- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Lesson 2 of 4

Already an Interactive Brokers Client?

New to Interactive Brokers?

Our first lesson in this course focused on how central banks use monetary policy to control the price of money largely through the control of interest rates. Monetary policy impacts both the economy and multiple asset classes, but its impact is felt most directly in what is known as the fixed income or bond market.

Bonds are debt instruments sold by governments or companies with a promise to pay the principal back to investors at a specific end date in time. In return, investors buying such bonds commonly receive interest, usually twice per year, at a fixed and agreed upon rate from the issuer. The fixed rate is known as the coupon rate. And while the coupon rate is fixed, the price of the bond will fluctuate from day to day depending upon several factors, not least of which is the central bank’s determination of monetary policy.

The changing price of bonds results in changes to its yield. When bond prices increase, yields decline. When bond prices decline, yields rise. This is referred to as the inverse relationship between bond prices and bond yields.

Fixed income investing represents one of the fundamental building blocks of investment portfolios, providing regular income streams and relatively lower risk compared to stocks. Understanding how fixed income instruments work is crucial for retail investors seeking stable returns and managing portfolio risk.

As noted earlier, a central bank seeks to control the price of money, mainly due to the threat or impact of rising prices, known as inflation. Because inflation erodes the value of money, cash received today is worth more than money received in the future. This is often referred to as the Time Value of Money.

Accountants talk about how future cash flows must be discounted to their present value, which basically repeats what was stated above: Money today is worth more than it will be in the future. Hence, longer-term investments require higher returns to compensate for waiting. This is a key point when we look at the yield curve.

Yield Curve Fundamentals

A yield curve plots interest rates across different bond maturities. The plot explains the relationship between time and yield until maturity. The yield curve can change over time depending largely on two things. One, where the economy is in terms of the economic cycle. Two, where investors believe the central bank will set monetary policy. Typically, under normal circumstances, the yield curve or the cost of borrowing across different maturity dates through time, is positively sloped. We referred earlier to the concept of the Time Value of Money, stating that inflation erodes the value of money over time. A normal or upwardly sloping yield curve shows that the cost of borrowing is lower at shorter maturities and increases steadily through time.

The yield curve will change over time, largely influenced by both economic cycle and predictions for monetary policy. When investors feel that the central bank has finished tightening monetary policy and has concluded a set of interest rate increases, the yield curve becomes flat. The cost of borrowing is generally the same at short, medium and long-term maturities.

As investors project that the economy is slowing and inflation is under control, the shape of the yield curve shifts from positive or flat to become negatively shaped. This means that it costs more to borrow at shorter-term maturities than it does to borrow over longer-term periods. Another way of interpreting this is that investors fearful that the central bank will cut interest rates, will lend for as far out on the maturity curve as they can and lock into higher yields in anticipation of easier monetary policy. Negatively sloped yield curves are often referred to as predictors of imminent recession.

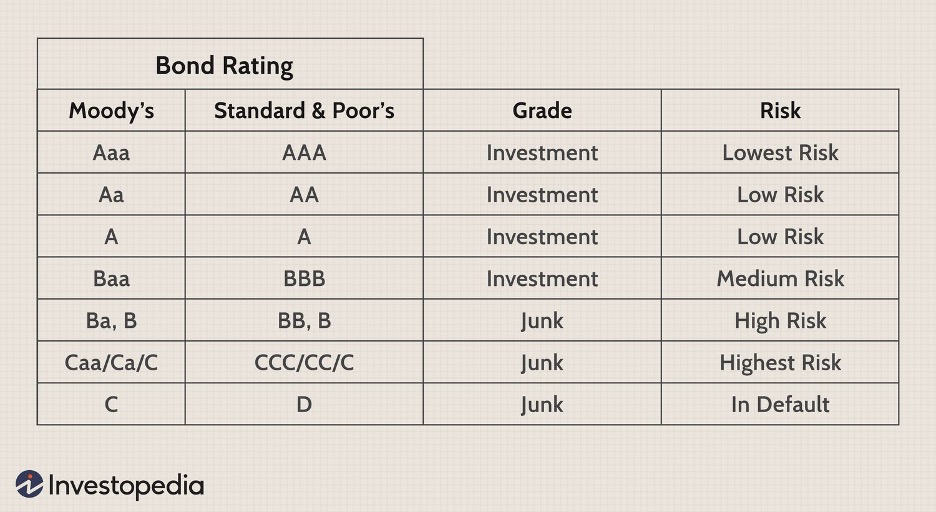

All bonds are not created equal. Remember that bonds represent debt issuance. From the perspective of the lender, investors are relatively sensitive to whom they are lending. Borrowers represent risk through their ability to repay the bond to lenders at maturity. Bigger corporations with a long history and strong balance sheet represent less risk than a company that was started two years ago, that might have little track record of growing revenues. In bond parlance, the newer company has higher credit risk. As such, there is a hierarchy amongst borrowers. Some are assigned a top rating, meaning that they are highly likely to repay their debts. At the other end of the scale are low rated companies with weaker financials, fewer revenues and potentially a poor history of paying good on their debts. Likewise, debt issued by the US government is deemed to be ultra-safe, while bonds issued by the government of Zimbabwe or Venezuela might be deemed much higher risk.

Bond ratings agencies are private companies, whose role it is to evaluate the risk of borrowers. Since they are private companies, they charge for this service, which has in the past led to suspicions of conflicting interests. After all, if a borrower wants to get a good rating, surely, they can pay the ratings agency. This is less of a concern nowadays following the Great Financial Crisis (2007/8).

Ratings agencies such as Moody’s and S&P evaluate the creditworthiness of companies by looking at financial records as well as the environment that the company operates in. Ratings reflect likelihood of repayment. Higher ratings indicate lower credit risk.

The ratings agencies establish a hierarchy of risk. It is assumed that the US government will always pay its debt obligations and is said to be Ultra-safe. Hence, US government issued Treasury debt is the benchmark for the so-called risk-free rate of return. Not much will trade below the commensurate US treasury curve, while levels of risk are marked increasingly lower on the ratings scale. Bonds fall into two broad categories of investment grade or non-investment grade.

Companies such as Johnson & Johnson and Microsoft are AAA credits. So-called Investment grade corporate bonds are rated BBB/Baa and higher by S&P.

Non-investment grade bonds are rated BB/Ba and lower.

What is of critical interest to a bond investor is the incremental compensation they can achieve by taking on higher levels of risk. Each rating level requires higher yields to compensate for increased risk.

The global bond market is huge. Many investors hold bonds for their perceived relative safety and ability to generate regular cash payments. How fast the economy is growing can influence the need for governments and companies to raise capital. Monetary policy greatly impacts the landscape in which the fixed income market lives. Demand for cash bonds can fluctuate depending on the stage of the economic cycle and the monetary policy stance of the central bank. Some bonds can be actively traded, while others may exhibit illiquidity, meaning that they rarely trade. In our next lesson we will examine the role of fixed income futures contracts that can be used to hedge underlying bond exposure or allow an investor to speculate on economic growth and anticipate the path of monetary policy.

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!