- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted August 15, 2025 at 12:49 pm

Yesterday was an odd and exciting day for me. For the first time in my (long; too long?) career, I was on the NYSE floor to participate as an IPO began trading. As a result, and despite my location, I was not as plugged into the intraday market movements as normal. Frankly, I was quite surprised to see the stock market’s reaction – or lack thereof – to the PPI report.

For those of you who have noticed my love of classic comedies, it should be little surprise that two of them came to mind when I was considering how stocks were essentially ignoring the newest inflation data. One was The Big Lebowski and its subplot about nihilists. The other was Meatballs, a far lesser film, but featuring Bill Murray’s rant about “It just doesn’t matter!” Take your pick – they’re both saying essentially the same thing.

First, a digression about the IPO. I have been privileged to be among the groups ringing the opening and closing bell at Nasdaq a few times. One of them was not when IBKR went public – I was helping to keep our then-critical market-making operations functional – but I was there when we re-listed on that exchange and on at least a couple of other recent occasions. I’ve also been part of the bell ringing ceremony at the Montreal Exchange at least twice. All were quite special, but to be fair, a historic building makes an impossible-to-duplicate backdrop. Even the team at the NYSE’s rival exchange group Miami International Holdings (MIAX), a relative newcomer, were impressed. (Full disclosure – IBKR owns a stake in MIAX, and as a result, I represent our firm on the board of its MIAX Pearl options and stock exchange.)

Spending the morning at a celebratory gathering in relatively unfamiliar surroundings meant that I was by no means as plugged into my customary news and market data sources as usual. The irony, of course, was that I was at an exchange amidst a group of other exchange and market professionals, but the location and schmoozing hardly replaced sitting at my desk analyzing data. (That said, it was much more fun, and the food was better.) Thus, I was rather surprised to see that stocks had generally yawned at the stunning +0.9% monthly jump in both the headline and Core Producer Price Index levels.

It seemed to me then, and now, that there is no way to sugarcoat an unpleasant surprise of that magnitude. On Tuesday, stocks and bonds both cheered the essentially in-line CPI report. Expectations for a 25-basis point rate cut, which were already robust, increased to a certainty. In fact, by Wednesday, Fed Funds were pricing in a slight chance for a 50bp cut at the September 17th FOMC meeting. After the PPI report, that expectation reverted to reflecting similar expectations to those that prevailed prior to the CPI. The yield curve reacted similarly, with bonds giving back virtually all their prior gains. Yet stocks meandered around unchanged levels throughout yesterday’s session, never giving back more than a small fraction of Tuesday’s rally:

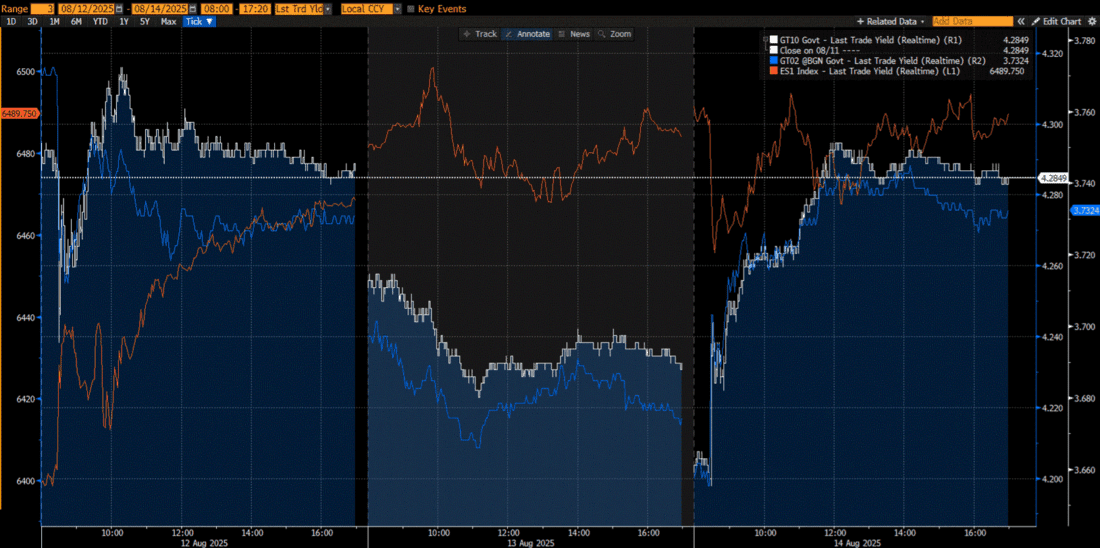

3-Day Chart, from 8:00am – 5:20pm EDT daily, September ES futures (red, left);10-year (white, right) and 2-year (blue, right) US Treasury Yields

Source: Bloomberg

Major stock indices have been exhibiting something of a ratchet effect. They move higher, often sharply higher, on good, or even just OK news, but only falling modestly – if at all – on bad news. That certainly describes the outcome of yesterday’s trading, where two separate groups of rational investors interpreted the same unpleasant data in a completely different manner. We see something similar today, with stocks only declining modestly after receiving the latest set of concerning surveys from the University of Michigan:

There is no way to read that data in a positive manner, except to offer the caveat that “soft data”, like surveys, is less meaningful than “hard data” like government statistics. (Of course, as were all recently reminded, the monthly jobs data from the BLS is also collected from surveys.)

We’ve utilized the term “nihilist market” before when it appeared that stock traders were so focused upon momentum-driven returns that they were ignoring key fundamentals. We unveiled that term on February 14th, 2020, when we expressed surprise at stock traders’ willingness to ignore news about a potential epidemic, writing:

This morning I was greeted with the following alert from Bloomberg news on my iPhone:

“Coronavirus infections still rising, Fed reduces repo operations, and euro-area economy stagnates. Here’s what’s moving markets.”

I should have been surprised that, despite the trifecta of gloomy headlines, US index futures were trading up about 0.2%, but I wasn’t. That sort of thing doesn’t surprise me anymore. Stock markets seem to have taken on a life of their own, beholden only to money flows and positive sentiment.

Our use of the term was similarly well-timed in August 2022, but far less so later in 2020 and in early 2024. Take the current opinion with a large grain of salt. But a market that willfully puts on blinders when confronted with inconvenient news, such as greeting the double whammy of sharply lower sentiment and higher inflationary expectations and readings with a relative yawn, makes me wonder whether “it just doesn’t matter” has become a new market mantra.

New to Interactive Brokers?

Open AccountAlready an Interactive Brokers Client?

Request Trading PermissionThe analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

Outstanding analysis! It was a tough week for day trading SPY as the news was leading one way and the price action seemed to be the opposite direction. Even earnings were difficult as many of those days seemed to be topsy turvy too!

Rational analysis of an irrational phenomenon- the current stock market.

AI has everyone mesmerized. And, yes, TBL is much better than MB.

And yet no one is talking about it, because it is no longer irrational to ignore the irrational. In fact, these days, pointing out the irrational is riskier than being irrational. What are you going to do?

Hi Steve, we rarely agree, but this time it could be me writing this article. I finally agree 100% with you. Despite voices stating that the importers and producers won’t pass the tariffs costs to consumers, I can only say that PPI today will be CPI tomorrow. Btw, we disagree mainly about the government. I believe it will fail in a scale never seen in the history of the US. Time will tell.

Obviously, the market has amnesia. It has forgotten that yes, given sufficient time and insufficient BS and speculation, it does also go lower. How quickly we forget. Selective memory? Preference bias? End – or close to the end – of a bull run…? No one can, or is willing to say, or take the punch bowl away…. i.e. until it happens or they are too punch drunk to remember. Only time will tell… “I don’t like chasing Bubbles, he doesn’t always come back” — Michael Jackson, commenting on Bubbles, his pet chimpanzee

When a new mantra doesn’t match reality, go with reality. I’ve moved most of my stuff to $BIL.

It may not matter but when the joke is over – it most certainly will matter.

Yeah, well, that’s just like, your opinion, man.