- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted August 28, 2024 at 12:00 pm

The long-awaited day is upon us. After much ink (more likely, pixels) has been spilled on the topic of Nvidia (NVDA) earnings, we will finally learn the results after today’s close. It bothers me to think that one company’s results are perceived as being consequential for the equity market’s performance on the whole, but in this case it is not an exaggeration.

In yesterday’s piece, we outlined the ways that NVDA influences a wide range of other key stocks and sectors beyond semiconductors. We won’t belabor them again today – read this linked article instead – but suffice to say that when artificial intelligence remains the dominant market theme and the other six Magnificent Seven stocks are among its largest customers, we feel comfortable continuing to assert that NVDA is the market’s Atlas, hoisting whole indices upon its broad shoulders.

The question before us is not whether NVDA will report good results. Even a subpar quarter from NVDA would be considered amazing for almost any other company. We’ve gotten spoiled by their unprecedented ability to beat on the top and bottom lines, raise guidance, then do it all again next quarter. The question before us is less about whether they will meet expectations but instead how much they will raise guidance going forward, and whether there is a “whisper number” that exceeds even the published expectations. The recent rally increases the likelihood of heightened expectations being priced in. Below is a helpful “cheat sheet” for interpreting this afternoon’s results (though it is impossible to quantify the potential impact of comments about the new Blackwell chip) :

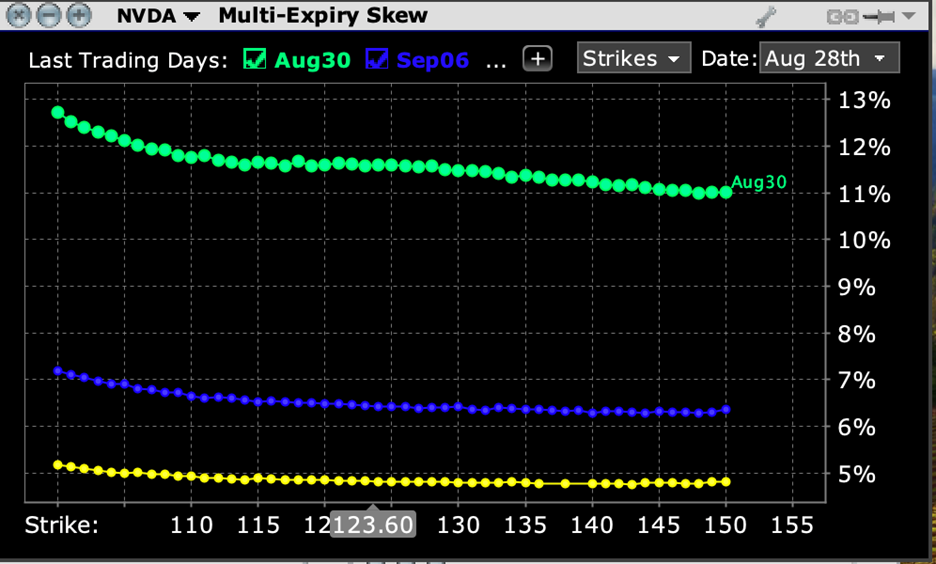

So, what might the options market be telling us about the potential post-earnings moves for NVDA? Bearing in mind that the last four of the last six post-earnings moves have exceeded 9% (+9.32%, +16.4%, -2.46%, +0.1%, +24.37%, 14.02%), it is hardly unreasonable to see that at-money options expiring this week are currently pricing in over 10% daily moves between now and Friday:

NVDA Skews for Options Expiring August 30th (green), September 6th (blue), September 20th (yellow)

Source: Interactive Brokers

Unlike before previous quarters, when skews were essentially flat, we do see a bit of a downside bias for options roughly +/- 20% from current levels. The skew steepens dramatically below $100, but that might be the result of NVDA’s recent flirtation with that key level:

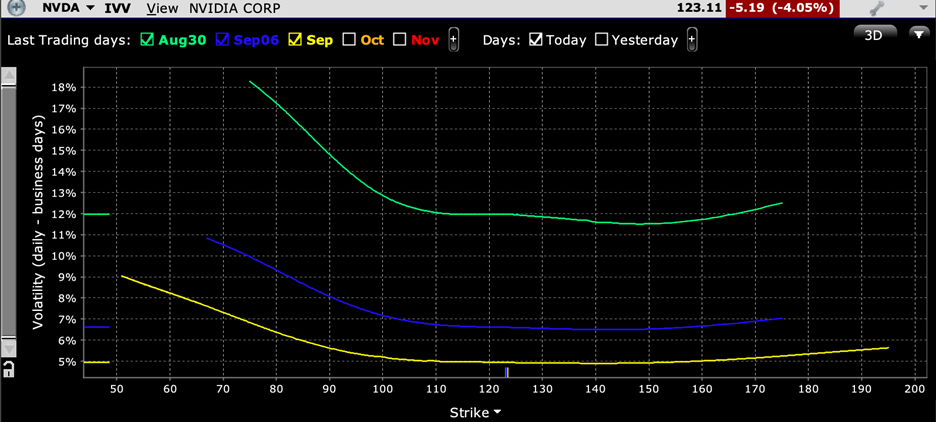

NVDA Skews for Options Expiring August 30th (green), September 6th (blue), September 20th (yellow)

Source: Interactive Brokers

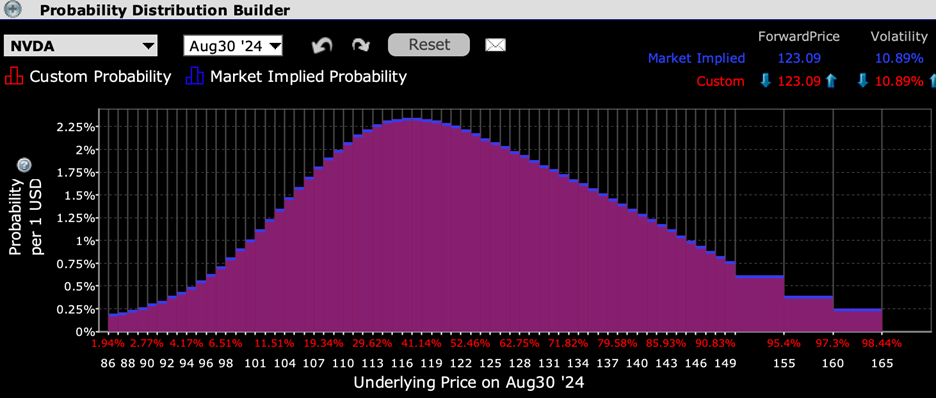

The IBKR Probability Lab also shows some modest risk aversion, with a peak outcome shown around $117.50, about 4.5% below current levels:

Source: Interactive Brokers

Both NVDA and broad indices and have sold off a bit since I started writing this piece. It is not unreasonable to think that at least some of that reflects a bit of concern ahead of today’s earnings report. Paradoxically, the more we sell off today, that might be a good thing for tomorrow. It is not necessarily a bad thing when people show some healthy risk aversion ahead of a potentially market-moving event – they’re less likely to get blindsided. Frankly, it’s a lot scarier when people are truly sanguine. That said, there was a considerable amount of good news priced in when the stock rallied from $100 to $125 in just three weeks. We’ll find out soon enough whether that was appropriate.

New to Interactive Brokers?

Open AccountAlready an Interactive Brokers Client?

Request Trading PermissionThe analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

The projections or other information generated by the Probability Lab tool regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results and are not guarantees of future results. Please note that results may vary with use of the tool over time.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

Now what is a reasonable strike price to sell covered calls?