- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted July 24, 2023 at 10:45 am

Within the Singapore stock market, Sembcorp Industries and Seatrium have booked the most net institutional fund inflows in the year to Jul 18.

Both stocks have been associated with pivots to sustainable infrastructure and have also ranked among Singapore’s most traded stocks over the period.

Seatrium has been Singapore’s sixth most traded stock, while Sembcorp Industries has ranked among the 15 most traded stocks, up from ranking among the 30 most traded stocks in 2022.

The next two stocks that have seen the next highest net institutional inflow, Genting Singapore and Singapore Airlines (SIA), have been associated with the new value the globe has put on travel and leisure following Covid, with SIA ranking as Singapore’s fifth most traded stock so far this year and Genting Singapore keeping its place among the 10 most actively traded.

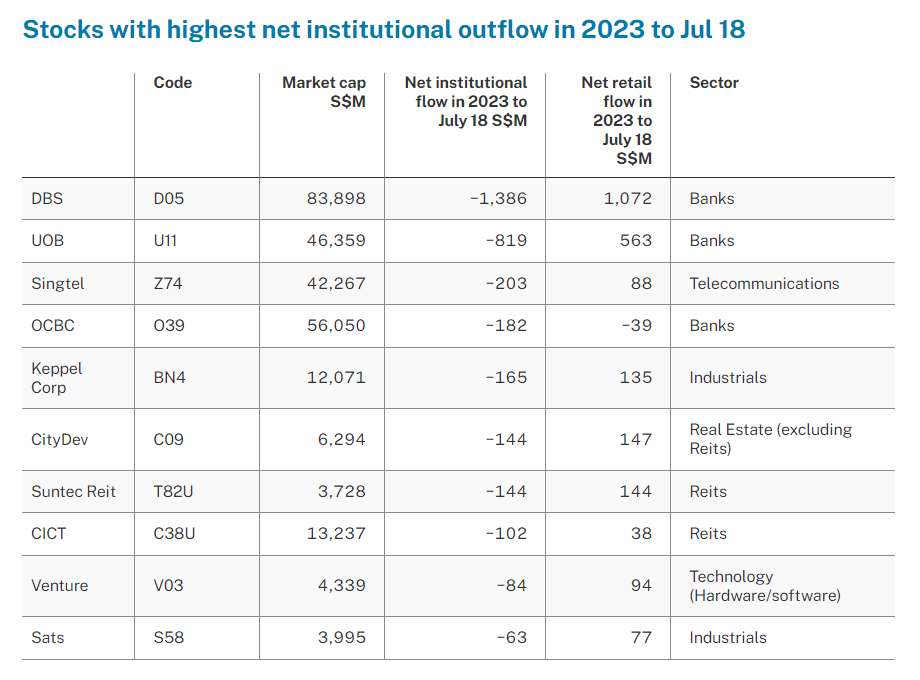

At the same time, stocks that have booked the highest net institutional outflow included DBS, UOB, Singtel, OCBC and Keppel Corporation.

Overall, Singapore Exchange-listed stocks have booked S$2.8 billion of net institutional fund outflow and S$1.4 billion of net retail inflow in the 2023 year to Jul 18.

By comparison, the same period in 2022 saw around S$200 million of net institutional outflow and S$1.1 billion of net retail inflow.

This indicative flow has been aggregated at an account level for both retail and institutional participants. The net amounts are derived from subtracting the total sell amount from the total buy amount for each of the institutional fund and retail fund segments.

The fund flow does not include net buying and net selling by market makers and active traders. Rather, this segment of flow bridges the difference between net institutional and net retail fund flow.

While S$2.8 billion of net institutional fund outflow and S$1.4 billion of net retail inflow might insinuate that stocks were mostly net sold by institutions, with maybe half as many stocks net bought by retail investors, these dollar amounts should also be measured against the size of the stocks to give an idea of the subsequent scale of the flow.

Stocks that lead the inflow and outflow tallies are typically those that maintain larger market capitalisation, in addition to daily turnover.

For instance, DBS and UOB, which rank as the largest and third-largest stock by market capitalisation in the Singapore market, have, as noted above, drawn the highest net institutional fund outflow and highest net retail inflow in the year to Jul 18.

While DBS has booked S$1.4 billion of net institutional fund outflow, this represented some 1.7 per cent of its market capitalisation on Jul 18.

Similarly, the S$819 million of net institutional outflow booked by UOB represented 1.8 per cent of its market capitalisation on Jul 18.

On a sector market-capitalisation-weighted basis, banks and real estate investment trusts (Reits) led the net institutional outflow for the year to Jul 18, with the trio of banks seeing combined net institutional outflow at 1.3 per cent of their combined market capitalisation, and Reits seeing net institutional outflow at 0.5 per cent of their combined market capitalisation.

As many as 30 of the 40 trusts in the Singapore Reit sector booked net institutional outflow.

US office Reits Prime US Reit and Manulife US Reit booked the highest net institutional outflow proportionate to their respective Jul 18 market capitalisations.

This has coincided with continued weakening of occupancy performance across the United States office market due to a slowdown in demand and leasing activity, as Manulife US Reit noted recently.

On a sector market-capitalisation-weighted basis, the sectors that saw the highest net institutional inflow proportionate to their market capitalisations were utilities, energy/oil & gas, and then consumer cyclicals.

All in all, the net institutional flow in the year to Jul 18, represented 0.3 per cent of the total market capitalisation of the Singapore stock market as at Jul 18, while the net retail inflow represented less than 0.2 per cent.

There were also multiple stocks that booked both net institutional inflow and net retail inflow for the year to Jul 18, which included four actively traded stocks: ESR-Logos Reit, CapitaLand China Trust, Nio and Emperador, that together averaged a 0.9 per cent decline in total returns over the period.

When comparing flow and returns, investors must be mindful not to interpret net fund flow as stock performance indicators, just as much as past performance has no bearing on future returns of a stock.

Fund flow simply indicates how investor genres such as institutions and retail investors are moving funds.

There can be a myriad of strategies applied by portfolio managers to achieve returns and attempt to mitigate market risks, including portfolio balancing techniques.

These techniques could see such an institution turn from being a net buyer to a net seller of a stock, sector, or country index because of its comparative outperformance to the rest of the portfolio. Such rebalancing can be a part of the typical processes that shape portfolios; thus, context matters.

For instance, as discussed above, DBS and UOB have booked a combined S$2.2 billion of net institutional outflow in the year to Jul 18.

As an educative example, earlier this year an investor may have anticipated interest rates were near highs and thus reduced previous overweight exposure to banks.

In addition, some outperformance in Singapore in 2022 saw both DBS and UOB average 9 per cent total returns even as Asia-Pacific banks generated average declines in the vicinity of 2 per cent.

This context could indicate that portfolio rebalancing could have been a contributing factor to the net institutional outflow.

Similarly, currency moves may also prompt rebalancing. From the end of 2022 through to Jul 18, 2023, for instance, a Singapore dollar (SGD) appreciation saw the USD/SGD fall from 1.340 to 1.323, which may have impacted the size of the net institutional outflow for the period.

By comparison, SGD depreciation, with the USD/SGD rising from 1.349 to 1.396 for the first 28 weeks of 2022 may have resulted in significantly less net institutional outflows.

Significant corporate actions can also impact the flow.

For instance, coinciding with the completion of the combination of Sembcorp Marine and Keppel Offshore & Marine in February, the first two months of 2023 had seen Keppel Corporation book S$188 million of net institutional fund outflow, while Seatrium, then Sembcorp Marine, booked S$46 million of net institutional fund inflow.

SGX fund flow data is published each Tuesday in The Business Times and on the SGX website.

—

Originally Posted July 24, 2023 – Taking stock of institutional and retail fund flows

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Singapore Exchange and is being posted with its permission. The views expressed in this material are solely those of the author and/or Singapore Exchange and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Alternative investments can be highly illiquid, are speculative and may not be suitable for all investors. Investing in Alternative investments is only intended for experienced and sophisticated investors who have a high risk tolerance. Investors should carefully review and consider potential risks before investing. Significant risks may include but are not limited to the loss of all or a portion of an investment due to leverage; lack of liquidity; volatility of returns; restrictions on transferring of interests in a fund; lower diversification; complex tax structures; reduced regulation and higher fees.

Related Articles

")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!