- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted August 14, 2024 at 12:36 pm

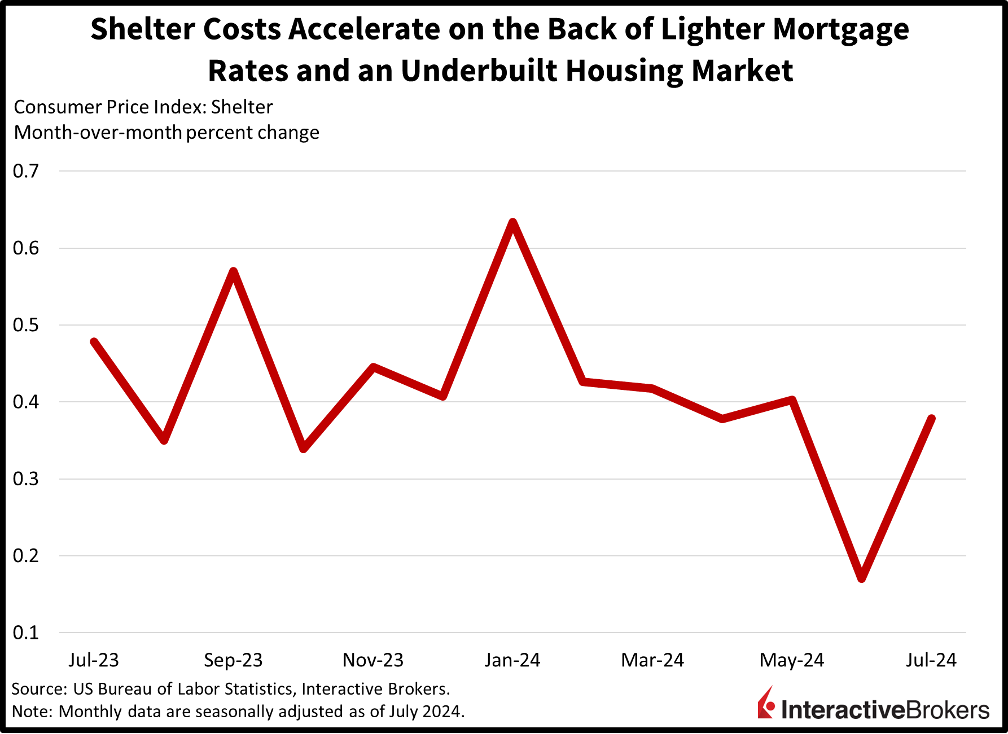

Market participants are confounded following this morning’s CPI report, which has produced a morning reversal in equities and fixed-income after yesterday’s strong gains. On the one hand, inflationary pressures are well contained near 3%, but on the other, shelter costs accelerated fiercely on the back of lighter mortgage rates and an underbuilt housing market. Reduced borrowing costs for prospective homeowners and landlords alike are serving to lower debt service expenses but are supporting property valuations and price pressures at levels above the Fed’s 2% target. Against the backdrop, odds in both the IBKR Forecast Trader and fed funds futures are favoring a 25-bp trim next month, with participants in the former market carrying more conviction.

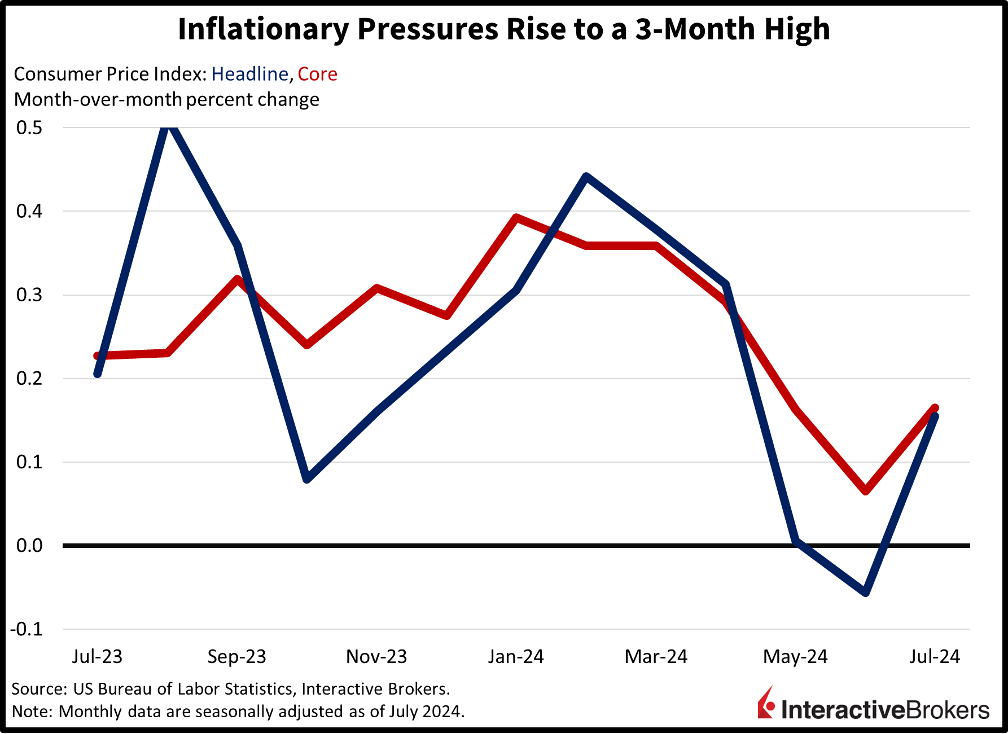

Inflationary pressures picked up steam last month with July’s Consumer Price Index (CPI) accelerating to its fastest monthly rate since April. Still, however, charges arrived in-line with estimates, rising just 0.2% month over month (m/m) and 2.9% year over year (y/y), which compares to -0.1% and 3% in June. The core CPI, which excludes food and energy due to their volatile characteristics, increased 0.2% m/m and 3.2% y/y, matching expectations and near the previous month’s 0.1% and 3.3%.

Cost trends were mixed across categories, with increases concentrated in the shelter and transportation services components, which saw prices move north by 0.4% m/m. For housing, the greatest weighting in the CPI, price momentum quickened from a mere 0.2% in June, pointing to significant inflationary risks associated with interest rate declines. Meanwhile, dining establishments, medical care commodities, food at markets and energy commodities experienced modest m/m upticks between 0.1% and 0.2%. Countering the price hikes were deflationary developments occurring in used automobiles, apparel, medical care services, new vehicles and energy services (heating & electricity), which saw discounts of 2.3%, 0.4%, 0.3%, 0.2% and 0.1%.

Investment banking and wealth management continue to experience strong demand while consumers in the US appear to be maintaining levels of fresh fruit purchases. Also in the US, ecommerce is still expanding. Consider the following earnings highlights:

Asset prices are mixed with stocks and bonds alike already trading red to green several times today. For equities, the Russell 2000 and Nasdaq Composite benchmarks are lagging with losses of 0.8% and 0.2%, while the Dow Jones Industrial and S&P 500 indices sport gains of 0.2% and 0.1%. Similarly, sector breadth is mixed, with 7 out of 11 sectors higher, being led by financials, real estate and consumer staples; they’re gaining 0.7%, 0.6% and 0.4%. Communication services, consumer discretionary and materials are leading to the downside with losses of 0.7%, 0.5% and 0.3%. Treasurys are near the flatline and changing hands at 3.93% and 3.83% across the 2- and 10-year maturities. The dollar gauge (DXY) is lower by 17 bps as the greenback depreciates versus the euro, franc, yen and yuan but gains against the pound sterling and Aussie and Canadian dollars. Commodity majors are weaker across the board except for lumber, which is up 0.7% and benefitting from this morning’s acceleration in shelter costs that may embolden builders to add more supply. Crude oil, silver, gold and copper are traveling south by 1.7%, 1.2%, 0.6% and 0.3%. WTI is trading at $77.38 per barrel as an inventory build stateside contends with a reduced conflict premium fueled by lighter expectations of a Middle Eastern escalation.

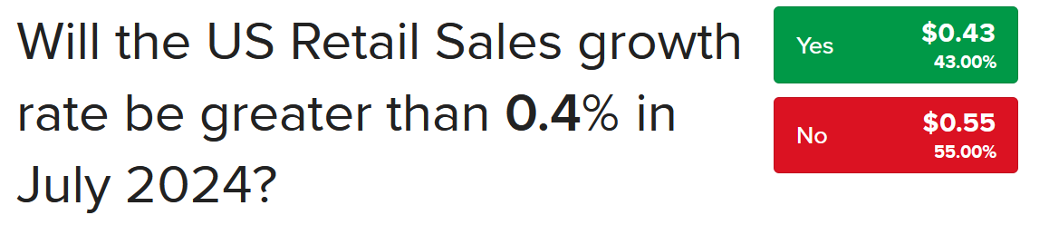

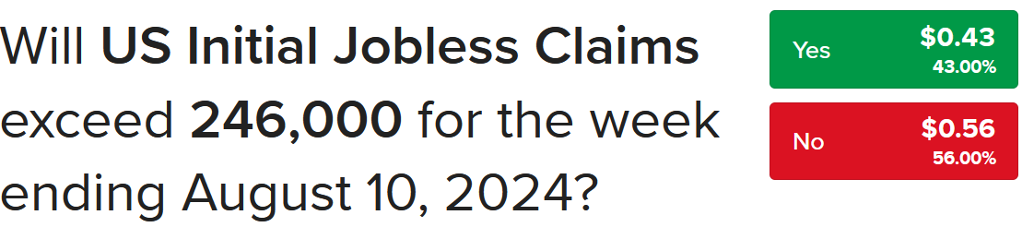

While this morning’s CPI figures dented the path toward a 50-bp reduction next month, tomorrow’s numbers on shopping patterns and layoffs may offer some optimism for monetary policy doves. Indeed, ForecastEx players are carefully selecting contracts for tomorrow morning’s retail sales and unemployment claim prints. For retail sales, investors are favoring the No contract for a figure exceeding 0.4% m/m, with the highest bids for Yes and No at $0.43 and $0.55. Turning to the labor market, ForecastEx participants are also preferring the under on initial claims exceeding 246,000, with the tallest bids for Yes and No at $0.43 and $0.56. A strong showing of these two reports pointing to robust transaction volumes and contained layoffs will likely weigh on asset prices, sending stocks south and yields north, as the data may block what market bulls want: the start of an aggressive Fed easing cycle. The bears, meanwhile, are preferring a tempered glide down to the terminal rate, rather than a swift elevator ride to the basement.

To learn more about ForecastEx, view our Traders’ Academy video here

New to Interactive Brokers?

Open AccountThe analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Interactive Brokers LLC is a CFTC-registered Futures Commission Merchant and a clearing member and affiliate of ForecastEx LLC (“ForecastEx”). ForecastEx is a CFTC-registered Designated Contract Market and Derivatives Clearing Organization. Interactive Brokers LLC provides access to ForecastEx Forecast Contracts for eligible customers. Interactive Brokers LLC does not make recommendations with respect to any products available on its platform, including those offered by ForecastEx.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!