- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted January 27, 2026 at 12:48 pm

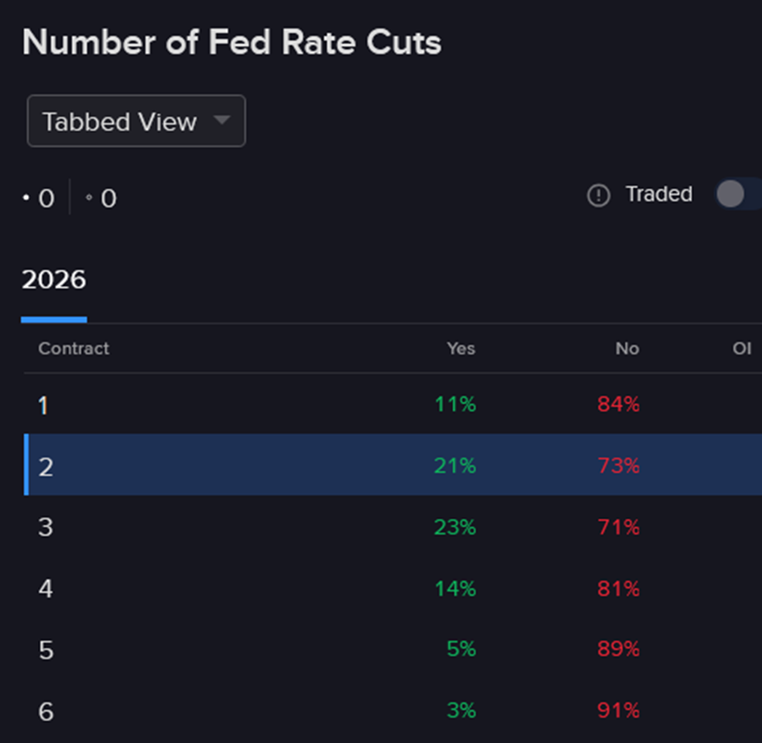

On the eve of tomorrow’s Fed decision, which is almost certainly going to feature a pause, the projected road ahead for additional accommodation is quite dovish. In 2026, prediction market participants believe that there are 21% and 23% chances of exactly two or three rate cuts by year end. Meanwhile, there’s an 11% likelihood of just one reduction and a 14% probability of four. Finally, when analyzing the odds for deeper drops in the central bank’s benchmark, prospects for precisely five or six cuts are at only 5% and 3%.

Meanwhile, tomorrow’s 99% chance of a Fed pause features uncertainty related to voting members formally dissenting against the central bank’s decision. Indeed, the probability of exactly one, two or three officials disagreeing with the verdict are at 46%, 41% and 10%, with Governor Stephen Miran, who supports much deeper cuts, sustaining the outlook for continued objections at current and future meetings.

Tomorrow’s Bank of Canada (BoC) decision is also expected to feature a pause with a 99% degree of certainty as monetary policy officials in Ottawa face similar conditions as their Washington counterparts. Indeed, persistent economic growth and above target inflation are keeping both institutions on hold this Wednesday, as they wait for risks of declining employment trends or accelerating cost pressures to respond via looser or tighter polices.

Source for images: ForecastEx

Note: Prices are highest bids as of the morning of Jan. 27, 2026.

To learn more about ForecastEx, view our Traders’ Academy video here

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Interactive Brokers LLC is a CFTC-registered Futures Commission Merchant and a clearing member and affiliate of ForecastEx LLC (“ForecastEx”). ForecastEx is a CFTC-registered Designated Contract Market and Derivatives Clearing Organization. Interactive Brokers LLC provides access to ForecastEx Forecast Contracts for eligible customers. Interactive Brokers LLC does not make recommendations with respect to any products available on its platform, including those offered by ForecastEx.

This is commentary on economic, political and/or market conditions within the meaning of CFTC Regulation 1.71, and is not meant provide sufficient information upon which to base a decision to enter into a derivatives transaction.

Related Articles

Hyperinflation here we come!