- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted July 25, 2024 at 10:00 am

2024 is a transitional year for political cycles in many countries and regions, with elections taking place across Europe, the US and India. The first week of July started with landmark elections in two major economies, the UK and France. The UK election resulted in a widely expected landslide victory for Kier Starmer’s Labour party. In France, on the other hand, the second-round election for the National Assembly resulted in a surprising turn from the first round, delivering what looks like a hung parliament, with the left-wing alliance Nouveau Front Populaire (NFP) winning 182 of the 577 seats, followed by Macron’s centrist coalition winning 168 seats.

Markets seemed to react more favorably to the French election results, with the Cboe France 40 Index rising over 1% in its first two hours of trading on Monday 8 July, the morning after the French election, likely reflecting relief that no single party secured a majority as was widely expected. By contrast, the Cboe UK 100 Index traded roughly flat through the UK election, likely because the results of the UK election were much closer to expectations.

In this article, we consider two option strategies for traders looking to profit from a specific view of how these elections might impact a fictional French stock: Le Boulanger Paresseux SA, with the ticker “LBP”. We will assume that LBP is currently trading at exactly €100 per share, and no dividends are expected to be paid between now and option expiry, and that the trader expects LBP to trade sideways over the next several months, neither rising nor falling significantly. In other words, the goal here will be to try and profit from gridlock between buyers or sellers, where the trader makes money even if the stock doesn’t go up or down. Each of these strategies involve combining multiple options and show how targeted you can get with your options strategy both on the upside and the downside.

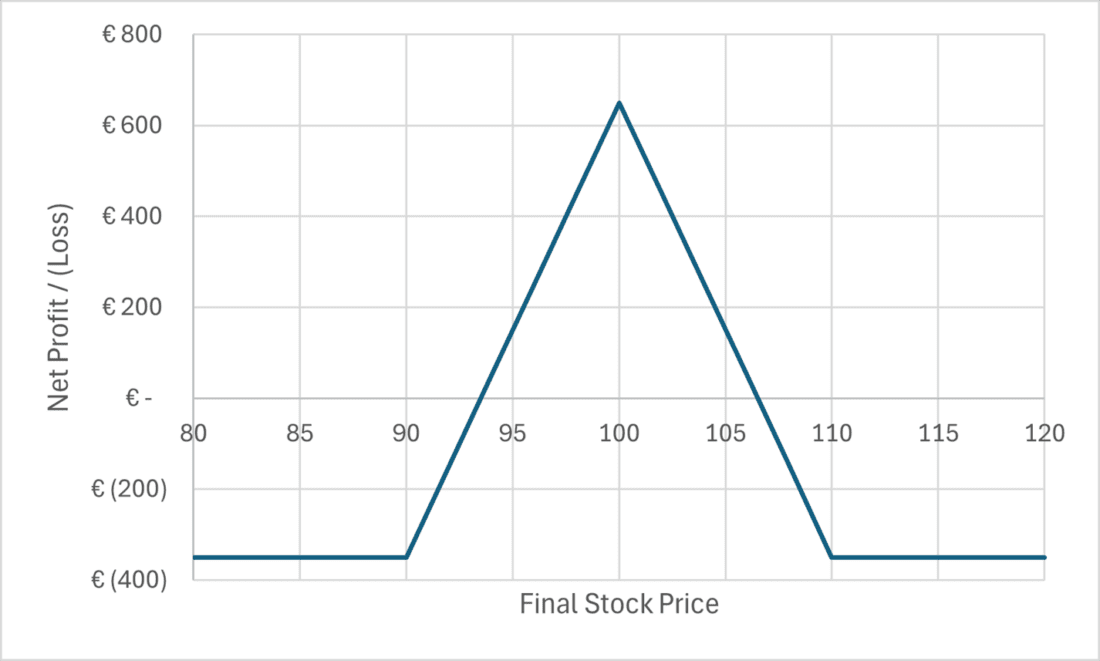

The first strategy we will consider is called a “butterfly”, so named because of the profit and loss chart might be compared to a picture of a butterfly flapping its wings. Here, the trader needs to choose an expiration date, and then a price expected to be the most likely level at which LBP can be expected to close on that expiration date. This strategy earns a maximum profit if LBP happens to close at exactly that target price on the exact expiration date, with gradually reduced payouts the further away the stock finishes from this target until the maximum loss of the whole premium paid for this option strategy. As an example based on LBP’s initial price of €100 per share, we put together the butterfly with the following three option positions:

1. We buy one 90 strike call, and

2. We selling two 100 strike calls, and

3. We buy one 110 strike call

This option combination could also be seen as a pair of call spreads: we buy a 90-100 call spread, and then we sell a 100-110 call spread. Based on a few similar examples, we assume the total net cost of these three options to be around 3.50 per share, or a total of €350 per round lot of 100 shares of LBP. The sum of the payouts of these options at expiry, based on the final closing price of LBP on that expiry date, would be as follows:

A. If LBP finishes below 90, all three options expire worthless and the trader loses the €350 premium, or

B. If LBP finishes between 90 and 100, the long 90 strike call option pays out €100 per point that LBP finishes above 90, and the 100 and 110 strike calls both expire worthless. For example, if LBP finishes at 92, the option pays out €200, which would be a net loss of €150 versus the €350 paid for the option position, while if LBP finishes at 98, the option payout would be €800, or a €450 gain over what was paid for the option. The maximum payout of this option position would be €1,000, in the case that LBP finishes at exactly 100, or

C. If LBP finishes between 100 and 110, then the short position in the 2x 100 strike calls would start eating into the payoff value of the 1x 90 strike option we are long. For example, if LBP finishes at 108, then the long 90 strike call would be worth €1,800, but the short 2x 100 strike options would require paying back 2x€800 = €1,600 for a net payout of €200, which would be a net loss of €150 versus the €350 paid for the option position. On the other hand, if LBP finishes at 102, the net option payout would add up to €800, or a €450 gain over what was paid for the option, or

D. If LBP finishes above 110, then the gains from the long 90 strike option would be exactly cancelled out by the other three options, leaving a net loss of the €350 up-front premium paid of this option combination.

The net profit and loss of this strategy, based on the final price of LBP, is charted in this next diagram which is described as the “butterfly”:

Past performance is not indicative of future results

Overall, this strategy makes the most sense for a trader who expects LBP to finish the term of these options within the “breakeven” range of 93.5 to 106.5, the range within which the final value of the options is worth more than the €350 premium paid up-front for the options. Of course, traders who instead expect that LBP will NOT finish within this range might consider putting on the opposite trade, where the €350 premium would be received up front and kept if LBP finishes below 90 or above 110, with the risk of having to pay out as much as €1,000 if LBP finishes at exactly 100. One disadvantage some traders see in this strategy is that the maximum payout is concentrated at a single point, and so a related strategy called the “Iron Condor” spreads out this maximum payout over a wider range.

The second strategy we will illustrate here is one whose name also conjures up images of a creature flying with wings, is called the “Iron Condor”, and differs from the butterfly primarily in spreading out the maximum payoff from a single point to a range. Although this requires putting together four distinct options contracts, all four of these options have the same expiry date, and are related in ways that make their overall exposure quite easy to understand, as we will see later:

1. We buy one 90 strike call, and

2. We sell one 95 strike call, and

3. We sell one 105 strike call, and

4. We buy one 110 strike call

As with the butterfly, this can also be seen as a pair of call spreads: we buy a 90-95 call spread, and then we sell a 105-110 call spread, with the difference from the butterfly being the gap between the two call spreads. Based on a few similar examples, we can assume the total net cost of these four options to be around 2.25 per share, or a total of €225 per round lot of 100 LBP shares. The sum of the payouts of these options at expiry, based on the final closing price of LBP on that expiry date, would be as follows:

A. If LBP finishes below 90, all four options expire worthless and the trader loses the €225 premium, or

B. If LBP finishes between 90 and 95, the long 90 strike call option pays out €100 per point that LBP finishes above 90, and the 95, 105 and 110 strike calls all expire worthless. For example, if LBP finishes at 92, the option pays out €200, which would be a net loss of €25 versus the €225 paid for the option position, while if LBP finishes at 94, the option payout would be €400, or a €175 gain over what was paid for the option, or

C. If LBP finishes between 95 and 105, then the lower 90-95 call spread pays it its maximum €500 value, while the upper 105-110 call spread expires worthless. This is the maximum profit of this strategy, where the €500 represents a net gain of €275 over the €225 premium paid, or

D. If LBP finishes between 105 and 110, then the short position in the 105 strike call would start eating into the payoff value of the long 90-95 call spread. For example, if LBP finishes at 106, the total final value of the options would be €400, versus €100 if LBP finishes at 109, representing a net profit of €175 or net loss of €125 respectively, or

E. If LBP finishes above 110, then the gains from the long 90-95 call spread would be exactly offset by the loss from the 105-110 call spread, leaving a net loss of the €225 up-front premium paid of this option combination.

The profit vs loss on this strategy, based on the final price of LBP, is charted below:

Past performance is not indicative of future results

In other words, although this strategy does require trading four distinct options contracts, the Iron Condor does have the advantage of having a lower up-front premium and a wider range of maximum payout outcomes than the butterfly. As with the butterfly, a trader expecting LBP to finish outside this range may also consider taking the opposite position, where the €225 premium is received up front in exchange for taking the risk of having to payout €500 if LBP finishes between 95 and 105.

Even if you expect political gridlock to result in market gridlock, where stocks trade sideways with no clear trend up or down, the butterfly and iron condor strategies explained in this article are just two ways you can use options to more precisely target profits in your chosen range of outcomes.

—

Originally Posted July 18, 2024 – Option Strategies for 2024 Elections

Disclaimers

·The above is the product of external market analysis commissioned on behalf of Cboe Europe B.V. The views expressed herein are those of the author and do not necessarily reflect the views of Cboe Europe B.V., Cboe Global Markets, Inc. or any of its affiliates (‘Cboe’). For more information on how this research was conducted and/or the author please contact EUDerivatives@cboe.com

·The information provided is for general education and information purposes only. No statement provided should be construed as a recommendation to buy or sell a security, future, financial instrument, investment fund, or other investment product (collectively, a “financial product”), or to provide investment advice.

·Cboe does not select the financial product for you to transact. Your financial adviser, broker, or other financial services professional may select the financial product for you to transact and you should speak with your financial advisor, broker or professional, as applicable, regarding any such selection.

·Hypothetical scenarios are provided for illustrative purposes only. The actual performance of financial products can differ significantly from the performance of a hypothetical scenario due to execution timing, market disruptions, lack of liquidity, brokerage expenses, transaction costs, tax consequences, and other considerations that may not be applicable to the hypothetical scenario.

·Trading in options and options strategies can be complex and recommended for sophisticated investors with the appropriate level of knowledge and expertise in these transactions

·The content of this article should not be construed as an endorsement or an indication by Cboe of the value of any non-Cboe financial product or service described.

·Past performance of a financial product or index is not indicative of future results. These products involve the risk of loss, which can be substantial and, depending on the type of product, can exceed the amount of money deposited in establishing the position.

·This information is not being provided as part of an offer or sale of any futures or options products to any persons located within the United States or to a jurisdiction where the provision of this information is prohibited

Options involve risk and are not suitable for all investors. Prior to buying or selling an option, a person must receive a copy of Characteristics and Risks of Standardized Options. Copies are available from your broker, or at www.theocc.com. The information in this program is provided solely for general education and information purposes. No statement within the program should be construed as a recommendation to buy or sell a security or to provide investment advice. The opinions expressed in this program are solely the opinions of the participants, and do not necessarily reflect the opinions of Cboe or any of its subsidiaries or affiliates. You agree that under no circumstances will Cboe or its affiliates, or their respective directors, officers, trading permit holders, employees, and agents, be liable for any loss or damage caused by your reliance on information obtained from the program.

Copyright © 2023 Chicago Board Options Exchange, Incorporated. All rights reserved.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Cboe Global Markets and is being posted with its permission. The views expressed in this material are solely those of the author and/or Cboe Global Markets and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!