for short-term interest rates in light of changing economic data.

Short-term interest rate contracts are a popular method for managing floating-rate exposure. That means that if an investor has an asset or liability that is not fixed, but pegged to market rates of interest, they could use interest rate futures contracts to hedge against adverse movements.

Although interest rate futures are most commonly used by sophisticated or institutional investors, retail investors can trade them too in order to express a view on developments in the economy or changing central bank views.

Interest rate futures are priced differently than other assets. They are expressed in terms of:

100 minus the rate of interest.

Such that if the three-month market rate of interest was 5 percent, then the three-month interest rate future would be priced at 100 minus 5.00 or 95.00. If the market senses that interest rates are likely to decline to 4.75 percent, futures prices would rise since 100 minus 4.75 = 95.25. Therefore, rising interest rates are synonymous with falling futures prices, while falling interest rates are associated with rising futures prices. Note earlier, the same holds true for bond prices where the inverse relationship with yields exists.

Holding a long futures position when market interest rates are falling should be profitable. Maintaining a short futures position when interest rates are rising should be profitable.

While outright long or outright short futures positions are most common, interest rate futures may be used to hedge exposure or speculate on a change in the shape of the yield curve. Remember that a normal yield curve is positively sloped, changes in actual policy or expectations about future policy movements can dramatically change the shape of the yield curve. For this to happen, prices of individual interest rate contracts must change at different paces. To capitalize on changes in the shape of the yield curve, traders can place curve steepening trades and curve flattening trades.

The mechanics here are very simple. The investor would take a position in a contract at a nearby expiration and take an opposing position in another at a further expiration.

For example, assume that the yield curve is currently normally sloped. The current rate of interest is 5 percent and in 12 months’ time is priced at 5.5 percent. The nearby futures price would be 95.00 and the deferred contract would be priced at 94.50. A trader projecting that the economy will slow and that the central bank will cut interest rates might place a curve flattening trade involving the sale of the nearby contract and the purchase of the deferred contract. The curve currently has a positive slope of 50 basis points.

Sell 1 December 2026 futures contract at 95.00.

Buy 1 December 2027 futures contract at 94.50.

Moving forward six months, the speculator was correct and the central bank cut interest rates by 25 basis points to 4.75 percent (95.25).

The December 2026 contract rose in price (as yields declined) to 95.25. Meanwhile, the December 2027 contract rose to 95.50 as the market priced in further declines in interest rates.

The December 2026 contract sold at 95.00 has risen to 95.25 incurring a 25-tick loss.

The December 2027 contract bought at 94.50 has risen to 95.50 incurring a 100-tick gain, for a net 75-tick gain. Not only did the anticipated yield curve flattening occur, but the curve became inverted by 25 basis points.

Investors can use short-term interest rate futures several years forward to manage risk and express views on the development of monetary policy. Outright long or short futures positions may be used as well as positioning along the yield curve.

Futures markets tend to be extremely liquid and provide an effective way to quickly hedge underlying exposure. Government bond futures contracts are available on exchanges worldwide to enable investors to target the specific part of the yield curve that they are exposed to in the world’s government bond market. Governments issue bonds or notes with varying maturities from one-month to 30-years. Each part of the yield curve has an equivalent bond or note future to enable government bond investors to quickly offset risk for as long as they need to.

Government bond futures markets tend to be highly liquid and can be used to offset risks for bonds of other quality. For example, investment grade bonds issued by Johnson & Johnson could be hedged almost perfectly with US government bond future of similar maturity.

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!