- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted September 4, 2025 at 12:45 pm

Tomorrow is the first Friday of the month, and thus the market’s eyes turn toward the monthly employment report. Bearing in mind the Federal Reserve’s dual mandate, there is reason to believe that this is the single most important set of data that we receive. It’s the best look at whether the goal of “maximum sustainable employment” is being met.

Although the Fed’s preferred price measure is Core PCE, there are myriad other sources of data that can shed light on “price stability” at their disposal. Besides CPI and PPI, various economic reports offer consistent insight into the level and growth of various input and output costs – including tomorrow’s Average Hourly Earnings and today’s Unit Labor Costs and ISM Service Prices Paid. That’s not to mention the relatively continuous data that commodity markets offer.

Conversely, while there are other labor measures, including yesterday’s JOLTS data and today’s ADP and Challenger reports, none of them are treated with the same degree of importance as the combination of Nonfarm Payrolls and the Unemployment Rate. Throw in the stunning revisions to the June and July numbers, and it is not unreasonable to assert the importance of tomorrow’s data.

We addressed the ramifications of the August employment report in a podcast we taped and released yesterday:

It’s about as big as it gets. Remember, the Fed is concerned with the dual mandate: stable prices and maximum sustainable employment. At Jackson Hole, Chairman Powell shifted his focus. Whereas before it was very much “tell me why rates should be cut,” it became “tell me why rates shouldn’t be cut.” It’s subtle, but the market of course loved it. ..Also, parenthetically, the likelihood of Fed cuts is actually below where it was before he spoke. A week before, Fed funds futures were pricing in about a 5–10% chance of a second rate cut — a 50-basis-point cut. By the way, ForecastEx, when I last looked yesterday, had about a 7% chance of a 50-basis-point cut as well. So I’d say our ForecastEx customers are maybe a little more enthused than those of the Chicago Mercantile Exchange.

As I type this, CME futures now show a 98% chance for a 25 basis point cut at the September 17th meeting. The IBKR ForecastTrader shows a more diffuse set of opinions, with “Yes” bids of 12% for “No Change”, 82% for “Lower 25bps”, and 5% for “Lower 50bps or more”. Regardless of your metric, it would seemingly require a true shock for expectations for something other than a 25bp cut to enter the market discussion. That said, we had that sort of surprise last month – one that likely spurred Powell’s changed bias toward cutting.

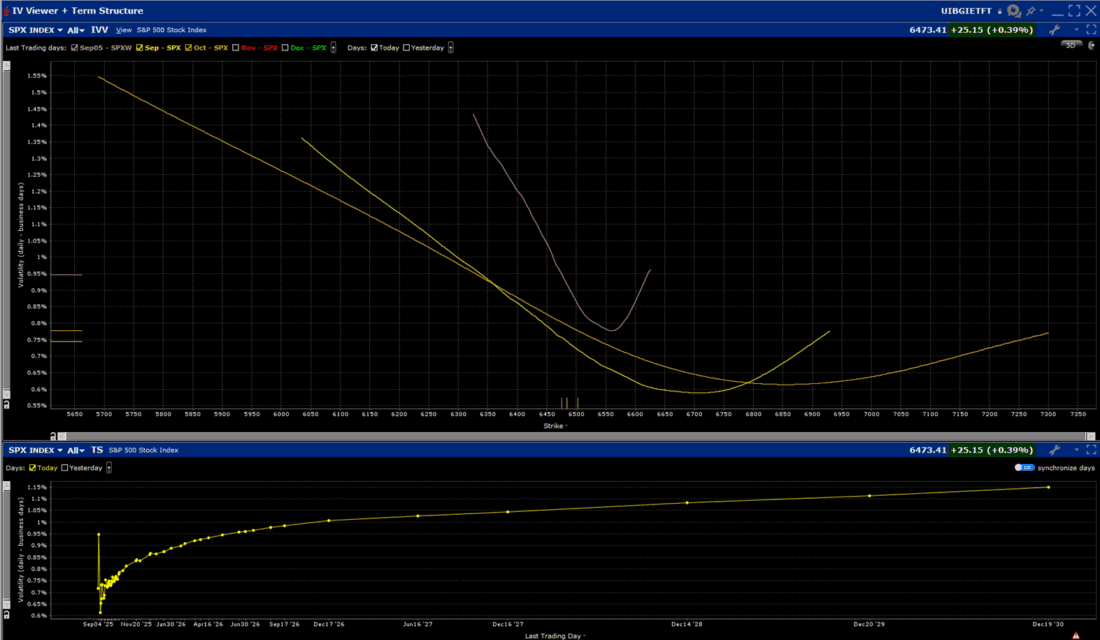

Options on the S&P 500 (SPX) are understandably pricing in a bit of extra risk aversion, but nothing too extreme. The charts below show that at-money SPX options expiring tomorrow are pricing in a move of 0.95% between now and tomorrow’s close, above the 0.75% average daily move that is priced into options expiring September 19th (the quarterly expiration two days after the next FOMC meeting). We see a steep skew in the near-dated options, indicating the demand for downside hedges:

Source: Interactive Brokers

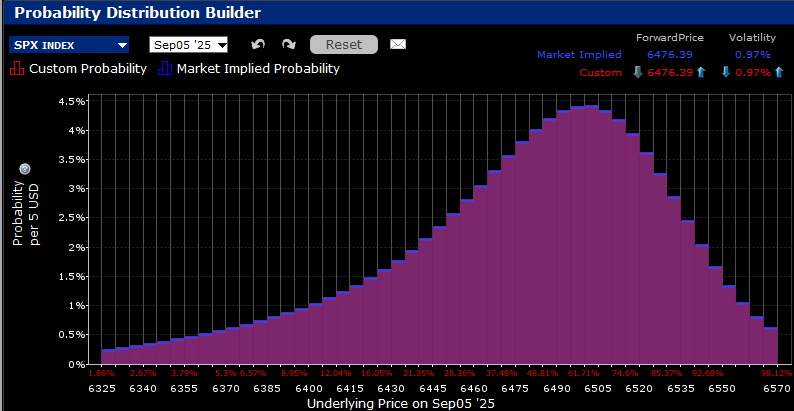

But the risk aversion only goes so far. As is now typical, we see options pricing in a higher likelihood of a higher close tomorrow, with a peak probability in the 6500-6505 region, about 0.4% above the current index level.

Many investors are clearly hoping for rate cuts, but it is important to remember to be careful what we wish for. Data that show a gently decelerating but not dire labor market would suit that goal. Plunging data might bias the Fed to further cuts, but could also raise concerns that the central bank is too far behind the curve. The former extends the “Goldilocks” narrative; the latter raises concerns about stagnation or stagflation. Equity investors should always opt for a better economy.

New to Interactive Brokers?

Open AccountAlready an Interactive Brokers Client?

Request Trading PermissionThe analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Options involve risk and are not suitable for all investors. For information on the uses and risks of options, you can obtain a copy of the Options Clearing Corporation risk disclosure document titled Characteristics and Risks of Standardized Options by going to the following link ibkr.com/occ. Multiple leg strategies, including spreads, will incur multiple transaction costs.

The projections or other information generated by the Probability Lab tool regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results and are not guarantees of future results. Please note that results may vary with use of the tool over time.

Related Articles

")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!