- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted February 19, 2026 at 8:51 am

The European Central Bank is designed to be technocratic and independent, insulated from the political cycles that shape the governments it serves. Yet the possibility that ECB President Christine Lagarde may step down before her term ends in October 2027 has thrust the bank into an unusually bright spotlight.

Even without confirmation from Frankfurt, the mere prospect of an early exit has opened a debate that reaches far beyond personnel: it touches on the future of central bank independence, the balance of power within the eurozone, and the direction of global monetary policy.

Lagarde has assured colleagues she’s focused on the job. Still, the ECB’s muted response stands in contrast to its sharp denials when similar rumors surfaced last year. That alone has been enough to set off a wave of speculation about what comes next.

The timing of Lagarde’s potential departure is not incidental. France heads into a pivotal presidential election in April 2027, and Germany faces its own shifting political landscape. If leaders more skeptical of EU institutions were to take power in either country, the appointment of the next ECB president could become contentious.

By stepping aside while President Emmanuel Macron and Chancellor Friedrich Merz remain in office, Lagarde would ensure that the selection process is handled by leaders broadly aligned with the ECB’s current direction.

But this logic cuts both ways. Critics argue that leaving early for political reasons — however well‑intentioned — could itself raise questions about the ECB’s independence. Modern central banks are designed to operate above electoral cycles, not around them. The debate echoes worries in the United States, where the White House has openly challenged the Fed policy and opened an investigation into outgoing chair Jerome Powell.

The early resignation of France’s central bank governor this month, enabling Macron to choose his successor, only adds to the sensitivity.

Choosing an ECB president is not a simple appointment. It is a multi‑layered negotiation involving national interests, regional balance, and the unwritten rules that have shaped the eurozone since its creation.

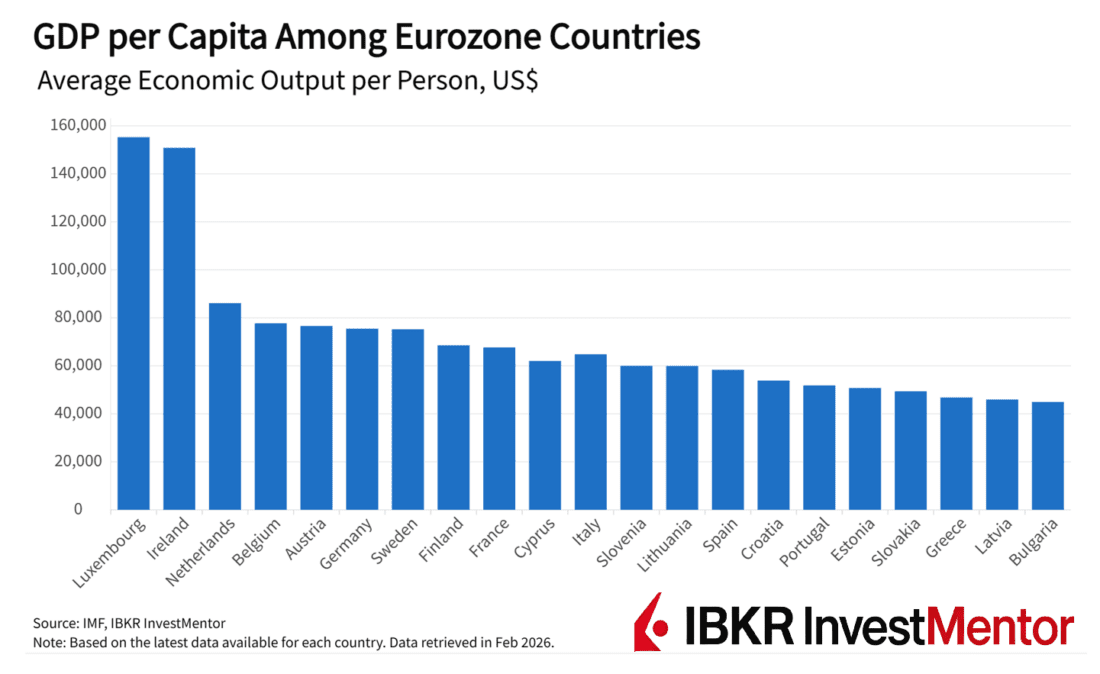

The basics are straightforward: the term is eight years, non‑renewable, and the candidate must be a national of a eurozone country. The European Council (made up of EU heads of state) proposes a name, the European Parliament issues a non‑binding opinion, and the Council formalizes the appointment. In practice, however, the process is a diplomatic exercise requiring alignment among 21 governments with different economic structures, political needs, and inflation profiles.

The ECB presidency signals how Europe manages diversity within a shared currency and how it balances influence among its members.

Germany, the eurozone’s largest economy, has never held the ECB presidency. That absence has served as a stabilizing compromise: allowing a German to lead the ECB in its early years risked reinforcing fears of Bundesbank dominance in the eurozone.

But the landscape has changed since the ECB was established in 1998. The central bank today is more consensus‑driven, more transparent, and less defined by national stereotypes. Berlin has abandoned its long-standing “debt brake” and is generally less rigid in its economic approach.

A German candidate could be harder to sideline this time around, even with the European Commission currently under German leadership (Ursula von der Leyen).

None of these candidates would represent a radical break. But each would bring a distinct tone to the institution, which matters a lot in central banking.

The ECB is not the only central bank facing transition. In the United States, Kevin Warsh is expected to take over the Federal Reserve, a figure long associated with a more hawkish stance — even though he’s most recently sided with the White House, advocating for rate cuts.

If the ECB also ends up with a leader inclined toward strict inflation control, global monetary policy could shift subtly but meaningfully.

“Hawkish” doesn’t have to mean aggressive rate hikes. It means placing price stability above growth support and preferring tighter financial conditions when uncertainty rises. Both Jerome Powell and Christine Lagarde oversaw significant rate rises as inflation surged after the pandemic. But Warsh, and some ECB contenders, have historically leaned further in that direction.

The next ECB president will inherit a landscape defined by competing pressures: Inflation has cooled, but fiscal policy is loosening across Europe. AI investment and surging defense spending are reshaping demand. At the same time, political volatility across Europe will test the ECB’s ability to remain above the fray.

If you want to learn more about central banks and their role in the global economy, download IBKR InvestMentor to gain access to free, interactive lessons and daily explainers.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR InvestMentor, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR InvestMentor and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!