- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted November 16, 2021 at 10:26 am

A concise weekly overview of the U.S. equities and derivatives markets

Last week (November 8 – November 12), inflation was the word of the week in U.S. equity markets. The large and small cap indices all fell incrementally but remain near all-time highs. On Wednesday, new Consumer Price Index (CPI) data showed an annualized increase of 6.2%, the highest annual inflation reading since 1990. Additionally, Producer Price Index (PPI) data was up 8.6%, the highest reading in 11 years. Core CPI has been above the Federal Reserve’s target of 2.0% for seven months. Between late 2011 and early 2020 (pre-pandemic), CPI averaged an increase of 1.6% annually. The narrative underpinning the inflation data remains centered on strong demand, supply chain issues, higher commodity prices and labor imbalances.

U.S. Treasuries sold off (yields higher) following the release of PPI and CPI data. The probability of more than one hike in the Fed Funds rate next year climbed. The Fed’s tapering of its monthly asset purchases is expected to conclude around June 2022, when the prospect of hikes will become more likely. Reports that President Biden interviewed Federal Reserve Governor Lael Brainard, a perceived “dove,” as well as Federal Reserve Chair Jerome Powell last week, indicate that the administration is making progress toward nominating the next Federal Reserve chair.

The University of Michigan Consumer Confidence Index data released on Friday was weak, falling to the lowest level since 2010. In terms of S&P 500 Index sector performance, the Health Care and Industrials sectors led with slight gains, while the Consumer Discretionary and Energy sectors lagged, declining 3.6% and 1.6% respectively.

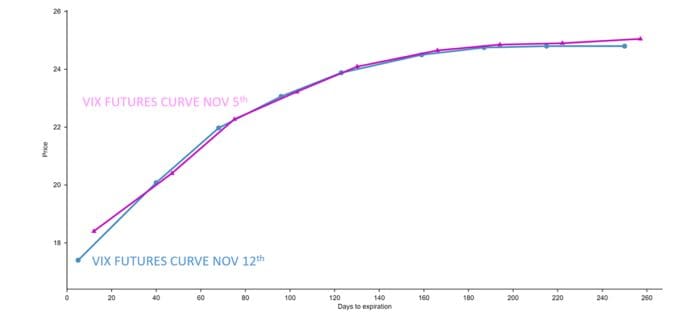

Observations on VIX futures term structure

Source: LiveVol Pro

Source: The New York Times

Source: St. Louis Federal Reserve

Source: The Daily Shot

Source: Multpl/Robert Shiller

—

Originally Posted on November 15, 2021 – The Week that Was: November 8 to November 12

There are important risks associated with transacting in any of the Cboe Company products discussed here. Before engaging in any transactions in those products, it is important for market participants to carefully review the disclosures and disclaimers contained at https://www.cboe.com/options_futures_disclaimers

Options involve risk and are not suitable for all investors. Prior to buying or selling an option, a person must receive a copy of Characteristics and Risks of Standardized Options. Copies are available from your broker, or at www.theocc.com. The information in this program is provided solely for general education and information purposes. No statement within the program should be construed as a recommendation to buy or sell a security or to provide investment advice. The opinions expressed in this program are solely the opinions of the participants, and do not necessarily reflect the opinions of Cboe or any of its subsidiaries or affiliates. You agree that under no circumstances will Cboe or its affiliates, or their respective directors, officers, trading permit holders, employees, and agents, be liable for any loss or damage caused by your reliance on information obtained from the program.

Copyright © 2023 Chicago Board Options Exchange, Incorporated. All rights reserved.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Cboe Global Markets and is being posted with its permission. The views expressed in this material are solely those of the author and/or Cboe Global Markets and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The information in this material is provided for informational purposes only and does not constitute tax advice and cannot be used by the recipient or any other taxpayer to avoid penalties under any federal, state, local or other tax statutes or regulations, or to resolve any tax issue.

TRADING IN BITCOIN FUTURES IS ESPECIALLY RISKY AND IS ONLY FOR CLIENTS WITH A HIGH RISK TOLERANCE AND THE FINANCIAL ABILITY TO SUSTAIN LOSSES. More information about the risk of trading Bitcoin products can be found on the IBKR website. If you're new to bitcoin, or futures in general, see Introduction to Bitcoin Futures.

Options involve risk and are not suitable for all investors. For information on the uses and risks of options, you can obtain a copy of the Options Clearing Corporation risk disclosure document titled Characteristics and Risks of Standardized Options by going to the following link ibkr.com/occ. Multiple leg strategies, including spreads, will incur multiple transaction costs.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!