- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted April 3, 2024 at 11:00 am

One of investors’ favorite stocks has been underperforming the S&P 500 for several weeks lately, falling from $200 to $170 during that time frame. I could of course be referring to Tesla (TSLA) – especially after yesterday’s disappointing deliveries – but the description also fits for Apple (AAPL).

Let me preface today’s piece by acknowledging that I am a fairly loyal and happy AAPL customer. I’m typing this on a MacBook Pro while monitoring markets on an iMac, and my iPhone is an all-too-constant companion. But my enthusiasm for the company’s products should not cloud my judgement about AAPL as an investment.

One of the first investing lessons that I learned was that great companies don’t always make great stocks. While AAPL has indeed been a great stock for most of its existence, it has been a bit of a laggard recently. On a year-to-date basis, AAPL is down a bit more than -11% even as the S&P 500 rose by just under +10%. On a one-year basis, that divergence is even more stark. AAPL is up about +3.5% while SPX rose more than 27%. There’s nothing wrong with a stock that is up 3.5% in a year, but the underperformance compared to an index in which AAPL is the second-largest component is quite stark. (AAPL is currently 5.6% of SPX weight, trailing only Microsoft’s (MSFT) 7.15% and followed closely by Nvidia’s (NVDA) 5.04%)

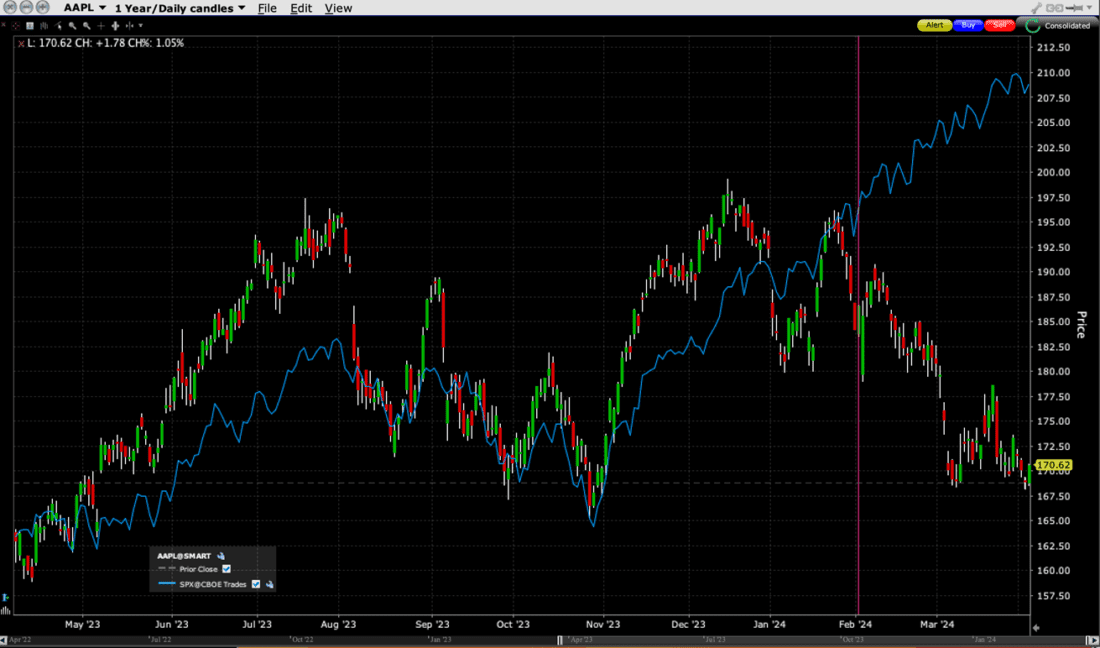

That said, a cursory glance of the one-year chart below shows that the bulk of AAPL’s underperformance has been relatively recent. The decline started just before the company’s most recent (Q1 FY 2024) earnings report on February 1st, and after a brief post-earnings recovery, the declines become more sustained.

1-Year Chart AAPL (red/green daily candles) vs. SPX (blue line), with vertical line on February 1st, 2024

Source: Interactive Brokers

My opinion about AAPL’s dubious role as a premier growth stock began to shift after the prior report (4Q FY 2023) on November 2nd. That of course proved to be premature considering AAPL’s role in the furious, “Magnificent 7”-powered year-end rally, but it appears that the market is coming around to that viewpoint. On November 3rd, in a report entitled “Yay, Fewer Jobs – Plus, When the Biggest Growth Stock Doesn’t Grow”, we wrote:

The current restrictive monetary conditions have led investors to favor companies with stable earnings and cash flows, and hence less need to borrow at high rates. The poster child for that type of company is Apple (AAPL), which is one of the few high-profile stocks that are trading lower today. Although AAPL reported EPS of $1.46, above the $1.39 consensus, concerns about sales in China weighed on investor perceptions. But for AAPL, investors should be concerned about sales overall. Although total revenues rose sequentially, breaking a three-quarter downtrend, this was the fourth quarter in a row when revenues fell on a year-over-year basis.

Quite frankly, it is hard to reckon with a growth stock whose sales aren’t growing. AAPL is a cash-generating machine, with over $20 billion in positive cash flow every quarter. That has led to a cash hoard of over $160bn. With short-term rates at 5%, that can be a significant contributor to the company’s bottom line, but investors aren’t paying 28X earnings for a company with no revenue growth and only modest EPS growth. AAPL earned $6.13 per share in 2023 (it’s fiscal year just ended); it earned $6.11 in 2022. Is that a growth stock? It will take some time for the market to decide whether to reclassify AAPL as a value stock. But I’ve come to think of it as almost a utility – I shell out a few dollars each month for iCloud and Apple TV, and many more dollars every few years to upgrade my iPhone. AAPL is far less boring than a typical utility stock – and far less regulated. But a re-rating of the stock with the largest market capitalization would be an existential drag on the indices that AAPL sits atop.

OK, that last line was a clunker. SPX has done just fine, thank you, even as AAPL sank. But I do think that the broader thrust of those paragraphs ultimately has proven largely correct. Since that report was published, I have been publicly questioning whether AAPL is properly considered a growth stock and whether it should instead be considered a value stock.

There is nothing wrong with being a value stock, by the way. Although growth has trounced value in recent months, the outperformance has been less pronounced recently. The declines in AAPL and TSLA, along with a broadening of the rally, likely have something to do with it. On a year-to-date basis, the S&P 500 Growth Index (SGX) is up 10.77% while the Value counterpart (SVX) is up 6.05%. If we think that the rally will continue to broaden, or instead that equities will trend sideways or down, particularly after the “sell in May” period, then value stocks – especially those with dividends that are supported by solid cash flows, like AAPL – should provide some ballast to a volatile portfolio.

But the process for AAPL being considered value, not growth, is incomplete. It still trades at a premium to SPX, with a P/E of 26.55 vs. the index’s 23.33. That 26.55 level is now well below that of SGX’s 32.33, but still well above SVX’s 17.47. Right now, broadly speaking, AAPL is trading like a proxy for the broad market. If that changes, and AAPL becomes more of a leading value stock, it still has some underperformance ahead of it.

New to Interactive Brokers?

Open AccountAlready an Interactive Brokers Client?

Request Trading PermissionThe analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

Apple has been my largest position for a long time; I have own a stake in it for most of the time since the late 80’s. Like any investment, it fluctuates, but mostly it has gone up. But there has been some periods of time when they lost their way. Although I have always found their operating system easier to use, I sold out of my original position because I thought they were severely restricting themselves by not allowing outside developers to have access, and so their market share would remain small. Later I sold out when they fired Jobs and continued to flounder, but I bought my largest stake when I saw early on the ubiquity of the I Phone. In one account I have held the shares for the last eleven and a half years. Those shares have increased nearly eight times. In another account, I’ve held the shares for almost three and a half years; those shares have only increased 52%. While clearly, the return hasn’t been as good recently, I am not dissatisfied with the second return.

I will continue to write covered calls; at times that will lead me to being assigned. If my position wasn’t so large, I might consider selling some puts now, but as I said my investment is already outsized compared to the rest of my portfolio, The point here is Apple’s problems are not like Boeing’s. The company’s culture is not in question. I can wait for them to develop the next big product/service, and in the meantime sell some more calls.

I am unsure if I should sell or sit on it. Your comment is not very encouraging. I already have investments in value, I need growth.