- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted August 2, 2024 at 9:46 am

The short-lived satisfaction of Fed Chief Powell communicating decent odds of a September rate cut has turned sour as investors are now panicking that the central bank isn’t trimming soon enough. Indeed, in our commentary yesterday, we warned that an afternoon reversal following the FOMC meeting was in the cards. While bulls kept their momentum to finish the month, bears kicked off August by capitalizing on much weaker-than-expected ISM-manufacturing and unemployment claim prints to push equities deep into the red in dramatic U-turn fashion. Market players are also worried that the US is among the last to begin accommodating monetary policy, with the BoE narrowly deciding to reduce borrowing costs this morning.

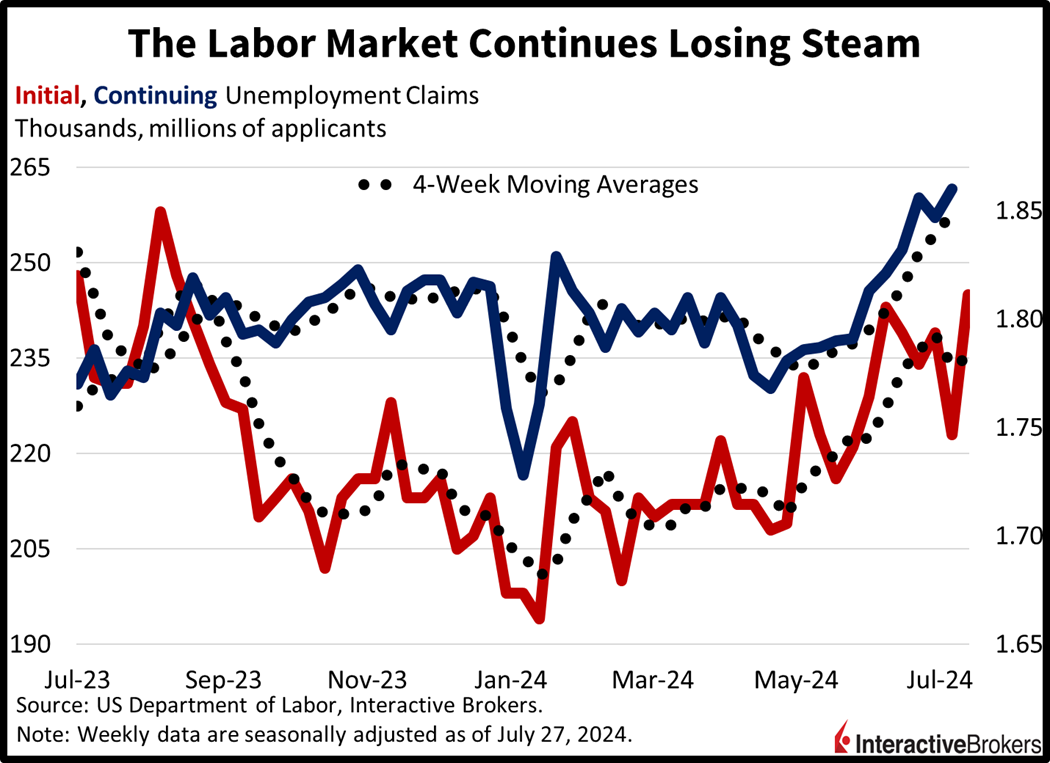

The labor market continues to reflect persistent weakness, with unemployment claim trends worsening in the past two weeks. Initial unemployment claims rose to 249,000 for the week ended July 27, much higher than the 236,000 projected and the 235,000 from the prior period. Continuing claims, meanwhile, increased to 1.877 million for the week ended July 20, above the previous interval’s 1.844 million and the median estimate of 1.860 million. Four-week moving averages also deteriorated on both fronts, rising from 235,500 and 1.852 million to 238,000 and 1.857 million. This morning’s release showing an increase in unemployment claims follows yesterday’s news from ADP of employers cutting back on hiring and slowing wage growth. Tomorrow’s non-farm payrolls will provide another fresh look into employer attitudes.

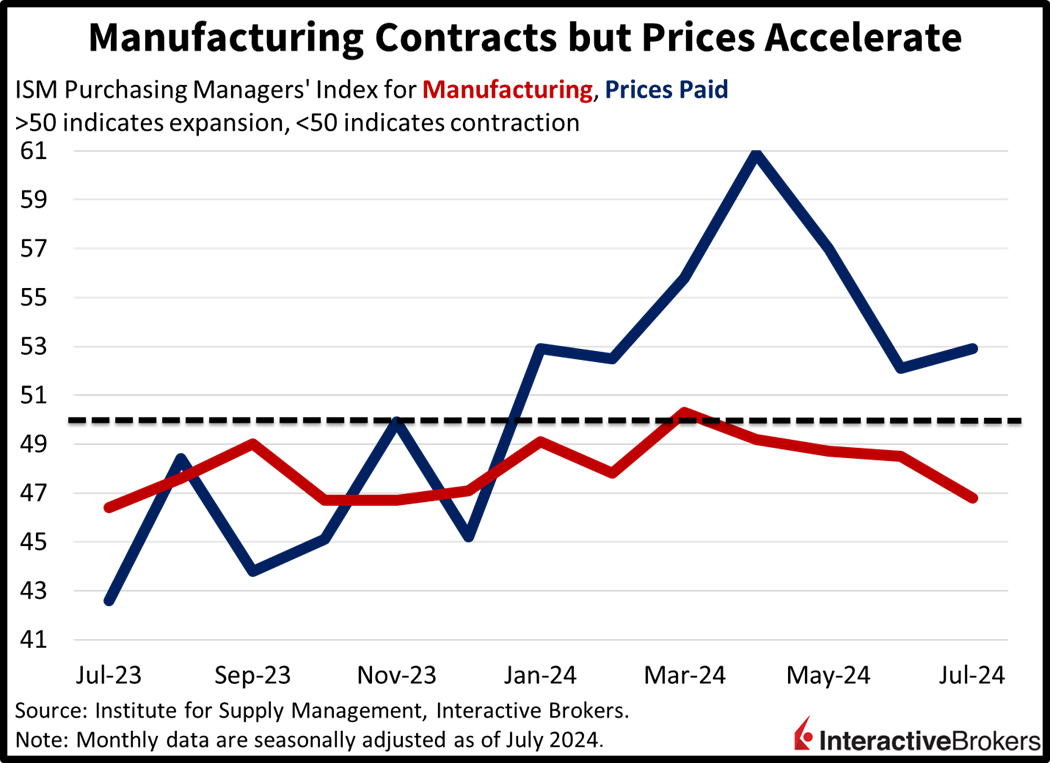

Reflecting further evidence of a decelerating economy, the manufacturing sector suffered a severe contraction last month. The Institute for Supply Management’s (ISM) Purchasing Managers’ Index for Manufacturing tanked deep into contraction territory, achieving a score of 46.8, beneath June’s 48.5 and the estimated 48.8. But despite orders and employment significantly weighing on the sector, prices gained momentum, accelerating to 52.9 from 52.1 on a month-to-month (m/m) basis.

Construction spending also showed weakness for the month of June, declining 3%, while analysts anticipated a 2% increase, but the Commerce Department’s data are stale because they do not reflect the recent bump in activity due to lighter mortgage rates.

Policymakers with the Bank of England (BoE) voted 5-4 in narrow favor of an initial cut to the benchmark interest rate, lowering it 25 basis points (bps) to 5%. The central bank reached the decision despite services inflation in June reaching 5.7%, a result, in part, of a Taylor Swift tour driving up hotel prices, although inflation-linked telephone contracts were another factor. BoE Governor Andrew Baily said monetary policy committee members anticipate keeping the rate restrictive for a sufficiently long period of time as they expect overall inflation may climb from 2% to 2.75%. The central bank has maintained one of the most restrictive policies among developed nations, with a labor shortage and Brexit having fueled price pressures.

Artificial Intelligence (AI) resulted in Meta and Qualcomm posting strong quarterly results while the formidable challenges faced by consumers have created a household goods recession. Consider the following earnings release summaries:

Markets are approaching panic mode as a plethora of economic factors converge and support a drift away from risk assets. Investors are dropping stocks like rocks and opting for Treasurys and Swiss francs instead. All major equity indices are in the red following sharp morning gains, with the Russell 2000, Nasdaq Composite, Dow Jones Industrial and S&P 500 benchmarks traveling south by 2.9%, 1.3%, 1.1% and 0.8%. Energy, technology and industrials are the heaviest laggards; they’re declining 2.3%, 2.1% and 1.9%. Sector breadth isn’t as dire, however, as market players are scooping up real estate, communication services and the defensive utilities, health care and consumer staples components; those segments are higher by 1.3%, 0.9%, 0.8%, 0.4% and 0.3%. Treasurys are getting bid up hand over fist with participants worried that the nation could fall into recession. The 2- and 10-year maturities are down 7 and 5 bps to 4.19% and 3.99%. The dollar is up though on the back of the BoE’s reduction this morning, with global traders viewing Washington as one of the last to provide accommodation. The greenback is gaining relative to all of its major counterparts ex-franc; it’s appreciating versus the euro, pound sterling, yen, yuan and Aussie and Canadian dollars. Commodities are also getting punished on demand concerns, with copper, silver, crude oil, lumber and gold lower by 2.3%, 1.8%, 1.7%, 0.2% and 0.1%.

While this year’s stock rally has been driven by AI and the technology’s potential to boost productivity and the bottom line, market players are worried about much greater problems. This evening’s reports from Apple and Amazon may provide bulls with short-term relief, especially if tomorrow’s non-farm payrolls report is well received. But this quarter, ladies and gentlemen, is all about the bears taking back some of the gains from the bulls. The headwinds for this market are just too stormy, especially considering that equities are priced for perfection. What are we seeing in the economy? imperfection. We’re going back to 5,000.

Visit Traders’ Academy to Learn More About ISM-Manufacturing and Other Economic Indicators

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!