- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted March 11, 2025 at 11:15 am

Investors are further reducing their equity exposure following President Trump’s decision to increase tariffs on Canada to 50%. The news is clouding the economic outlook, specifically as it pertains to inflation, consumer demand and confidence. Furthermore, heightening trade tensions, government spending cuts and lackluster corporate earnings commentary are weighing on animal spirits, leading to traders running for cover in the commodity complex while adding to stock volatility protection through VIX calls and index equity puts. Meanwhile, the economic calendar was rather neutral, as a miss on NFIB coincided with a beat on JOLTS, but the price pressure data from the CPI and PPI to be released during the next two days are top of mind. Also, IBKR ForecastTraders are adding to wagers of a possible government shutdown this weekend with some participants opting to build speculative positions while others look to hedge their portfolios from the potential turbulence that such an event could generate.

Source: ForecastEx

Small business optimism fell for the second consecutive month in February as uncertainty regarding economic prospects weighed on sentiment. Additionally, labor quality and inflation remained the two top problems for survey respondents. Overall, declining confidence is subduing capital expenditure and hiring plans, contributing to the National Federation of Independent Business’s (NFIB) Small Business Optimism Index slipping to 100.7, beneath expectations of 101 and January’s 102.8. The figures have been dwindling from December’s 12-year high of 105.1, as the post-election enthusiasm has tempered.

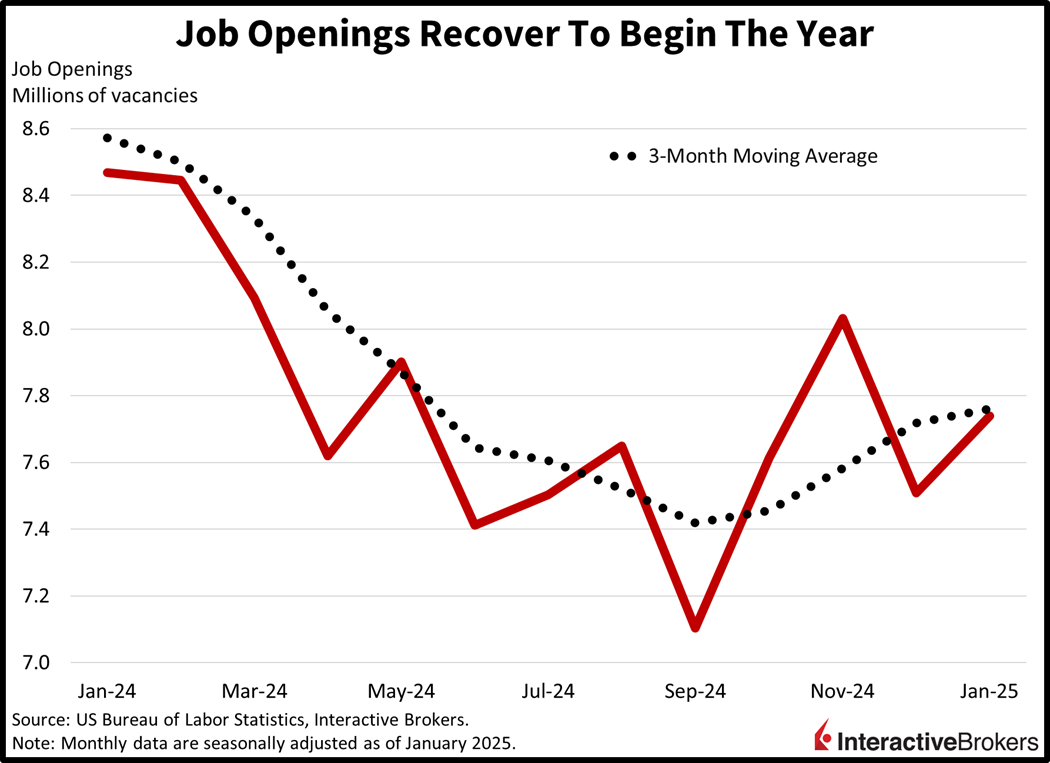

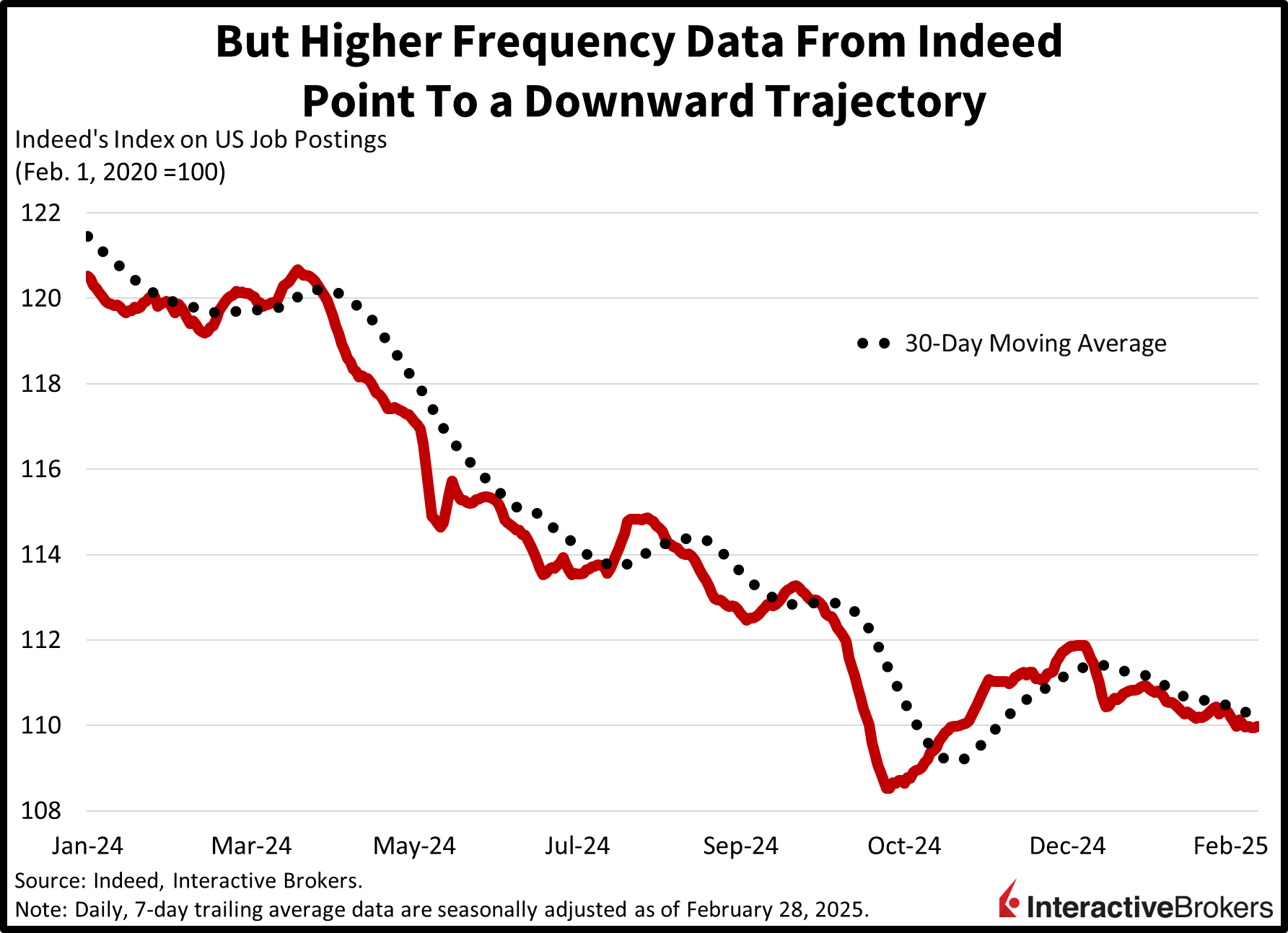

The new year started with employers adding a hefty number of for-hire signs, according to the Job Openings and Labor Turnover Survey (JOLTS). January vacancies rose to 7.74 million, eclipsing the 7.63 million median estimate and December’s 7.508 million. The retail and finance sectors expanded the most openings during the period, increasing 143,000 and 122,000, comprising a sizeable chunk of the total gain of 232,000. In an indication of healthy employment conditions at the beginning of 2025, job openings remained above the number of unemployed people, although the ratio has been tightening considerably. Furthermore, higher frequency data from Indeed, updated as of February 28, has been trending south, pointing to employment market deceleration.

Tariff tension is leading to investors scooping up commodity futures as they unload equities and Treasurys alike. Stock and fixed-income areas aren’t seeing much interest due to a softening earnings outlook amidst rising inflation expectations. Commodities are catching bids since their performance is positively correlated with price pressures while trade worries may disrupt supplies.

All equity benchmarks are lower on the session with the Dow Jones Industrial, S&P 500, Russell 2000 and Nasdaq 100 gauges losing 0.9%, 0.4%, 0.2% and 0.1%. Sectoral breadth is deeply negative with all 11 segments suffering losses. Leading the laggards south are consumer staples, industrials and health care, which are lower by 0.8%, 0.8% and 0.7%. Treasurys are also getting trimmed as the 2- and 10-year maturities change hands at 3.92% and 4.26%, 3 and 4 basis points (bps) heavier on the session. But weaker growth projections in the states are weighing on the dollar, despite yields climbing. The greenback’s index is down 50 bps as the US currency depreciates against the euro, pound sterling, franc, yuan and Aussie tender but appreciates versus the loonie and yen. Commodities are performing strongly with copper, silver, crude oil, gold and lumber higher by 2.4%, 1.9%, 1.4%, 1% and 0.6%.

Tomorrow’s Consumer Price Index (CPI) could arrive ahead of estimates, similar to the January print, as firms and consumers alike had braced for tariffs by raising their own inflation expectations. This psychological dynamic leads to companies increasing charges while households increasingly accept higher costs in light of trade policy uncertainty and front running efforts. Meanwhile, immigration restriction also pushes up wage bills via a capped labor force, which we saw in last week’s jobs report featuring a sharp decline in the participation rate. The one-two punch of tense international commerce and mass deportations has the potential to support an elevated price level even if economic growth decelerates, generating stagflationary winds. Finally, IBKR ForecastTraders assign a 32% chance that the headline CPI beats to the upside, but an opportunity has presented itself in the core CPI contracts this morning. While my expectation of the core figure is at 3.3% year over year (y/y) in tomorrow’s February report, the IBKR ForecastTrader prediction market offers the “Yes” version for a number above 2.9% at just $0.30, paying out a dollar if correct. I am labeling the “Yes” on Core CPI over 2.9% as a high-conviction call.

Source: ForecastEx

Household spending in Japan grew only 0.8% y/y and sank 4.5% month over month (m/m) in January, weakening significantly from the final month of 2024 and coming in short of expectations. In December, outlays grew 2.7% and 2.3% y/y and m/m, according to Japan’s Ministry of Internal Affairs and Communications. Meanwhile, analysts expected January to record a y/y increase of 3.6% and a m/m decline of only 1.9%.

Japan’s February machine tool orders racked up their fifth-consecutive y/y increase but fell short of economists’ expectations and growth moderated from the first month of the year, according to the Japan Machine Tool Builders’ Association. Orders climbed 3.5% and underperformed the estimate of 4.7%. Domestic transactions expanded 3.9% y/y while foreign activity advanced 3.4%. On a m/m basis, orders were 1.8% higher after dropping 18.8% in January.

The National Australia Bank’s (NAB) business survey climbed 1 point to 4 last month but confidence dropped significantly from 5 to -1. NAB Chief Economist Alan Oster maintains that lingering price pressures continue to challenge profits and he notes that confidence fell despite encouraging fourth-quarter data and policymakers reducing the country’s key interest rate. Overall orders were steady last month with the exception of retail, which experienced a decline.

Slowing inflation and a recent interest rate cut by the NAB helped push consumer confidence up 4% from 92.2 in February to 95.9 this month. It is the highest result in three years and reflects increased optimism regarding making major purchases and a stabilizing job market. Conversely, unsettling overseas news appears to be hindering sentiment.

To learn more about ForecastEx, view our Traders’ Academy video here

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Interactive Brokers LLC is a CFTC-registered Futures Commission Merchant and a clearing member and affiliate of ForecastEx LLC (“ForecastEx”). ForecastEx is a CFTC-registered Designated Contract Market and Derivatives Clearing Organization. Interactive Brokers LLC provides access to ForecastEx Forecast Contracts for eligible customers. Interactive Brokers LLC does not make recommendations with respect to any products available on its platform, including those offered by ForecastEx.

This is commentary on economic, political and/or market conditions within the meaning of CFTC Regulation 1.71, and is not meant provide sufficient information upon which to base a decision to enter into a derivatives transaction.

Related Articles

Really like these economic updates!