- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted October 27, 2025 at 9:45 am

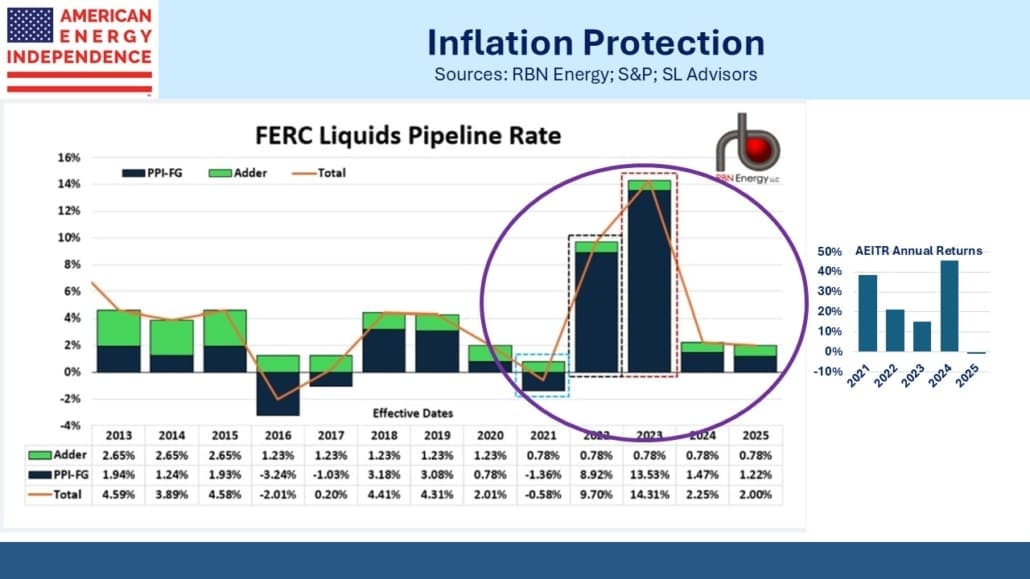

The link between inflation and fee increases for liquids pipelines doesn’t draw much attention, but it proved to be valuable to midstream investors three years ago when the Biden administration’s excessive stimulus drove the Producer Price Index (PPI) up 13%.

Maintaining purchasing power is the goal of most long-term investors. Inflation is reasonably close to the Fed’s target, but our dire fiscal outlook is well known. The White House is likely to maintain pressure for low rates for the remainder of Trump’s term in office, and through relentless criticism plus the choice of co-operative FOMC appointments when given the opportunity, he’ll probably get his way.

Last week the WSJ reminded us that during and after World War II, the Fed co-operated with the Treasury in maintaining low rates while “…inflation rose into the teens” (see How Federal Reserve Interest Rates Could Get Stuck on the Floor).

We’re heading into a period of political constraints on the Fed to raise rates in response to higher inflation.

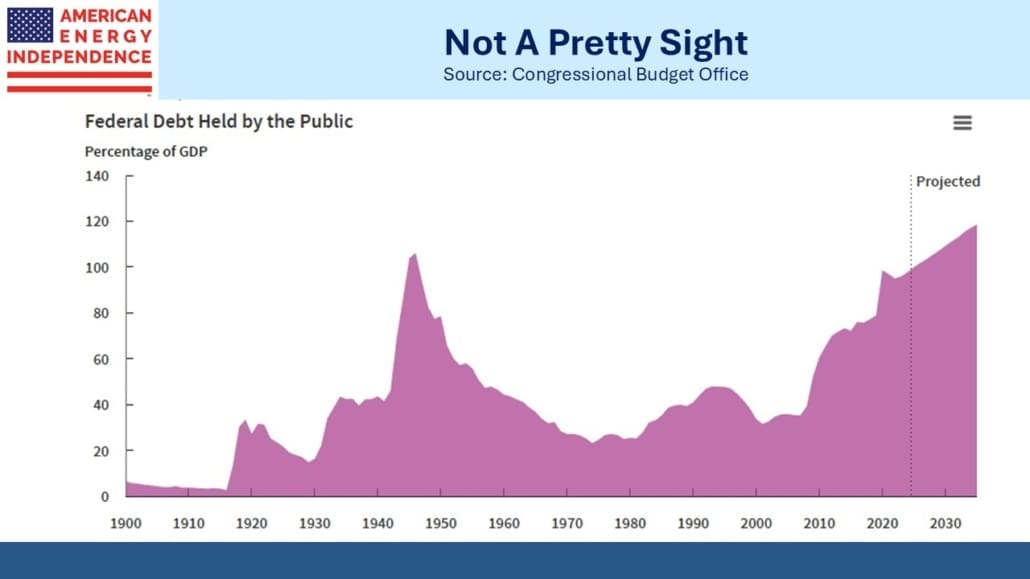

With US Debt:GDP approaching the levels of 1946 when the war ended and assuredly heading higher, it’s worth reviewing the pricing power embedded in pipeline contracts.

It’s generally estimated that around half the EBITDA of the midstream sector is subject to automatic price hikes linked to PPI plus a margin set every five years by the Federal Energy Regulatory Commission (FERC). The purpose is to ensure that pipeline owners can maintain an adequate profit margin that incentivizes continued investment in the sector.

The chart from RBN Energy shows the startling yet lucrative impact of this in 2022-23, which coincided with and partially drove some sparkling returns for the American Energy Independence Index (AEITR).

FERC sets an adjustment factor, which is usually positive, every five years. It was last set in 2020 at +0.78% when FERC was under Republican leadership. However, in 2022 when FERC was under Democrat leadership, the adjustment factor was changed from +0.78% to –0.21%.

The industry sued and last year the U.S. Court of Appeals for the D.C. Circuit vacated the order.

FERC is now under Republican leadership again, and next summer will set the adjustment factor for the five-year period beginning July 1, 2026. Pipeline companies are pressing for the adjustment factor to compensate for the two and a half years when it was incorrectly low. Pipeline customers understandably hold an opposing view.

If FERC does what the pipeline companies want, it will benefit liquids-focused companies, including names such as Oneok and Targa Resources, which have both been weak this year.

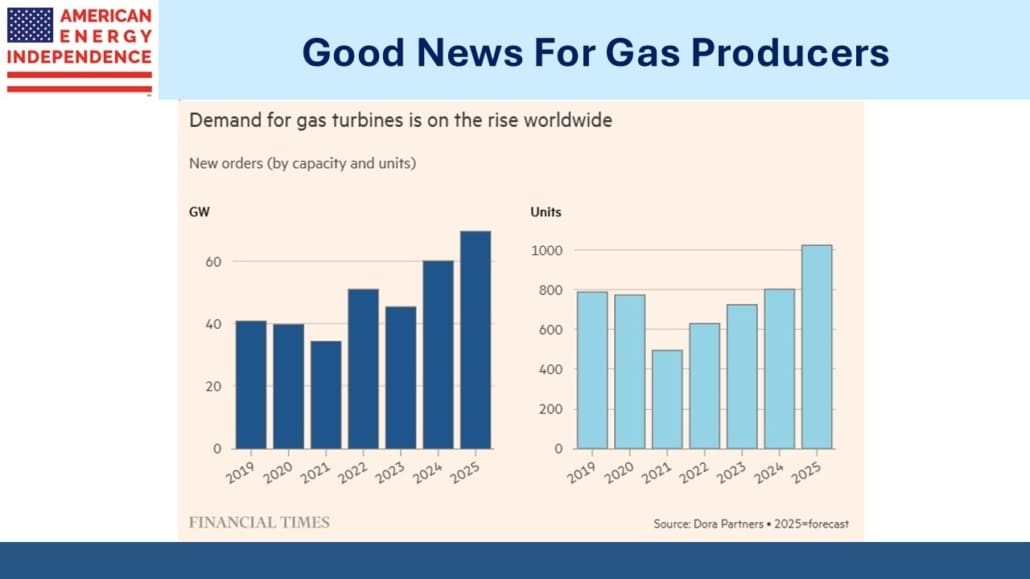

The twin drivers of demand for natural gas haven’t done much to help gas-oriented pipeline companies this year. The AI boom is so widely described as a speculative bubble that one must assume it’s not a secret. Goldman Sachs has estimated that generative AI needs to produce $1TN in annual revenue for the capital invested to earn an adequate return, roughly equal to our defense budget or interest on Federal debt.

Morgan Stanley thinks this could happen by 2028, up from $45BN last year.

Midstream companies providing Behind The Meter (BTM) direct hookups to gas supply for dedicated gas turbines aren’t exposed to the returns on equity earned by the data center owners. Buyers of gas turbines are facing a three-year backlog. A turbine is unlikely to be installed and not used, just as a gas pipeline is unlikely to be laid without a secure contract guaranteeing a return for the owner.

Williams Companies (WMB) announced a strategic LNG partnership with Australia’s Woodside Energy to own an interest in the Louisiana LNG facility. This is the project that Charif Souki originally launched with Tellurian, but it was sold to Woodside after Souki failed to obtain financing (see Tellurian Drifts Into Stronger Hands).

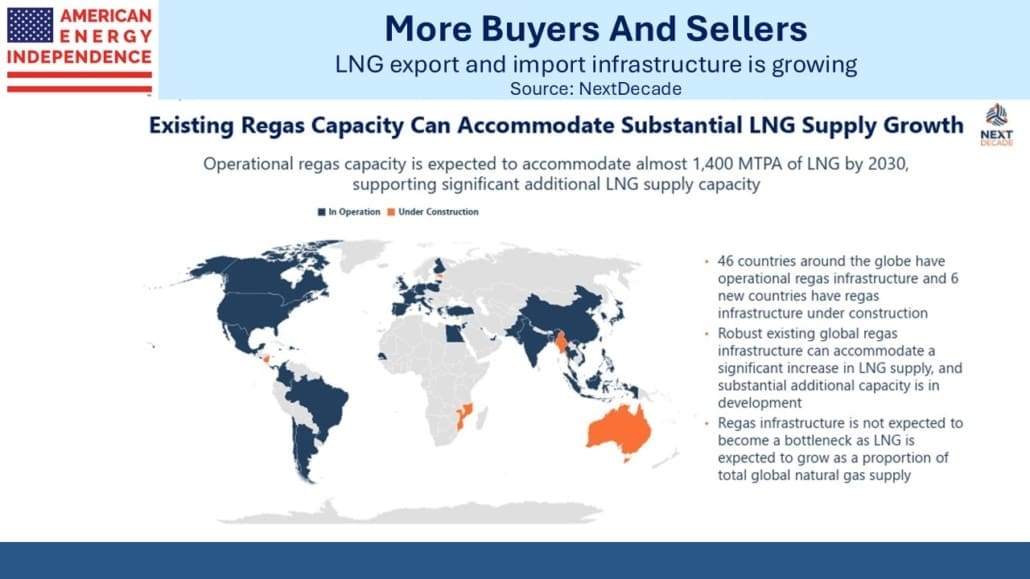

WMB’s stock dropped 5% on the news, confirming that the market fears a looming LNG glut and dislikes exposure to it. Total CEO Patrick Pouyanne has been warning of overcapacity among liquefaction terminals, with global capacity expected to rise from 425 Million Tonnes Per Annum (MTPA) to 600 MTPA by 2030.

Meanwhile, Total has restarted construction at its Mozambique LNG project after halting work in 2021 following a terrorist attack in nearby Palma town. If there is a glut they’ll be part of the reason. A slower build-out of competing facilities would suit Total.

New regasification continues to match the growth of liquefaction, maintaining a roughly 2X ratio between the receiving versus the sending side of LNG trade. The world’s buyers of LNG continue to prepare for increased shipments.

Although the precise terms of WMB’s investment with Woodside weren’t published, it’s likely that the perception of a glut would have been incorporated. In a form of vertical integration, WMB will be able to offer its customers gas transportation from its pipeline network and onto an LNG tanker. It looks like good timing on their part.

—

Originally Posted on October 26, 2025 – Inflation Protection From Pipelines

Please go to following link for important legal disclosures: https://sl-advisors.com/legal-disclosure

SL Advisors is invested in all the components of the American Energy Independence Index via the ETF that seeks to track its performance.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from SL Advisors and is being posted with its permission. The views expressed in this material are solely those of the author and/or SL Advisors and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!