- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted November 24, 2025 at 10:00 am

After an exceptionally strong start to the year, the S&P 500 has entered a period of notable weakness. Over recent weeks, the index has retreated from its highs as investors reassessed inflation expectations, interest-rate trajectories, and corporate earnings durability.

Several sectors that previously led the rally, such as technology and consumer discretionary, have shown signs of fatigue, contributing to short-term downward pressure. At the same time, defensive pockets of the market have stabilized, highlighting a rotation in market sentiment rather than a structural breakdown.

While corrections are a natural part of market cycles, the question now is whether the current pullback represents the beginning of a deeper downturn or simply a healthy consolidation within a broader upward trend. To explore this, we look at four different lenses: seasonality patterns, fundamental valuation, and AI-based market projections.

Historical seasonality provides a useful lens for interpreting the current environment. When comparing the present price action with the typical seasonal path, as well as with last year’s pattern, the resemblance is striking.

In the detrended seasonal chart (chart above), the correlation between the current year and the previous year exceeds 78%, suggesting that the market is broadly following a similar rhythm. Notably, both periods show a plateau in November followed by a tendency toward weakness in the early winter months.

Seasonality therefore indicates that the market could experience a few additional weeks, potentially even months, of volatility or mild downside pressure before historically entering a more constructive phase later in the new year. While seasonality does not guarantee outcomes, the current alignment is unusually close and worth monitoring.

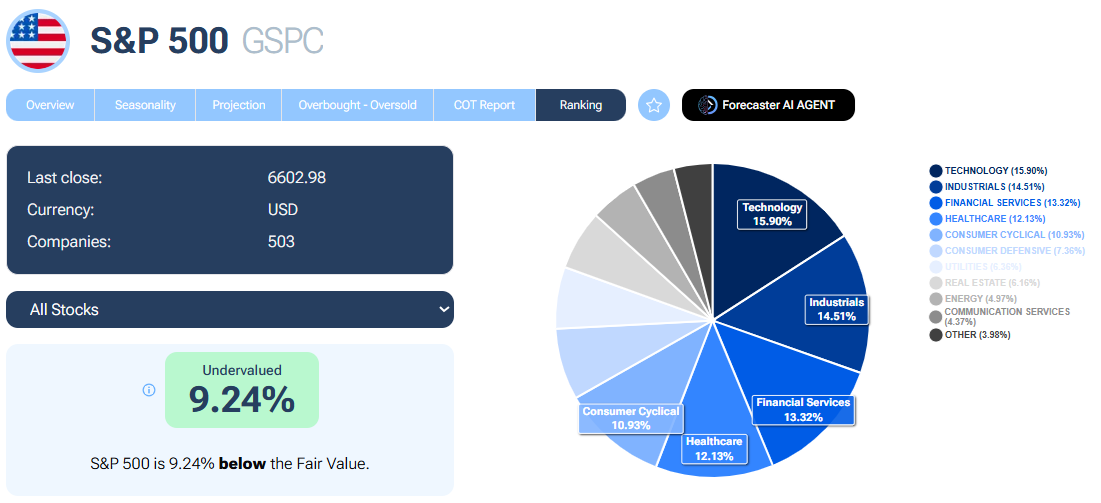

A bottom-up valuation of the S&P 500, based on the fair value estimates of the individual companies composing the index, suggests that the market remains fundamentally supported.

Fair value modeling suggests the S&P 500 is 9.24% undervalued, with Technology as the index’s largest sector.. Source: Forecaster Terminal S&P500 Ranking

According to this aggregate model, the S&P 500 is currently 9.24% below its estimated fair value. Several sectors contribute to this undervaluation, most notably technology, industrials, and healthcare, highlighting that despite elevated headline levels, the broad market does not appear overstretched from a valuation perspective.

This does not eliminate the possibility of short-term volatility, but it provides a counterpoint to the more cautious seasonal signals. Fundamentally, many companies continue to show solid earnings resilience and long-term growth potential.

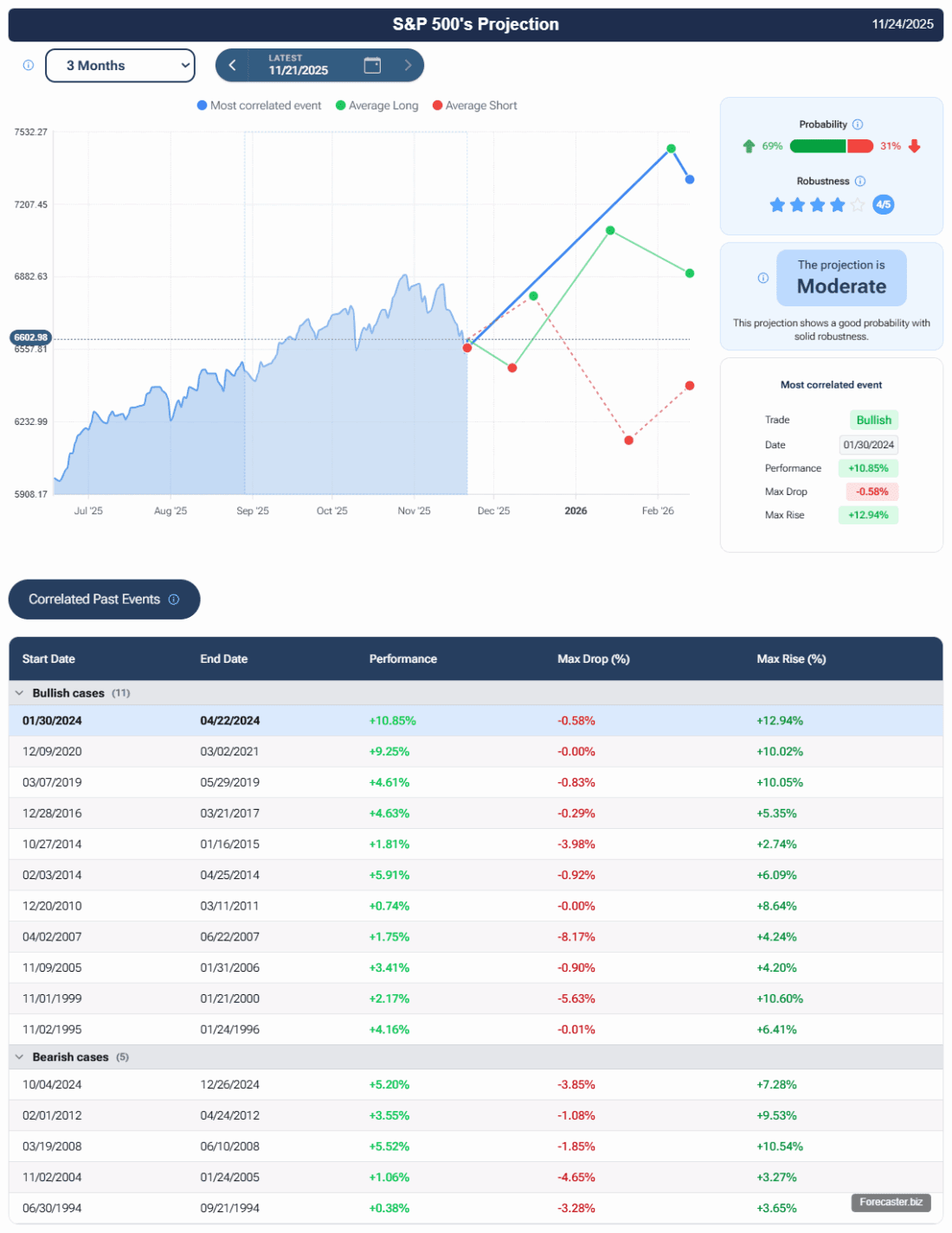

To complement traditional analysis, Forecaster’s AI-driven projection model (the so called ChatGPT for finance ) suggests that while further downside cannot be excluded, the current movement may represent a standard retracement within a medium-term upward trend.

Out of 16 historical analogues identified by the model, 11 resulted in bullish scenarios — suggesting that past markets with similar setups often recovered after short-term weakness. Source: AI Projection Forecaster Terminal

The model assigns a moderate probability to the baseline scenario, with a 69% probability favoring a bullish continuation after a near-term consolidation. Historical analogues identified by the AI show that in similar setups the index experienced a temporary drawdown before recovering and advancing further.

However, as always, alternative outcomes remain possible. The bearish scenario—representing 31% probability—indicates that a deeper correction may materialize if macroeconomic pressures intensify or if earnings weaken more than expected.

The S&P 500 enters the final part of the year with a mixed but balanced outlook:

While the index may still experience volatility in the coming weeks, the combination of seasonal patterns and fundamental fair value estimates indicates that current conditions remain consistent with a corrective phase rather than a structural downturn. Investors should remain attentive to economic data, earnings revisions, and policy developments, all of which will play a crucial role in shaping the next leg of the market’s trajectory.

—

Originally Posted on November 24, 2025

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Forecaster.biz and is being posted with its permission. The views expressed in this material are solely those of the author and/or Forecaster.biz and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!